Monday, December 31, 2018

Turpins’ ‘House of Horrors’ Is Up for Sale—but Who’d Buy It?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

One Year On, These Housing Markets Are the Winners and Losers of U.S. Tax Reform

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, December 28, 2018

Notable Numbers: December 2018

22%

Any uptick in a community's rent affordability beyond 22 percent translates into more people experiencing homelessness.

32%

Communities where people spend more than 32 percent of their income on rent can expect a more rapid increase in homelessness.

$222,800

The median home value nationwide in November, up 7.7 percent from a year earlier.

$257,700

Median sale price for existing homes in November, up 4.2 percent from a year earlier — and the 81st straight month of year-over-year gains.

43.2%

Share of buyers who put down 20 percent when buying a home.

24.2%

Share of buyers who put down 5 percent or less when buying a home.

5.4%

Additional share of currently for-sale homes that would be out of reach for a typical household’s budget if mortgage rates increase to 5.5 percent.

The post Notable Numbers: December 2018 appeared first on Zillow Research.

via Notable Numbers: December 2018

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Pending Home Sales Slump Again in November as Housing Market Faces Big Chill

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Well-Being Facilities, Designs From Top Pros and Sky-High Perks: The Amenities of 2019

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Not Quite Done, $44.5M Palm Beach Spec House Is the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, December 27, 2018

A New Seattle Housing Law Forbids Landlords From Checking Into Tenants’ Criminal History—but Does It Go Too Far?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

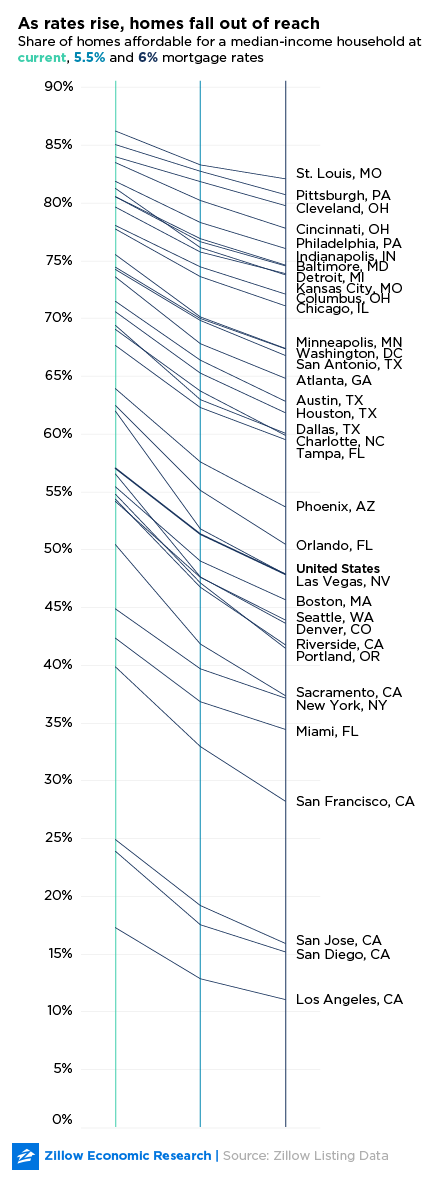

Rising Mortgage Rates Thorn in Otherwise Rosy Conditions for Home Buyers

- Mortgage rates have risen 0.7 percentage points this year, and most experts expect that trend to continue.

- If rates increase to 5.5 percent, it would eliminate an additional 5.4 percent of currently for-sale homes from a typical household's budget.

- Would-be home buyers in Las Vegas, Denver and Sacramento would be the most affected by rising rates.

As home-value growth slows and for-sale inventory ticks up, one would think that all is well for would-be home buyers. However, mortgage rates continue to grow, taking a big bite out of home shoppers' budgets and slicing the share of homes available to those looking to buy.

In fact, if mortgage rates grow to 5.5 percent from where they are today[1], a typical household looking to spend no more than 30 percent of its income on housing would have to slash its home-buying budget by nearly $35,000 to cover the higher mortgage payments. Doing so would eliminate 5.4 percent of currently for-sale homes, or about 31,700 homes, from a typical household's budget[2].

Mortgage rates rose substantially in 2018. The average 30-year fixed rate in the U.S. increased by 70 basis points this year[3], more than any year since 2013, when rates were just beginning to ascend from historic lows. In mid-November, rates touched their highest point since early 2011, nearly reaching the 5 percent mark, only to retreat slightly to end the year.

Even though rates declined in December, many experts expect that rates will resume their ascension in 2019. Zillow projects that by the end of the year, rates will have reached at least 5.5 percent, higher than any point since June 2009. The National Association of Realtors (NAR) also expects rates to rise to an average of around 5.3 percent sometime in the new year.

Even though rates declined in December, many experts expect that rates will resume their ascension in 2019. Zillow projects that by the end of the year, rates will have reached at least 5.5 percent, higher than any point since June 2009. The National Association of Realtors (NAR) also expects rates to rise to an average of around 5.3 percent sometime in the new year.

Increasing mortgage rates present financial issues for potential buyers:

- Homeowners are less likely to sell their domiciles, as they themselves would be forced to take on more expensive debt to buy a new home. Because they stay put, there are fewer available homes on the market.

- What's more, homes become less affordable, as higher rates make the typical monthly payment represent a larger share of a buyer's income. In other words, the value of a home that a would-be buyer can afford will decrease as mortgage payments eat into their budget.

- A rate increase also limits the number and share of homes on the market that a buyer can afford. These (now fewer) affordable homes will become more competitive and could potentially sell at a premium, as a result.

As a result, many home buyers will likely have to reset their price points and possibly make concessions — about where they want to live, how large a home they want, among others.

Should rates reach beyond 5.5 percent to the 6 percent threshold, the impact would, obviously, be even larger. Compared to the current environment, the typical household would have to set its budget $52,800 lower, eliminating close to 50,000, or 8.5 percent, of current for-sale homes from its radar.

As one would expect, the impact of rate changes varies regionally. Of the 35 largest metro areas in the U.S., a mortgage rate increase to 5.5 percent would have the greatest impact in Las Vegas. Such a rate hike would make a whopping 10.2 percent of currently for-sale Sin City homes no longer affordable to the typical household there, which earns an annual income of $57,900. A rate increase to 6 percent would remove 14.1 percent, or more than 1,500, of today's for-sale homes from the ranks of affordability.

Households looking to buy in Portland, Ore., Sacramento, Calif., Denver, Riverside, Calif. and Orlando, Fla., also would disproportionately feel the impact of rising rates: In each of those metros, a move to 6 percent rates would eliminate more than 12 percent of currently for-sale homes from a typical household's budget.

The impact of rising mortgage rates on the share of affordable for-sale homes would be smallest in St. Louis, where only 4.1 percent of homes would no longer be affordable to the median household should rates reach 6 percent. Following the Gateway to the West is Cleveland, (where 4.2 percent of for-sale homes would no longer be in the typical family's budget) and Pittsburgh (4.3 percent). Each of these three metros has a median home value that is less than that of the nation.

Although growing mortgage rates would have the most immediate impact on potential home buyers, renters would feel the effects as well. As increasing rates limit the number, and share, of affordable homes for buyers, many of those potential buyers would choose to abandon the home search and continue renting. As a result, should more households choose to renew their leases, after a few months of slow or even negative growth, many experts believe rents would resume their climb alongside mortgage rates.

| Metro | Share of homes affordable at current rates | Share of homes affordable at 5.5% | Share of homes affordable at 6% |

|---|---|---|---|

| New York, NY | 44.8% | 39.6% | 37.0% |

| Los Angeles, CA | 17.2% | 12.8% | 11.0% |

| Chicago, IL | 77.6% | 73.5% | 71.0% |

| Dallas, TX | 69.3% | 62.9% | 60.0% |

| Philadelphia, PA | 81.8% | 78.2% | 76.0% |

| Houston, TX | 70.5% | 65.2% | 61.7% |

| Washington, DC | 74.3% | 69.9% | 67.3% |

| Miami, FL | 42.2% | 36.7% | 34.3% |

| Atlanta, GA | 73.5% | 67.7% | 64.7% |

| Boston, MA | 55.3% | 48.9% | 45.6% |

| San Francisco, CA | 39.8% | 32.8% | 28.1% |

| Detroit, MI | 79.5% | 75.7% | 73.8% |

| Riverside, CA | 54.3% | 46.6% | 41.7% |

| Phoenix, AZ | 63.8% | 57.5% | 53.6% |

| Seattle, WA | 54.1% | 47.5% | 43.8% |

| Minneapolis, MN | 75.4% | 70.0% | 67.3% |

| San Diego, CA | 23.8% | 17.4% | 15.1% |

| St. Louis, MO | 86.1% | 83.2% | 82.0% |

| Tampa, FL | 67.6% | 62.2% | 59.4% |

| Baltimore, MD | 80.4% | 76.5% | 74.5% |

| Denver, CO | 56.4% | 47.5% | 43.5% |

| Pittsburgh, PA | 85.0% | 82.6% | 80.6% |

| Portland, OR | 54.7% | 47.0% | 41.4% |

| Charlotte, NC | 69.0% | 63.6% | 59.8% |

| Sacramento, CA | 50.3% | 41.7% | 37.3% |

| San Antonio, TX | 74.1% | 69.7% | 66.7% |

| Orlando, FL | 62.4% | 55.0% | 50.4% |

| Cincinnati, OH | 83.4% | 80.1% | 77.7% |

| Cleveland, OH | 83.9% | 81.7% | 79.7% |

| Kansas City, MO | 81.2% | 76.0% | 73.7% |

| Las Vegas, NV | 61.9% | 51.7% | 47.8% |

| Columbus, OH | 78.0% | 74.4% | 72.0% |

| Indianapolis, IN | 80.4% | 76.8% | 74.5% |

| San Jose, CA | 24.8% | 19.1% | 15.8% |

| Austin, TX | 71.4% | 66.3% | 62.7% |

[1] At the time of writing, the average 30 year fixed mortgage rate for the U.S. was 4.63 percent

