Applications for home purchase loans improved slightly on the week, halting a streak of four straight weekly declines. Safety concerns related to the pandemic may be contributing to increased rates of people quitting their jobs. And durable goods orders rose strongly in September, another good sign for the manufacturing sector.

For-purchase mortgage applications stop their four-week slide

A seasonally adjusted reading of applications for home purchase loans increased by 0.2% in the week ending October 23 from the week prior, according to the Mortgage Bankers Association

The index had fallen slightly for each of the last four weeks

The pandemic is causing some people to consider leaving their job

A new poll conducted by the Associated Press-NORC Center for Public Affairs Research suggests that a quarter of current U.S. workers have considered quitting their jobs due to fears pertaining to the pandemic

About 20% of workers have had to take leave as a result

Factory orders increased strongly in September, but rising cases threatens this momentum

Orders for durable goods rose 1.9% in September from August

But durable goods orders are still well below pre-pandemic levels and rising case counts threaten this growing optimism

So what?

Applications for home purchase loans had fallen on a weekly basis for four consecutive weeks before today's announced modest weekly improvement. Today's release wasn't a blockbuster – the weekly improvement was minuscule – but it reinforced that homebuyer demand remains robust heading into the fall. Despite the four weekly declines, application activity pertaining to home purchase mortgage loans remains near its highest level in the last 12 years and 24% above last year's levels. This enduring homebuyer activity comes as inventory levels continue to plummet and price continue to spike. In the week ending October 17, there were 37% fewer homes on the market than there were in the same week last year,according to Zillow Economic Research, and the average purchase loan size that was applied for last week was $372,600 – a new all-time high.

Recent reports on labor turnover – the number of people entering or exiting employment or the labor force and the reasons why they're doing so – have highlighted what's usually an encouraging trend: more people are quitting their jobs. Quits are generally viewed as evidence of a strong or strengthening labor market, suggesting that people are sufficiently confident in their ability to find new employment that they decide to pass on their existing job, though there's reason for skepticism in the current environment. The number of people voluntarily leaving their roles fell slightly in August from July, but the level has increased by about 50% since a low in April. A new report suggests that the recent increases in quits may not be occurring for healthy reasons after all. A poll conducted by the Association Press-NORC Center for Public Affairs Research suggests that a quarter of current U.S. workers have considered quitting their jobs due to worries related to the pandemic, and about 20% of U.S. workers have had to take leave as a result. Lower income households – those making $30,000 or less annually – were disproportionately more likely to express these concerns. The report also showed a divide across genders. Half of women feel the pandemic is a major source of stress, compared to just 36% of men. All told, the report suggests that voluntary job losses may have been due to unhealthy factors such as safety concerns and childcare responsibilities, rather than people finding a better job.

In another sign that the economy is finding its footing, seasonally adjusted orders for durable goods – products that are designed to last at least three years, often in factories – increased 1.9% in September from August. New orders for nondefense capital goods excluding aircrafts – a widely cited proxy for business investment – grew 1% on the month. Both series were above consensus expectations. The report was the latest piece of encouraging news for the manufacturing sector in recent weeks – the IHS Markit Purchasing Managers Index, released last week, showed that activity in the manufacturing sector was growing at its fastest pace since early 2019. But recent strong upticks in coronavirus cases threaten this mounting optimism. As global case counts rise across the globe, demand for goods may wane and supply chain issues may worsen from their already delicate state.

Click here to read past editions of Zillow’s Market Pulse updates.

When it comes to horror flicks, there’s nothing Hollywood loves more than a towering Victorian manse that’s a bit past its prime. After all, there’s a reason Ryan Murphy set the inaugural (and scariest) “Murder House” season of “American Horror Story”in a sprawling (and spectacularly haunted) Victorian home. Alfred Hitchcock situated Norman Bates and his irascible mom in one for “Psycho.” Even Walt Disney understood the Victorian’s freaky allure—that’s why Disneyland’s Haunted Mansion is built in the same inescapable and inescapably unnerving style.

“It has a lot to do with the proportions,” says Jonathan Moore, an architect in Tampa, FL. “Many of the details—like doors, windows, and trim—are long and vertical.” Remind you of anything?

“There’s a direct relationship to an open mouth and wide eyes.” A screaming mouth, that is.

Terrifying visuals aside, there are a few nuanced reasons—firmly grounded in architectural history—why Victorians turned into the pop culture stuff of nightmares.

Victorians were inherently ‘dark’

So let’s start at the beginning: The Victorian era is typically defined as beginning in 1837—when Queen Victoria of England ascended the throne. But the period’s influence on American architecture focuses on the years between 1860 and 1900.

Homes built during this period typically drew their influences from Gothic Revival, Romanesque, Queen Anne, and Second Empire styles. For example: false fronts, false chimneys, tall towers, dormer windows, and gables. Victorians were typically situated on hilltops, where their usually wealthy owners could, quite literally, look down on their neighbors.

Victorians often feature tall turrets or rectangular towers topped by ornate cast-iron railings and prominent weather vanes—features that rusted and sometimes slipped out of place over time.

“These are the house styles Hollywood depicts high on a hilltop with bright lightning strikes in the background, causing the descriptor building to be outlined in dark silhouette against the sudden light,” says archaeologist and architectural historian Ronald V. May of Legacy 106 Historic Preservation in California.

In other words: creepy.

The era was also notable for its overwrought furniture, dark interiors, and heavy draperies, says Charles Robertson, a board member of the Victorian Society of America (who himself lives in a meticulously maintained Victorian home in Washington, DC’s Dupont Circle neighborhood).

During their heyday, “these houses were indeed dark and cluttered,” he says. “They had bric-a-brac everywhere, and they were just elaborate and ornate.”

Move toward modern architecture left Victorians empty and decrepit

Interest in the genre waned dramatically over the years, leaving more and more Victorian homes empty and decrepit. Some historians claim the downfall of the Victorian aesthetic really began with the 1893 World’s Fair in Chicago—the site of which became known as “White City” for its clean, mostly white neoclassical buildings.

It was the beginning of the end for Victorian homes’ heyday, according to Robertson. The style fell out of favor in the 1930s as tastes began to skew toward modern design.

As time wore on, “the elderly owners passed away, and their children let the houses fall into serious disrepair with little or no paint, causing shingles to slough off, ornamental metal roof edges to rust and break down, pieces of siding drop off, and windows break and not be replaced,” May says.

A Victorian revival?

But here’s the thing: What goes around indeed comes around. Look no further than San Francisco, which has enjoyed a historic home preservation blitz over the past several decades—and where a Painted Lady will now run you at least $3 million.

And if the headache of a large-scale renovation isn’t your bag, there are a handful of builders committed to building “new Victorian” homes—although the intricacies involved in this kind of construction make it more expensive than your usual run-of-the-mill new build.

But in the end, Americans love a good horror story—and classic Victorians provide the perfect backdrop.

“The aging population of historic homes makes everyone familiar with that one neighborhood house that has deteriorated, and everyone talks about the crazy old man that used to live there,” Moore says.

Throw in peeling wallpaper and paint, decades-old dusty draperies, and more gables and turrets than could possibly be prudent, and you’ve got the stuff of nightmares (and more than a few urban legends).

———

Watch: We Dare to Peek Inside the Winchester Mystery House

Fertility phenom Kate Gosselin famously shared her family life with the world on “Kate Plus 8.” Now that her kids are growing up, she’s selling the family home she bought with her former husband, Jon, in 2008.

It served as the backdrop for the long-running reality TV show, and folks wanted a peek inside. Those curiosity-driven clicks made the 24-acre spread this week’s most popular home on realtor.com®.

On the market for $1.3 million, the 7,591-square-foot home is designed for a large family. It boasts a large family room, a man cave, and a separate living space over the garage.

You also clicked on a noteworthy celebrity mansion: the marvelous modern house of Washington Nationals pitcher Max Scherzer, which sits on the banks of the Potomac.

Other homes attracting attention this week include a Michigan home painted inside and out in gunmetal gray, a custom log cabin headed for auction, and a spectacular winery in Washington.

While we debate the sanity of spending $50 on a personalized greeting from Jon Gosselin, we think you should scroll down for a look at this week’s 10 most popular properties.

Price: $400,000 Why it’s here: Built in 1870, the Max Freuerbacher mansion is also known as the Lion House thanks to the two limestone lion statues flanking the front entrance.