[2] Based on homes listed for sale on Zillow, at time of writing

[3] https://fred.stlouisfed.org/series/MORTGAGE30US

The post Rising Mortgage Rates Thorn in Otherwise Rosy Conditions for Home Buyers appeared first on Zillow Research.

via Rising Mortgage Rates Thorn in Otherwise Rosy Conditions for Home Buyers

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, December 26, 2018

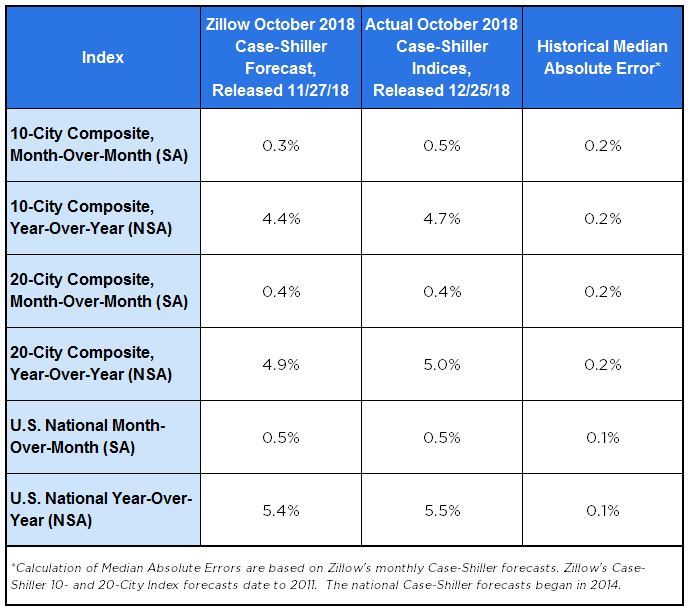

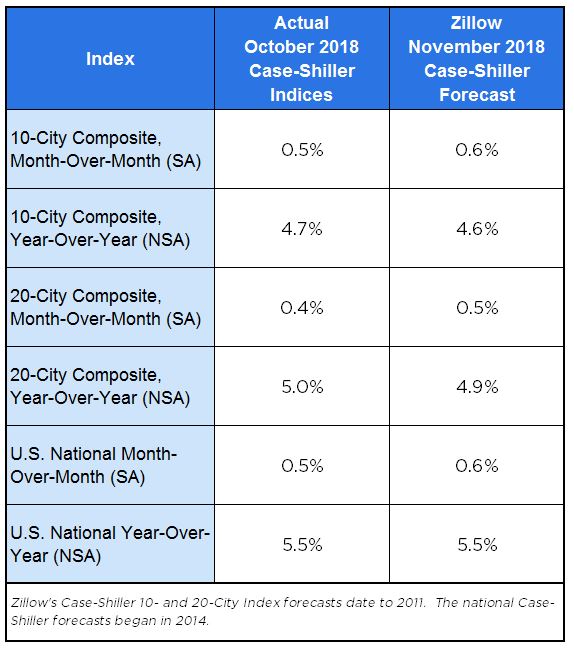

October Case-Shiller Results and November Forecast: Phoenix Replaces Seattle Among Top Three Home-Price Gainers

- The U.S. National S&P CoreLogic Case-Shiller Home Price Index - which tracks home prices - rose 5.5 percent in October from a year earlier, a hair above Zillow's forecast last month.

- The S&P CoreLogic Case-Shiller 20-city index climbed 5 percent annually in October, while the 10-city index rose 4.7 percent.

- Zillow forecasts a steady 5.5 percent annual gain for November.

Home prices were steady in October, gaining 5.5 percent year-over-year, the same as September, according to the Case-Shiller home price index. The gain was slightly above Zillow’s forecast, and we expect another 5.5 percent year-over-year increase in November.

Las Vegas led the 20-city index with an annual gain of 12.8 percent. San Francisco was next, posting a 7.9 percent year-over-year gain. And Phoenix replaced Seattle in the top three gainers, climbing 7.7 percent year-over-year in October.

The housing market slowdown that began in the second half of 2018 sets up a mixed bag for home buyers and sellers as we look at an uncertain 2019. Slowing home price appreciation can be read by many as an ominous sign – a kind of canary in the coal mine – for a more general downturn to come, but it's not necessarily an indicator that the sky is falling.

In fact, this slowdown could turn out to be more of a present for the market than a penalty. Would-be sellers that have ridden appreciation up over the past few years may choose to sell and capitalize on their recent gains as that upward ride slows – which will undoubtedly benefit buyers frustrated for years by limited inventory. And buyers themselves may find themselves with time to catch their breath and save for a home appropriate for them, rather than feeling like they're trying to hit a rapidly moving target in the face of faster appreciation.

There are tradeoffs, of course. If and when more sellers come out of the woodwork, the currently fierce competition among buyers may shift to sellers – a shift that has materialized more quickly than was anticipated at the start of this year. Listings with price cuts and longer time on market – already both growing – may become even more frequent. For the time being, this slowdown represents a return to fundamentals more than anything else, and to more balance between buyers and sellers.

The post October Case-Shiller Results and November Forecast: Phoenix Replaces Seattle Among Top Three Home-Price Gainers appeared first on Zillow Research.

via October Case-Shiller Results and November Forecast: Phoenix Replaces Seattle Among Top Three Home-Price Gainers

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, December 25, 2018

Mansion’s 10 Best-Read Stories of 2018

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

We Invite You to Cozy Up to These 9 Winter Wonderland Homes

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, December 24, 2018

How the Value of Your Home Affects How Much You Pay for College

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Please, Just Stop With These Holiday Decorations—We’re Begging You

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, December 21, 2018

Winter Might be the Best Time to Buy a House in Need of Renovation

In the market for a fixer-upper? This winter just might be the right time for you!

An argument could be made that winter is a bad time to shop for a home. It’s cold out, which makes house hunting a drag. And the trees and grass don’t look quite as pretty as they did a few months ago. When you really think about it, however, these issues could be good things! Here’s why.

Competition Falls Off

Ask any real estate professional, “When is the slow time?” and he or she is very likely to point a finger at wintertime. Once the holidays get rolling and the weather turns cold, the pace of showings and open houses tends to fall off significantly. People are far less likely to move when the kids are in school, and the holidays only serve to cement that reluctance.

Once the holidays get rolling and the weather turns cold, the pace of showings and open houses tends to fall off significantly.

If you’re willing to navigate winter challenges, you may find yourself at an advantage. Fewer buyers out there means sellers, short on offers, might be more willing to make a deal. Add to that the naturally smaller pool of buyers willing to look at fixer-uppers and the odds really might be more in your favor than they were in July.

Contractors Aren’t Booked Solid

Depending on where you live, the winter might be an easier time to find tradesmen to do smaller, fixer-upper type projects. In theory, the winter sees fewer large project starts in areas where it snows or freezes frequently. This temporary downturn in large projects can leave some highly skilled people with a few days available here and there. Those short little windows of availability can be just the amount of time needed to bang out smaller projects that come hand in hand with a handyman special.

Indoor projects are also more attractive to tradespeople during the winter. A carpenter who’s happy place most of the year is in building decks might be far more willing to take on your interior trim project when it’s single-digit temps outside!

|

|

|

Faster ROI on Green Building Projects

Energy efficiency is almost always on the short list of improvements for fixer-upper homes. A home that needs work rarely boasts the most recent technology. Old single-pane windows are leaking air, insulation is thin or nonexistent and the old HVAC systems is constantly breaking down while also consuming a fortune in energy costs.

If you live in a cold climate, winter can be a great time to see almost instant returns on energy efficiency projects. Just be cautious when asking about pricing because the law of supply and demand can come into play. When it gets cold outside, people tend to pay closer attention to those HVAC systems on their last legs and other green building-type issues. This can increase demand and raise prices. Do the math to be sure you don’t pay so much of a premium as to negate all of your energy cost savings.

The underlying premise here is no surprise. If you look for the opportunity in every situation, or every season, you can usually find it. As the seasons change and the weather turns cold for a few months, maybe there’s an opportunity in that for you. I hope you find it!

The post Winter Might be the Best Time to Buy a House in Need of Renovation appeared first on RE: Find.

from Winter Might be the Best Time to Buy a House in Need of Renovationhttps://http://bit.ly/2SfkG7c

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Amazon Effect in New York Will Reach Beyond Long Island City

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Marin County Magic! $39M Belvedere Mansion Is the Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, December 20, 2018

New Year’s Resolutions for Your Credit

The new year is a natural time to assess your life and set new goals. For many people, financial resolutions top the list of things they wish to improve in the coming year.

However, sometimes people overlook their credit as an important part of their financial health. Don’t make this mistake. If you haven’t already added any credit-specific goals to your new year’s resolutions list, here are a few to consider.

New Year’s Resolution #1: Evaluate Your Attitude Toward Credit

When it comes to overall financial health, your credit is a big deal. If you’ve been ignoring the importance of your credit or trying to avoid credit altogether in an attempt to stay debt free, your attitude toward credit may need to be reassessed, unless you are independently wealthy and can pay cash for homes and cars.

For starters, it’s important to understand that you don’t need to take on debt to earn good credit. In fact, the opposite is true. Credit scoring models reward you when you have less debt, no debt or low-risk debt, such as mortgages.

Earning and maintaining good credit will save you tens of thousands or even hundreds of thousands of dollars over the course of your credit lifecycle.

It’s also important to understand the money saving potential of good credit. Earning and maintaining good credit will save you tens of thousands or even hundreds of thousands of dollars over the course of your credit lifecycle. Savings opportunities range from lower interest rates to money saved every month on your insurance premiums. Point being: If you are spending less on interest and fees, you are able to redirect that money to something more meaningful to you and your family, like retirement accounts.

|

|

|

New Year’s Resolution #2: Monitor Your Credit Reports

Once you understand the importance of earning good credit, you need a plan to track your progress. Monitoring your credit scores is fine, but it is equally important to keep an eye on the data that is the basis for every single one of your credit scores, which is your Equifax, Trans Union and Experian credit reports.

It’s a good idea to review your credit reports every month. Credit reporting errors, simple mistakes and fraud can all occur from time to time. If incorrect information shows up on your credit reports, it could hurt your scores and potentially cost you time and money.

Thankfully, it’s easy and free to claim free copies of your credit reports online. If you haven’t already claimed your free annual reports from AnnualCreditReport.com, that’s a great place to start.

New Year’s Resolution #3: Improve Your Credit

Earning good credit doesn’t happen overnight, especially if you have made credit management mistakes in the past. Yet with the right plan and some dedication on your end it’s possible to begin improving your credit as soon as by next month.

Here are a few credit improvement strategies to get you started:

Stop Missing Payments Immediately

Roughly one third of the points in your FICO and VantageScore credit scores are driven from the presence or lack of negative information on your credit report. If you make all of your payments on time, none of the other more severe negative information, like defaults and collections, will ever appear on your credit reports.

Pay Down Your Credit Card Debt ...

... and then keep paying it off, every month. Roughly one third of the points in your FICO and VantageScore credit scores are driven from how you manage your debt. If you can limit the number of accounts that have balances and maintain lower balances on your credit cards, you’ll do fine in this category.

Don’t Apply for New Credit Unnecessarily

Every time you apply for credit, a credit inquiry will be posted to at least one of your credit reports. And while inquiries aren’t that problematic, they can lower your credit scores.

Be Patient

I know this isn’t normally realistic advice, but the age of your credit reports is an important factor in your credit scores. As your credit reports age, you’re going to earn more points organically. You can help this by not constantly opening new accounts, as they will drag down the average age of your accounts.

If you can do these things over and over, you really have no choice but to earn solid credit reports and scores. And the best news is that you don’t need a 850 FICO or VantageScore to get the best deals from lenders. If you can consistently keep your scores at or above 760, you will likely receive the best offer from any lender for any credit product.

The post New Year’s Resolutions for Your Credit appeared first on RE: Find.

from New Year’s Resolutions for Your Credithttps://https://ift.tt/2S8yRdX

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

What Housing Slowdown? Home Affordability Hits a 10-Year Low

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Mortgage Rates Hit a 3-Month Low With Home Buyers Biding Their Time

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Is Offerpad legit? An Atlanta Pro’s Honest Review

Source: Is Offerpad legit? An Atlanta Pro’s Honest Review

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Check-In Time: Rundown Motels Are Becoming Cool Condos, Affordable Apartments

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Inventory Climbs for Third Straight Month, But Don't Call it a Comeback (November 2018 Market Report)

- The number of homes on the market in November rose 0.4 percent from a year earlier, the third consecutive month of modest gains following nearly four years of inventory declines.

- In November, there were 1.6 million homes on the market – well below the 1.96 million homes for sale in December 2014, just before inventory started its multi-year plunge.

- Pricey metros that until recently clocked some of the fastest rising home values are now experiencing slower growth.

Low housing inventory, a major contributor to a runup in home prices in recent years, has risen for three consecutive months – but it is climbing at a slow rate, more akin to bumping along the bottom than growing in any meaningful way.

The number of homes on the market in November rose 0.4 percent from a year earlier, a small increase that follows a 2 percent year-over-year bump in October and a tiny 0.1 percent boost in September. The gains follow nearly four years of inventory declines that were far larger, including a nearly double-digit drop as recently as March 2018.

In November, there were 1.6 million homes on the market nationwide – almost 400,000 fewer homes than in December 2014, just before inventory started its multi-year plunge.

Roughly twice as many homes were for sale in the top third of the market (675,823) as the bottom third (334,857), squeezing buyers on a budget.

Sluggish inventory growth likely was influenced by a spike in mortgage rates in November, when rates hit their highest level since 2011. Higher rates can keep potential sellers at home, not wanting to trade into higher-rate mortgages. Rising rates also give some buyers pause, because they increase monthly mortgage payments.

Inventory fell in 11 of the nation's largest 35 metros, with biggest decline coming in Kansas City, Mo., where the number of homes for sale fell 14.9 percent. The largest inventory gains in November were along the West Coast, led by San Jose, Calif., with a 70.7 percent increase (to 2,902 homes for sale during the month). It was followed by San Diego (34.9 percent), Seattle (33.5 percent), San Francisco (33.4 percent) and Los Angeles (28.8 percent).

Home values cool in pricey markets

Pricey metros that until recently clocked some of the fastest rising home values are now experiencing slower growth.

Home value growth in the Seattle metro area, for example, continues to decelerate, slowing to 5.6 percent year-over-year in November – less than half the pace of growth clocked a year ago (12.5 percent in November 2017) and the slowest pace since December 2012. The median home value in the Seattle area is $486,400.

Similarly, the median home value in San Jose rose 11.2 percent, to $1.25 million in November, the highest median value among the largest 35 markets. But even that robust pace of appreciation was well below annual growth that topped 20 percent in seven months this year.

For the first time since September 2017, San Jose was not in the top spot for annual growth among the largest 35 markets. It posted the fifth-fastest annual growth, behind Las Vegas (13.9 percent), Atlanta (13.3 percent), Indianapolis (12.7 percent) and Charlotte, N.C. (11.5 percent).

The median U.S. home value climbed 7.7 percent – in line with its growth rate all year.

Rents are picking up again

Median U.S. rent rose 0.5 percent in November from a year earlier, up $7 to $1,449 a month – a small boost that follows two consecutive months of declines.

Among the largest 35 metro areas, the largest annual gain was in Orlando, Fla., where median rent climbed, 4.4 percent or $62 to $1,472 a month. The greatest drop was in Portland, Ore., where median rent fell 2.4 percent or $46 to $1,846 a month.

The post Inventory Climbs for Third Straight Month, But Don't Call it a Comeback (November 2018 Market Report) appeared first on Zillow Research.

via Inventory Climbs for Third Straight Month, But Don't Call it a Comeback (November 2018 Market Report)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, December 19, 2018

3 Smart End-of-the-Year Money Moves

The end of the year is fast approaching, and before you know it, 2019 will be here. Before you pull out your confetti and champagne to ring in the New Year, consider a few of these smart money moves.