According to the listing, the home’s original owner was the founder of Green Tree Brewery. The one-of-a-kind mansion is being sold as is. It has three sets of entry doors, pine inner doors with art glass, double drawing rooms, marble fireplaces, and a frescoed 14-foot ceiling. And for oenophiles, this place is a treat: The basement has two vaulted wine cellars.

Price: $679,900 Why it’s here: This 20-acre property comes with 1,100 feet of Kennebec River frontage. The four-bedroom farmhouse was built in 1820 and offers 3,136 square feet of living space.

Highlights of the remodeled home include a gorgeous kitchen, spacious mudroom, wood floors, and built-ins. You can soak in the views from the home’s large front porch, take a dip in the heated in-ground pool, or make use of the many outbuildings and barn.

Price: $224,000 Why it’s here: Also in Maine, this affordably priced property comes with a six-bedroom home built in 1780. Although it looks like it could use some TLC, the property offers plenty of potential for a bargain shopper willing to take on a project.

Price: $325,000 Why it’s here: We love a log cabin, and this one is absolutely adorable.

Rustic meets modern in this cute three-bedroom cabin near the lake. Built in 1953 and updated throughout, the charming home sits in a clearing of aspen trees bordering a U.S. Forest Service parcel. Close to loads of outdoor activities, the property even has a seasonal creek for an added touch of magic.

Price: $439,800 Why it’s here: One-of-a-kind and updated throughout, this lovely three-bedroom, German-style farmhouse was built in 1936. The leafy acre lot also features a barn with a second-story bonus room and an outdoor patio with a large fire pit.

Price: $3,750,000 Why it’s here: For fans of Carménère grapes, this Washington winery looks absolutely delicious.

Known as the Naoi Cailini Oga Estate, the 6-acre property includes a luxe mansion with an indoor pool. There’s also an art studio, workout room with ballet barre, as well as several terraces and balconies. The home is surrounded by lush landscaping and comes with a tasting room for indulging in a few of your favorite vintages.

Price: $201,000 Why it’s here: This five-bedroom log home is headed to an online auction with a starting bid of $1,000. The current owner has moved to be closer to family and wants to part with this property in a hurry. According to the listing, the custom home has an assessed value of $416,000. Get your bid in now!

Price: $15,000,000 Why it’s here: Sleek and chic, this five-bedroom mansion along the Potomac is being sold by Nationals ace Max Scherzer. The future Hall of Famer gave the home a full makeover, including multitiered decks, an infinity pool, and a rooftop terrace to take in the river views.

Price: $69,900 Why it’s here: The owner of this house made a commitment to the color gray, and you simply have to respect it. It’s not just the exterior. All interior walls, ceilings, and floors have the same silvery hue.

Besides the occasional pop of white furniture, all carpets, drapes, and doors are monochromatic. The three-bedroom house has a large front porch, an updated bathroom with high-tech shower, and a full basement—which looks to be the only space that evaded the gray paintbrush. The home isn’t expensive, but a buyer will need to shell out money for new paint unless he happens to be gaga for gray.

Price: $1,299,900 Why it’s here: Supersized and customized to accommodate her large brood, the home of reality TV star Kate Gosselin is up for sale.

She’s ready to part with the 24-acre property, which includes the six-bedroom home where she’s been raising her kids for over a decade. Ideal for a large family, the home boasts a lower-level game room, two washers and dryers, and a separate living area over the detached three-car garage. For downtime, there’s a pool plus a three-stall horse barn with 10-acre fenced paddock.

Households that own their home typically spent 17.5% of household income on their monthly housing payments in September, down from 19.6% two years earlier.

Record-low mortgage rates are driving these affordability gains, but saving for a down payment remains a challenge for first-time buyers especially.

Home values have grown at about twice the rate as incomes over the past six years. The typical U.S. home is now worth 3.08 times the median homeowner household income, an all-time high in Zillow's data.

Ultra-low mortgage interest rates are helping to keep monthly payments remarkably affordable for would-be home buyers and homeowners alike. But these same low rates are also helping to mask an alarming rise in price-income ratios, keeping homes affordable on paper while doing nothing in practice to help buyers put themselves in position to buy in the first place.