Flexible Spending Account – Use It or Lose It

If you work for a company, you most likely have access to a Flexible Spending Account (FSA). These accounts are a popular way to save pre-tax dollars that you can use throughout the year for healthcare expenses. In 2018, you can save $2,650 in an FSA, and in 2019 that amount increases to $2,700.

|

|

|

FSAs are great if you know you’re going to have significant healthcare costs throughout the year. However, you should be careful with what you save in an FSA. Whatever you don’t use in each year goes away at the stroke of midnight on January 1, 2019, and you start all over again. For that reason, if you find yourself with some money lingering in your FSA, it’s time to go shopping.

What can you buy? There are over 4,000 products you can purchase with FSA funds, and the FSA Store is a good place to shop (yes, a whole online store where you can spend your remaining FSA funds). Here are some examples to consider.

- Sunscreen

- First-aid kit

- Vitamins

- Ovulation tests

- Condoms

- Over-the-counter drugs

- Travel essentials

- Acne treatment

Budget Like a Pro

Budgeting has a bad rap. It’s time to stop looking at your budget as something that tells you what you can’t spend money on, and start looking at your budget as a tool to help you achieve your goals. You’ve got stuff you want to do in life — buy a house, move abroad, start a business, etc. — and those amazing goals need a plan of action to achieve them.

Don’t wait until the new year to start tracking your money. There are lots of great mobile apps and programs that can help you step up your budgeting game in 2019. Here are some favorite budgeting apps:

If an app isn’t your thing, there are plenty of budget templates in Microsoft or other platforms that you can use to track your spending. There’s also nothing wrong with using paper and pen to create your budget each month.

Put Your Bonus to Work

Consider yourself lucky if you receive an end-of-the-year bonus check from work. Those checks are always a welcome surprise, even if the IRS gets a hefty chunk of your check. Before you go out and blow your bonus check, consider putting that money to work for you.

Make an Extra Contribution to Your 401(k)

If you haven’t maxed out your contributions for 2018, why not make an additional tax-deductible contribution for the year?

Fund a Roth IRA

You can contribute up to $5,500 in 2018 in a Roth IRA, and it’s a great way to supercharge your retirement. Plus, any contributions you make to a Roth can be withdrawn penalty and tax-free at any point in time.

Invest in Your House

Maybe you need a new roof, or you want to get a Food Network-worthy kitchen. Invest your bonus in house renovations or projects that give you the best bang for your buck, like bathrooms, kitchens, windows and curb appeal projects.

The post 3 Smart End-of-the-Year Money Moves appeared first on RE: Find.

from 3 Smart End-of-the-Year Money Moveshttps://https://ift.tt/2UV1du8

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

What on Earth Is ‘Cwtch’? The Warmest, Fuzziest Design Trend to Date

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Washington’s Most Expensive Home Is $45M Art Collector’s Modern Masterpiece

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

December Fed Rate Hike: Recalibrating Expectations

- The U.S. Federal Reserve raised its benchmark interest rate by a quarter-point, to a target range of 2.25 percent to 2.5 percent.

- The Fed rate hike was the fourth such rate increase in 2018.

The Fed's decision to raise interest rates for a fourth time this year was expected given the overall strength of the economy, even as the U.S. stock market is in the midst of its worst December in recent memory. More importantly, the Fed's comments make clear that central bankers are in the process of resetting market expectations for 2019: If economic data come in strong, we should expect a steady path of hikes in 2019. But if macro data turn out surprisingly weak, then the Fed is likely to pause.

Longer-term lending rates, including mortgage interest rates, aren't directly tied to the short-term rates that the Fed targets, but they often move in the wake of these hikes, and mortgage rates have risen nearly 100 basis points since the start of 2018. Over the course of the year, long-term rates have increased by less than might have been anticipated given the increase in short-term rates – a relationship that his historically signaled fears of a broader economic downturn. That means home shoppers have been spared from what could have been a potentially much more dramatic dent in affordability.

Still, home shoppers will have to recalibrate their home-buying budgets since the historic low rates of the past few years, if they haven't already. That lowered price point comes with tradeoffs, though, as inventory is up and price cuts are becoming more common, allowing home shoppers the opportunity to be a bit more strategic. Over time, however, that diminishing buying power can put even more stress on demand for less-expensive homes – where inventory already is lowest – and send prices higher at those most affordable price points.

The post December Fed Rate Hike: Recalibrating Expectations appeared first on Zillow Research.

via December Fed Rate Hike: Recalibrating Expectations

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

I Hate Barn Doors as Decor: Why It’s Time to Ditch the Farm Fashion

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

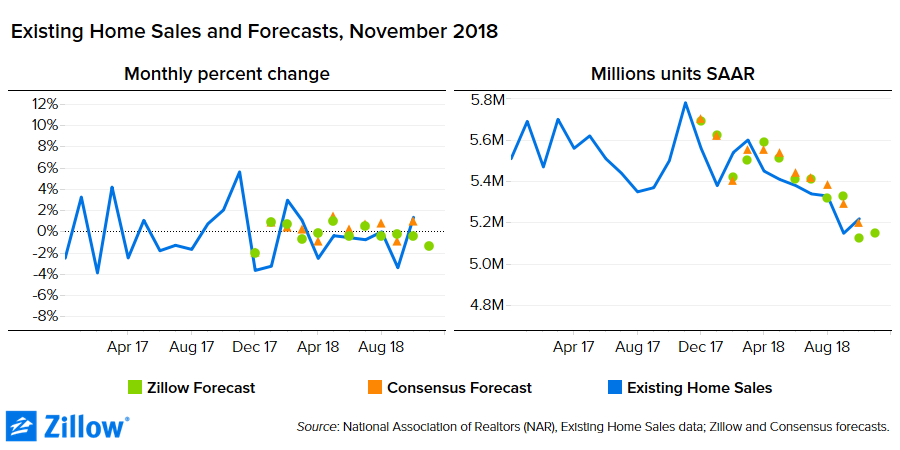

November Existing Home Sales: Signs of Life

- November existing home sales rose 1.9 percent from October to 5.32 million sales, according to the National Association of Realtors. Sales were down 7 percent from a year ago — when a rush of closings were pushed forward in advance of changes to federal tax laws that diminished some traditional and longstanding homeownership tax advantages.

- The median existing home sale price in November was $257,700, up 4.2 percent from November 2017. November's price increase marks the 81st straight month of year-over-year gains.

- Total inventory fell from October, to 1.74 million homes available for sale from 1.85 million, but was up from 1.67 million a year ago.

A small recovery in inventory beginning in September is paying some dividends as the year comes to a close, breathing some life into an existing sales market that has been pretty limp for much of 2018. Existing sales began flat lining two years ago, when tight inventory helped put the brakes on resale activity.

A volatile mix of rising mortgage interest rates, tax changes and an increasingly cloudy macroeconomic outlook heading into 2019 is introducing more than a little uncertainty into the minds of buyers and sellers alike, and it’s unknown how this will play out as conditions develop. On the one hand, affordability issues driven by consistently rising prices and fast growth in mortgage interest rates are clearly having an effect on many buyers budgets, especially at the ultra-competitive entry level. This affordability crunch is particularly acute in the pricey West, the only major region in which existing sales fell in November.

But taking a step back, it’s clear that rising rates aren’t impacting everyone the same — and it can be too easy to confuse “higher” rates with “high” rates. Rates on a 30-year, fixed mortgage are currently hovering around 4.6 percent, which is up almost 100 basis points from recent lows, but remains incredibly low historically speaking, and is still helping to keep monthly payments in check on increasingly expensive homes. Still, buyers no longer seem as automatically willing to pay the sticker price on a home, and the share of homes listed with at least one price cut is growing rapidly.

The most affordable markets continue to offer healthy gains, but in markets where price growth has long outpaced gains in income and where affordability is already stretched, buyers and sellers alike are both starting to adjust their expectations. There is no doubt that the housing market is moving toward a phase where there is more uncertainty for both buyers and sellers, and where above-market gains are no longer guaranteed. And with the scars of a decade ago still fresh for many, this newfound uncertainty can be disorienting.

The post November Existing Home Sales: Signs of Life appeared first on Zillow Research.

via November Existing Home Sales: Signs of Life

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, December 18, 2018

These Most-Viewed Homes of 2018 Are Still for Sale

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

2019 Design Forecast: What's In, What's Out

As we flip to the last pages of our 2018 calendar, it’s time to look at interior design trends on the rise - and say goodbye to those on their way out in 2019.

Here are our predictions about what’s in and what’s out in the year to come.

What’s in

Warm modernism

It’s official - many regions throughout the U.S. are choosing a modern aesthetic over a rustic style.

While black-and-white contrast and raw materials like steel and wood will continue to be popular, they’ll be softened by color and asymmetry. These modern elements will have a fresh approachability when surrounded by sun-soaked fabrics and natural wallcoverings.

Effortless technology and transformations

Talk-to-me tech products help you get things done with your voice, and homeowners are using them to modernize their daily routine.

In 2019 you’ll see smart faucets, fans, window coverings and appliances paired with popular platforms - Google Home, Amazon Alexa and Apple HomePod - for a convenient, connected home.

Additionally, products that offer easy installation and seamless integration into existing layouts make projects remodel-friendly. Innovative sinks, faucets, medicine cabinets, appliances and lighting provide a quick transformation to refresh the style and functionality of your space.

Om sweet home

Though talk-to-me tech is trending, some will be looking for ways to escape the chatter.

Meditative and sound-barrier features will appear in more homes this year - think transformative experiences using acoustic panels, colored lights and aura effects. Ethereal, sheer and translucent fabrics will support the aesthetic, pairing an organic feel with the benefits and convenience of select technology.

Industrial style

Concrete, quartz and metal lovers, rejoice! Industrial styles are predicted to rise in popularity in 2019.

Matte black and bronze continue to dominate and complement a more industrial vibe. But when selecting wall colors, appliances, faucet finishes and fabrics, consider the possibilities of moody blues and the gray color spectrum. From warm light grays to the coolness of matte black, these tones add a subtle layer of intrigue and distinction.

Plus, black and charcoal gray front doors could earn up to $6,271 more when selling your home!

Organic maker accents

Handmade details can immediately soften an interior. This year you’ll see rhythmic patterns and imperfect lines incorporated through hand-painting, stitching and detailing, expanding the possibilities for endless mixing and matching in the home. Additionally, fabrics and accents with strands of crystal, wooden and pearlescent beads present a sophisticated flair for artful detail.

Home decor favorites will still include earthy elements and nubby textures. Think neutral naturals by simply adding a wooden side table and sculpture, live and fake plants for color, and natural fibers through rugs and fabrics.

What’s out

Rustic

Is America finally over the “Fixer Upper” movement? Not quite, but the rustic, farmhouse-chic elements are getting refined.

The shiplap-crazy trend seems to be leaning toward a modern twist, simplifying layers of the look. Cutesy barn doors will take a backseat to more modern versions featuring glass and metal instead of reclaimed barn wood.

The signature statement range hood covered in rustic materials will swing to simplified finishes, like brushed brass, stainless and matte black. Lastly, the harsh light of the Edison bulb will move to a more complementary glow, reflecting concealed bulbs versus exposed ones.

Millennial pink

Bold, trendy color schemes are likely on the way out, with more subtle earth tones and cool, classic palettes on the rise.

Blues and neutrals continue to top Zillow trend reports, adding higher dollar values related to home sales when used in kitchen and bathroom areas. While millennial pink may have been all the rage on designer Instagram feeds, people don’t actually want to live with it throughout their homes.

Whether trends inspire you or not, it’s important to be aware of them, because they help shape our own personal interior style. If you love purple gingham in your dining room, go for it. If an all-white interior speaks to you, celebrate it.

Our homes are where we express ourselves and tell our unique style story, so I encourage you to do just that in the new year.

Related:

- 3 Design Tricks That Will Make Your Small Space Feel Big

- Quiz: What Type of Bar Should You Build in Your Home?

- A Park Slope Townhome That Went From ‘Mess’ to Masterpiece

via 2019 Design Forecast: What's In, What's Out

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

November Housing Starts: Canary in the Coal Mine?

- November housing starts rose 3.2 percent from October but were down 3.6 percent from a year ago, according to the Census Bureau.

- Housing permits rose 5 percent from October and 0.4 percent from November 2017.

- National housing completions rose 0.4 percent from October, but fell 3.9 percent from November.

The relative strength in building activity in November is welcome news after months of lackluster reports. But the topline numbers obscure some persistent weakness in the sector; much of last month’s growth was driven by the volatile multifamily segment, with single-family home building activity falling. Several economic indicators – notably the historically low national unemployment rate – paint a picture of a booming American economy, the residential construction market hit the pause button in 2018. And as it becomes more clear that the three headline construction indices – permits, starts and completions – all look to end 2018 on a sour note, speculation has already begun as to whether the construction industry is a macroeconomic canary in the coalmine signaling a larger shift to come. Permits and starts are down from a year ago, and completions are just barely higher – the end-game of projects begun months or years ago when the outlook was a bit rosier. This construction pullback is not due to lack of demand, and instead seems born out of builders' fears that it's almost impossible for them to profitably deliver new homes at a lower price points where that demand is strongest. Builders have struggled with rising labor, materials and land costs for years, and while materials costs have eased somewhat lately, labor costs have only surged higher. Rising mortgage interest rates, tax changes and an aging recovery have also snowballed, putting a meaningful dent in what buyers can afford to pay. Having turned a corner in 2018, the critical unknown for 2019 will be whether this builders' retreat will prove to be prescient or premature.

The post November Housing Starts: Canary in the Coal Mine? appeared first on Zillow Research.

via November Housing Starts: Canary in the Coal Mine?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Delicious Dwellings! 10 Homes for Sale That Look Exactly Like Gingerbread Houses

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, December 17, 2018

What Debt Collectors Can and Cannot Do

No one likes to pick up the phone to discover a debt collector on the other line. Debt collectors are those friendly folks tasked with collecting debts that you have not, will not or cannot pay. If you fail to pay back a debt as you initially agreed, debt collectors are most likely going to come calling.

If you’re in the unfortunate situation of having past due debts, the good news is that you can count on federal law to protect you from abusive debt collection practices. Debt collectors have a hard job and they certainly have the right to try to collect the money you owe. Still, that doesn’t mean they’re allowed to behave any way they wish when pressuring you to pay up.

Here is a look at some of what debt collectors can and cannot do, according to the Fair Debt Collection Practices Act (FDCPA).

What Debt Collectors Are Allowed to Do

Call and Write

Although you probably wish debt collectors would leave you alone, it’s not illegal for them to contact you via phone or mail. Debt collectors can even call you at work, unless you inform them that you’re not allowed to receive personal calls on the job.

|

|

|

Sue You and Force Payment

As long as they abide by debt collection statutes within the state where you resided when the debt was initially incurred, debt collectors can and often sue people for unpaid debts. To make matters worse, if a debt collector sues you and you ignore it, the court will enter a default judgment that may eventually grant the debt collector the right to forcibly take funds from you. Debt collectors are not allowed to threaten to sue you unless they intend to do so, so take them seriously.

Report Information to the Credit Reporting Agencies

Debt collectors can also put pressure on you to pay outstanding bills by reporting the negative information to the credit reporting agencies. As long as the information reported is accurate and doesn’t exceed the credit reporting statute of limitations, it is perfectly legal for them to do so in most circumstances.

What Debt Collectors Are NOT Allowed to Do

Attempt to Collect More Than You Owe

“Overbiffing,” or overstating your balance, is a debt collection practice that is prohibited by the FDCPA. Debt collectors are not allowed to misrepresent your account balance nor try to trick you into paying more than you owe. Several state AGs have come down hard on debt collectors who have practiced overbiffing.

Discuss Your Debt with Third Parties

It’s fair game for a debt collector to call your friends and family to try to find you, but they cannot disclose the nature of the call or discuss any debt you allegedly owe. This is formally referred to as “Third Party Disclosure” and it is illegal.

Harass You

Threatening you with bodily harm, intentional damage to your reputation or arrest are all things that might be considered harassment under the FDCPA. Such behavior is strictly off limits.

Call You at All Hours

Debt collectors are only allowed to contact you during reasonable hours, specifically between 8:00 a.m. and 9:00 p.m. in your local time zone, not their local time zone. If a debt collector calls you at midnight, that person has broken the law.

Should You Pay?

You should always pay your debts. It’s the right thing to do and will help you to maintain a solid credit report and credit scores. Most people don’t take on debt with the intention of avoiding it. You probably intended to make every payment on time, but sometimes unfortunate circumstances or even plain bad planning leads to a situation where you owe more than you can afford.

Nonetheless, your debts aren’t going to go away simply because you can’t afford them unless you qualify for and eventually file for bankruptcy protection. If a debt is legitimate, you should try to find a way to pay it.

The post What Debt Collectors Can and Cannot Do appeared first on RE: Find.

from What Debt Collectors Can and Cannot Dohttps://https://ift.tt/2EAGLKg

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

5 Christmas Decor Fails to Never, Ever Try at Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Forecast for Existing and New Home Sales (November 2018)

Existing home sales caught a much-needed reprieve in October, posting a month-over-month increase for the first time since March. It was not enough, however, to break a string of year-over-year declines in home sales – the longest extended period of annual declines since the 2013-14 Taper Tantrum.

We expect sales to revert to a more typical recent pattern in November, falling 1.4 percent from October to 5.15 million units at a seasonally adjusted annual rate (SAAR), down 10.1 percent from November 2017.

The National Association of Realtors (NAR) will report existing home sales on Wednesday, December 19.

While existing home sales have suffered from supply side constraints for the past three years, new home sales are facing more recent headwinds. They had been steadily increasing until late 2017, but have now been on a precipitous slide for the past year. October new home sales posted their slowest pace since early 2016 and have now undershot forecasts for five consecutive months.

We expect another disappointing month for new home sales in November with sales up 2.7 percent from October to 559,000 (SAAR), but down 21.5 percent from November 2017 – the recent high mark when 711,000 new homes were sold.

The U.S. Census Bureau will report new home sales on Thursday, December 27.

The post Forecast for Existing and New Home Sales (November 2018) appeared first on Zillow Research.

via Forecast for Existing and New Home Sales (November 2018)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

How Christmas Decorating Can Help You Identify Next Year’s Home Maintenance Checklist

As you decorate and undecorate for the holidays this year, pay attention to some of the details surrounding your decorations. Make a home maintenance checklist. Take some pictures. Put the repairs on your 2019 renovation calendar and in your 2019 budget. Do that, and next year you may feel confident enough to enter your home in the local decorating contest.

1. Roofing and Overhangs

As you install and uninstall those holiday lights, you’ll have the perfect opportunity to get a close look at your roof and overhangs. Your overhang includes three main components: the soffit, the fascia and the gutter.

The soffit, which is the underside of your overhang and is usually wood or metal, might have some loose pieces, some holes critters could get in or water damage from a roof leak above.

You’re already up on a ladder or on the roof itself to do the lights. Take a good look at the gutters while you’re there.

The fascia is the flat board around the perimeter of your overhang and is usually where the lights themselves are installed. Fascia boards rot, come loose and are notorious for needing a paint job far sooner than the rest of your home.

The gutters are self-explanatory, I suppose, but there’s no better time to check them for clogs, loose nails or broken corners. You’re already up on a ladder or on the roof itself to do the lights. Take a good look at the gutters while you’re there.

Speaking of the roof, holiday decorating time is probably one of the few times you actually get on your roof, which should always be done with great care and proper safety measures. But if you are safely up there, you should get a look at your roofing. How are your shingles? Do you see any dips in the roof that might indicate a soft section of underlayment? This usually means a leak is present.

No matter what part of your exterior you’re looking at, the installation and removal of holiday lighting is a chance to inspect your home closely. Take it!

2. Front Door and Entryway

Good cheer starts at the front door. Giant wreaths hung carefully on a door flanked by bright red poinsettias is about as inviting as an entryway can get, don’t you think? The front entry sets the tone for the feel of your house. It’s worth the effort during the holidays and all year round. Focus on the details and go big on the warm holiday welcome!

Does your door need a new coat of paint or varnish? Are all of the porch lights working properly? Does the landscaping on either side of the front walk need to be revamped? Add these items to your list so that, come next holiday season, your house really does offer a warm welcome.

3. Fireplace

Fireplaces are probably the most commonly decorated component in a home. If you have a fireplace, chances are you’ve decorated it even if you haven’t put up a single string of lights. Everyone loves a decorated mantel and hearth.

Interestingly, fireplaces are also a common source of accidents. From unwanted smoke and mantles falling off to actual fires where they aren’t supposed to be, fireplace maintenance shouldn’t be ignored.

Take the decorating process as an opportunity to check a few things:

- Do the firebox glass doors and/or screen work properly and seal well?

- Does the chimney itself need to be swept?

- Is the mantel securely fastened to the wall?

- Are there any loose stones, bricks or tiles on the hearth or the face of your fireplace?

Add these to your 2019 to-do list so that next year your fireplace looks as hot as it actually is inside!

4. Railings and Banisters

Along the same lines as loose fireplace mantels, loose railings and banisters can represent a real safety hazard. This danger can sometimes be made even worse through the process of adding and removing holiday decorations.

The good news is that the running of garlands around all of your stair and balcony railings pretty much requires someone to put their hands on every section of your railing assembly. Take care to note those spindles that are broken or missing, those newel posts that are wobbly and the like. A good carpenter can usually fix these things without too much trouble and the improvement in look, functionality and safety are worth every bit of effort.

5. Electrical

Last but not least is electrical. Every Christmas tree fire I’ve ever seen has been caused by some sort of electrical issue. Holiday decorations, especially lights, take up electrical outlets all around your home inside and out. Are breakers tripping when they shouldn’t be, or more importantly, are they not tripping when they should be? If you’ve got far more plugged into one outlet than it should be able to handle but it still works, that could be a sign of a dangerous condition in your electrical system.

As you install and subsequently remove electrically powered holiday decorations this year, look for things like loose outlets, switches that don’t seem to connect every time, outdoor outlets that aren’t properly waterproofed and other potential electrical hazards. You really can’t be too careful.

Holiday Showcases are About Details

No matter what your level of decoration is this year, or where you hope for it be in the years ahead, the real difference is in the details.

Take the time to look closely at the permanent parts of your home that surround and support the decorations you’re enjoying during the holidays. This is your chance to make your list and check it twice so that next year your home is perfectly ready to win the blue ribbon in your local holiday home decorating contest.

The post How Christmas Decorating Can Help You Identify Next Year’s Home Maintenance Checklist appeared first on RE: Find.

from How Christmas Decorating Can Help You Identify Next Year’s Home Maintenance Checklisthttps://https://ift.tt/2QAxVT6

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Artsy Southern Town That Wants to Be the Next Portland

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

10 Cities With the Most Homes Under $200K—You Won’t Believe Where They Are

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, December 14, 2018

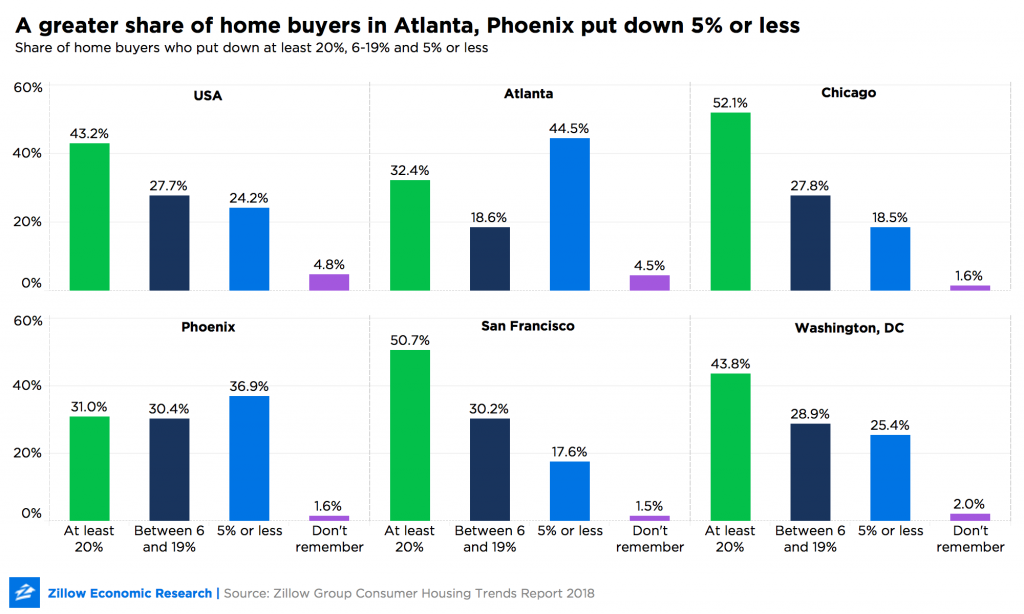

Atlanta and Phoenix Home Buyers Have Smaller Down Payments

- Nationally, 43.2 percent of buyers put down 20 percent, a longstanding benchmark.

- 24.2 percent of buyers put down 5 percent or less. The share is much higher in Atlanta, where 44.5 percent of buyers put down 5 percent or less, and Phoenix, where 36.9 percent do.

- Atlanta and Phoenix also have the smallest share of buyers who put down 20 percent or more when they bought a home. In Atlanta, it's 32.4 percent and in Phoenix, 31 percent.

With mortgage rates rising, the size of a down payment takes on even greater importance. It can make the difference between a monthly mortgage payment that's affordable and one that stretches a household's budget too thin. In the Zillow Group Consumer Housing Trends Report 2018, we asked home buyers nationally and in five major metro areas – Atlanta, Chicago, Washington, D.C., Phoenix and San Francisco – about their down payments, including how much they put down and where they got the money.

The down payment trends reflect home value differences across the metros, giving potential buyers a sense of how buying happens in their areas. For people in particularly competitive markets, it's an informational edge to know what you're up against and how others are handling what may be the largest investment of their lives.

A notable difference among the five metros is how much mortgage buyers put down – and how that compares to the national trend.

Nationally, 24.2 percent of buyers put down 5 percent or less. The share is much higher in Atlanta, where a whopping 44.5 percent of buyers put down 5 percent or less, and Phoenix, where 36.9 percent do. The median mortgage payment in both metros is $1,131 a month, which is lower than the median mortgage payments in Chicago ($1,336), Washington, D.C. ($1,850), and San Francisco ($2,158).[1]

Atlanta and Phoenix also have the smallest share of buyers who put down the traditional 20 percent or more when they bought a home. In Atlanta, it's 32.4 percent and in Phoenix, 31 percent.

Interestingly, buyers in the three metros with higher monthly mortgage payments are more likely to put down 20 percent or more. In Chicago, it's 52.1 percent of buyers; in San Francisco, 50.7 percent of buyers; and in Washington, D.C., 43.8 percent. All three are above the national share of 43.2 percent of buyers who put that much down.

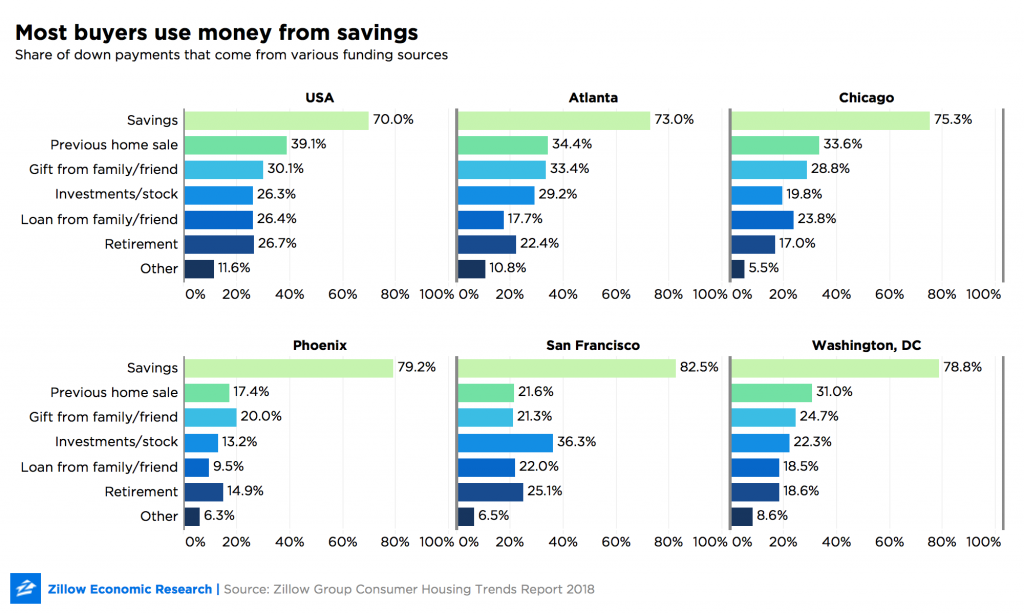

Most home buyers in the United States and each of the surveyed metros used savings for their down payments. For the U.S. as a whole, 70 percent of mortgage buyers use at least some savings for their down payments. In all five major metros that we examined, the share was similar or greater: 82.5 percent in San Francisco, 79.2 percent in Phoenix, 78.8 percent and Washington, D.C., 75.3 percent in Chicago and 73 percent in Atlanta.

After savings, previous home sales are the second most common source of funding for the average American down payment – a trend that holds in Atlanta, Chicago, and Washington D.C.

In San Francisco, investments come in second – with 36.3 percent of buyers using that source, the largest share of most metros examined and somewhat higher than the 26.3 percent of buyers nationally who put the sale of investments toward a home purchase.

In Phoenix, a gift from family and friends come in second: 20 percent of buyers there rely on that help from loved ones. Only 17.4 percent draw on proceeds from previous home sales — lower than the national average of 39.1 percent.

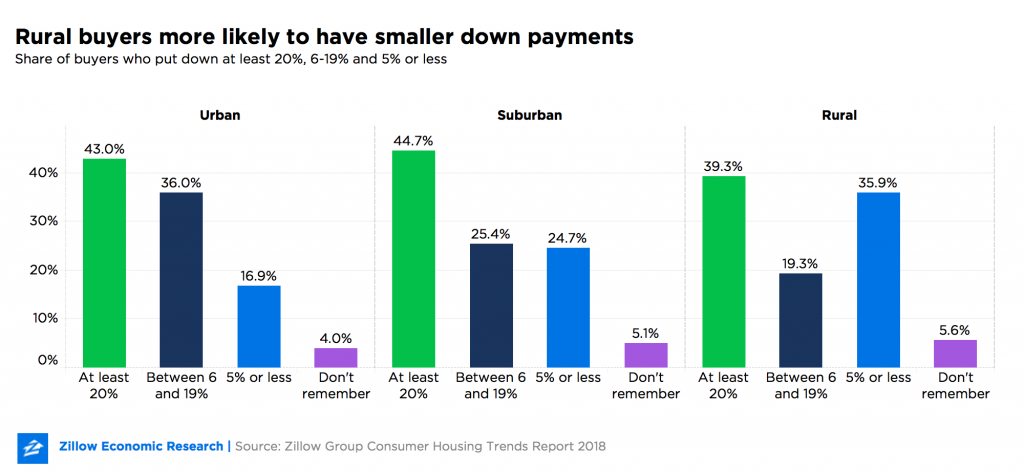

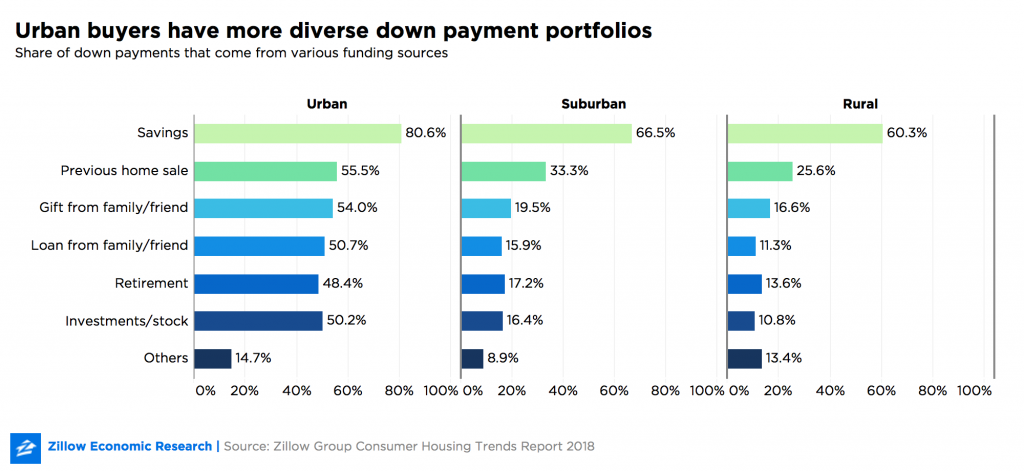

When making a down payment, 35.9 percent of rural buyers put down 5 percent or less. Comparatively, only 24.7 percent of suburban buyers and 16.9 percent of those buying homes in urban parts of the country do the same.

Putting down 20 percent or more is similar across urbanicity, but urban and suburban buyers are more likely to make down payments between 6 and 19 percent. In fact, 36 percent of urban buyers and 25.4 percent of suburban buyers do this, compared with 19.3 percent of rural buyers.

In general, urban buyers draw from a more diverse portfolio of funding than their rural and suburban counterparts. Savings still top the list: 80.6 percent of urban buyers finance at least part of their down payments with it. Additional sources include the sale of a previous home (55.5 percent), a gift from family or friends (54 percent), a loan from family or friends (50.7 percent), stock or other investments (50.2 percent), and drawing from retirement (48.4 percent). Buyers in Atlanta, Chicago, Washington, D.C., and San Francisco tended to have more diverse down payment portfolios than their rural American counterparts. Phoenix, on the other hand, was similar to rural America.

[1] Zillow analysis of the U.S. Census Bureau, American Community Survey, 2017 in inflation-adjusted 2018 dollars.

The post Atlanta and Phoenix Home Buyers Have Smaller Down Payments appeared first on Zillow Research.

via Atlanta and Phoenix Home Buyers Have Smaller Down Payments

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

King of the Clicks: What Was the Most Popular Home of 2018?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, December 13, 2018

Creative Ways to Give Money

We’ve all received those gifts that require a fake smile and public appreciation. Some gifts get re-gifted in the hope that no one will notice. Don't want to be one of those gifters? These money-centric gifts — great ways to invest in a loved one's future — are more thoughtful than simply stuffing cash in an envelope.

Give for College

It’s hard to believe, but the average cost of a four-year private college in 2018 hovers around $32,000 a year. Affording college is no small feat and students can use all the help they can get to fund their degrees.

A 529 college savings plan has become a popular way for parents, grandparents and friends to help fund a child’s college education. These plans vary from state to state, with some states offering tax incentives, however, all 529 contributions are not tax-deductible.

|

|

|

One way you can give the gift of college is to set up a 529 account for that special child in your life. Companies like Collegebacker make giving the gift of college simple and easy. Within a few short minutes, you can set up an online account and designate a one-time or monthly funding amount and easily track a student's college savings.

Give to the New Investor

Why not help someone fund his or her financial future this holiday season? Two popular ways to give to a new investor include funds for a Roth IRA contribution and a gift card towards an Acorns investing account.

Roth IRA

If the gift receiver has earned income, you can gift money towards a Roth IRA contribution. The maximum contribution for 2018 is $5,500; however, you can gift any denomination up to the amount of earned income for 2018. For example, if the gift receiver earned $3,000 babysitting or freelance writing, you can gift up to $3,000. You can set up a Roth IRA at nearly every investment house, including Vanguard, Fidelity, and Betterment.

Acorns

An Acorns account is a great gift idea for a new investor who is looking to dip his or her toes into investing. Acorns is a mobile app that allows you to invest in portfolios that match your risk tolerance. Acorns was built on the concept of investing your spare change to grow your wealth over time. Acorns offers gift cards for the holiday season so you can give the gift of investing in $25 denominations.

Give Credit Card Rewards

Rather than using your credit card rewards yourself, why not gift them this holiday season? In fact, 31 percent of credit card holders aren’t redeeming their miles and rewards every year and let those miles go to waste. However, credit card rewards are worth value and can be redeemed for lots of gift giving options.

• Plane tickets

• Car rental

• Hotel stays

• Gift cards for restaurants, movies and stores

• Cash back

• Entertainment, such as concert tickets

Make a list of all your rewards credit cards and then check your balances and the reward options available to you. Gifting your rewards is a great way to give money and help fund a goal.

There are lots of creative ways to give money this holiday season. Think outside the box and give money that will help fund someone’s financial future — or at least, give that person a healthy boost to get started funding his or her money goals.

The post Creative Ways to Give Money appeared first on RE: Find.

from Creative Ways to Give Moneyhttps://https://ift.tt/2UE3Pwm

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

How to Enjoy Christmas on a Budget

Remember when you were a kid, and you anxiously waited for the sun to rise so you could go and see what Santa brought you? Counting the presents under the tree, you just knew it was going to be your best Christmas yet. Those feelings of excitement during the holiday season never seem to vanish no matter how old we are.

Christmas can also be a time of hardship if you are living paycheck to paycheck and trying to make ends meet. No matter what your bank account situation is this Christmas, there are lots of ways to celebrate the season and stay within your budget.

|

|

|

Budget for Success

When you’re on a budget, the last thing you want to hear is that you need to make another budget. However, putting together a list of who you need to buy gifts for and how much you want to spend per person is a great way to make sure you don’t overspend. Start with how much you can spend in total and then break that number down based on who you’re buying gifts for.

There are lots of Christmas budget apps to keep you within your spending limits:

The Christmas List

A free IOS app, The Christmas List app lets you set a budget for each person on your list and then keep track of how much you’ve spent — all in the palm of your hand.

Giftster

A free IOS and Android app, Giftster also lets you create a list for each person or group you are buying gifts for and track how much you’ve spent. You can also have each person provide links to the gifts he or she wants the most and easily purchase the gifts through Gifster.

Hint: If you plan to use a credit card for your holiday shopping, call the credit card company before you make your first purchase. Ask for an interest rate reduction if you know you won’t be able to pay off the credit card bill within 30 days. When you’re using a credit card, the lower the interest rate, the better off you are to ensure you won’t be overpaying for your gifts.

Use What You’ve Got

When you’re on a budget this holiday season, you’ve got to think outside the box and use what you’ve got to maximize your gift giving. There are some clever ways to put a little extra cash in your bank account this holiday season.

Credit Card Points

They are worth value and many people overlook their credit card reward points. Depending on your credit card, points can often be redeemed for things like airfare, hotel stays, car rental, cash back and even gift certificates to be used at stores and restaurants.

Unused Gift Cards

Do you have a stack of unused gift cards laying around that you haven’t used? You can turn those into cash with companies like Raise and Cardpool that you can use on Christmas gifts. Most companies offer 80 to 90 percent of the value of the gift card in cash.

Negotiate

You can negotiate many of your common bills to save extra money that you can use for your Christmas budget — think bills like your internet, cell phone and cable bills. It’s not uncommon to be on a plan that is old and outdated and with one call to the company you can move onto a better plan that is less expensive. Use the money you save to help fund your Christmas gifts.

Christmastime doesn’t have to be a time of stress. There are lots of ways to manage Christmas on a budget with a little forward thinking and some ingenuity working with what you’ve got available to you. Always remember that it’s the giving spirit that counts and not the gift itself.

The post How to Enjoy Christmas on a Budget appeared first on RE: Find.

from How to Enjoy Christmas on a Budgethttps://https://ift.tt/2Bg6IL5

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Warm Up to $29.5M Opportunity in Coral Gables, the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Sugar-Sweet Gingerbread-Style Homes for Sale, ‘Cause It’s the Holiday Season

It’s all about the trim! In the late 1800s, homeowners used what came to be called gingerbread trim to dress up otherwise pretty basic-looking homes. Pierced frieze board, scroll-sawn brackets and balusters — the more frills and geegaws, the better.

During this holiday season, we thought we’d take a look at homes on the market that showcase gingerbread folk architecture. Which one is your favorite?

Bristol, Rhode Island

Year built: 1850

What we love most: The living room boasts a working fireplace and floor-to-ceiling windows, plus period woodwork has been preserved. Learn more about this three-bedroom home.

|

|

|

|

|

|

|

|

|

|

|

|

|

Bennington, Vermont

Year built: 1870

What we love most: This urban farmhouse is within walking distance of all the cool stuff in town. Plus, the wraparound porch, wide-plank floors and exposed brick details harken to times gone by. Learn more about this lovely single-family home.

|

|

|

|

|

|

|

|

|

|

|

|

|

Hooversville, Pennsylvania

Year built: 1895

What we love most: Where do we start? The tree-lined lot, the 10-foot ceilings and the absolutely adorable covered porches to enjoy the changing seasons! Learn more about this blue beauty.

|

|

|

|

|

|

|

|

|

|

|

|

|

Bridgeton, New Jersey

Year built: 1890

What we love most: All dental molding is original, but interiors have been updated to suit a modern family. The home includes both front and back porches to enjoy picturesque farmland and an Amish-built two-car garage (so you know it will last forever). Learn more about this country home.

|

|

|

|

|

|

|

|

|

|

|

|

|

Troy, North Carolina

Year built: 1905

What we love most: Original woodwork and doors remain intact! And we can't get enough of that cantilevered staircase and lion head/lion paw mantle. The home does need work — the right person could put his or her signature touch and make this a family home for multiple generations. Learn more about this grand Queen Anne.

|

|

|

|

|

|

|

|

|

|

|

|

|

Tampa, Florida

Year built: 1991

What we love most: You get the look of a bygone era with all the modern and energy efficient features of new construction. This home comes with a porch swing and enough space in the backyard to host some pretty fun summer parties. Learn more about this shotgun bungalow.

|

|

|

|

|

|

|

|

|

|

|

|

|

Greenville, Alabama

Year built: 1900

What we love most: The fireplace mantel is quite striking and the gingerbread trim makes this home look almost like a confection. Interiors require TLC, but an experienced DIYer could whip this home into shape in no time flat. Learn more about this quaint cottage.

|

|

|

|

|

|

|

|

|

|

|

|

|

Greenup, Kentucky

Year built: 1870

What we love most: Views of the Ohio River from this home are simply spectacular. Known as the McKee House, this grand lady is listed on the National Register of Historic Places and boasts gardens, a gazebo and even its own boat dock. Learn more about this six-bedroom home.

|

|

|

|

|

|

|

|

|

|

|

|

|

Fredericksburg, Texas

Year built: 1847

What we love most: The home started its life as a one-floor dwelling. When German immigrant Frederick Kuenemann purchased the home, he added on to accomomdate a growing family. This building is an important Texas landmark. Learn more about the "German Jewel."

|

|

|

|

|

|

|

|

|

|

|

|

|

Ferndale, California

Year built: 1894

What we love most: This place, coined the Gingerbread Mansion, has served as a hospital, tenement and private home during its long life. Most recently a bed and breakfast, the property boasts beautiful English-style gardens. Learn more about this Northern California beauty.

|

|

|

|

|

|

|

|

|

|

|

|

|

The post Sugar-Sweet Gingerbread-Style Homes for Sale, ‘Cause It’s the Holiday Season appeared first on RE: Find.

from Sugar-Sweet Gingerbread-Style Homes for Sale, ‘Cause It’s the Holiday Seasonhttps://https://ift.tt/2LfxyaC

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.