A would-be home buyer earning the median income for buyers ($83,674) and looking to purchase the typical U.S. home in September — assuming a 20% down payment and 30-year, fixed-rate mortgage at prevailing rates — could expect to spend 17.5% of their monthly income on a mortgage payment, taxes and insurance. The same buyer could have expected to spend 18.2% and 19.6% of their income each month on their core housing payments in September 2019 and September 2018, respectively, according to a Zillow analysis of housing costs andprojected income growthover the past two years.

At current rates, mortgage payments on the typical local home are most affordable in Louisville (12.3% of income), Birmingham (12.5%) and Indianapolis (12.7%). They are the most burdensome in San Francisco (34.4%), San Jose (31.6%) and Los Angeles (29.9%).

Rates at Historic Lows

Falling interest rates are the primary driver of improving mortgage affordability in recent years. Currently (as of Oct. 26, 2020), the average rate on a 30-year, fixed-rate mortgage is 2.8%,according to Freddie Mac, almost 100 full basis points less than the 3.75% average rate quoted at the same time a year ago. The other side of the affordability equation — incomes — are also improving. In September 2020, typical U.S. homeowner incomes grew an estimated 2.7% relative to the prior year, from $81,502 to $83,674.

At the same time, the typical total monthly payment fell 1.4% year-over-year — but almost entirely on the back of lower interest rates. Because even as incomes grew, home prices themselves were growing even faster. While homeowner income was up 2.7% year-over-year in September, the typical U.S. home increased in value by 5.8% over the same period. Since September 2014, home values have grown 38.3%, roughly double the pace of homeowner income growth (18.8%) over the same period.

It was not so long ago that a mortgage rate of 5% on a 30-year, fixed-rate loan was considered a steal — in weekly data from Freddie Mac going back to 1971 (which includes periods, like the early 1980s, in which rates in the teens were commonplace), the average rate on a 30-year, fixed-rate mortgage is 7.92%. Historically low mortgage interest rates have been a fixture of the market for the past several years, hovering in the mid-4% range for much of 2018 and 2019. But rates below 3% were virtually unheard of prior to the past few months — but have been below 3% on average in every week since July 30.

Low rates are undoubtedly good news for would-be home buyers and particularly current homeowners, who have enjoyed big equity gains in recent years and can now refinance their mortgage to lower their monthly payments and savethousands of dollarsover the course of their loan. But these low rates serve to mask an ugly truth: Without them, rapidly rising home prices and more-modest wage growth would threaten to put homeownership out of reach.

The Price of Rising Prices

For the better part of the last 6 years, total monthly payments grew faster than incomes. In September 2020, the U.S. home price-to-income ratio was 3.1 — meaning the typical home was worth 3.1 times as much as the typical homeowner earned in a year — the highest multiple since at least 2014. In January 2014, the typical home was worth about 2.6 times the median homeowner income. Since 2014, the long-run average price-income ratio has been 2.8.

When income growth fails to keep pace with home value growth, it makes saving for a suitable down payment of even 5% or 10% — to say nothing of the "standard" 20% down payment assumed in this analysis — that much more difficult. Putting 20% down enables buyers to avoid paying additional private mortgage insurance premiums, but it's not required, and just 39% of buyers with a mortgage put down at least 20%, according to the 2020 Zillow Consumer Housing Trends Report. And it's no wonder: Saving for a down payment is a massive financial barrier for those looking to move into homeownership. More than a quarter of first-time buyers report difficulties saving for a down payment, and 40% of all buyers rely on a gift or loan from family or friends for at least part of their down payment, according to the same 2020 Zillow survey.

At the start of 2014, a 20% down payment on the typical U.S. home would have been about $36,600, or 6.4 months of income for the median homeowner household. As of September, that down payment had grown to about $52,000 (on a home worth almost $260,000) — or about 7.5 months of income for the typical homeowner household. Zillow expects the typical U.S. home to grow in value by 7% over the next 12 months, to slightly more than $278,000 by September 2021. By then, the amount needed to cover a 20% down payment on that typical home will have risen to $55,600 — up about $3600 from today, or a full $300 in additional savings needed per month. Faced with this unrelenting rise in home prices, it's no wonder that buyers currently in the market may be desperate to quickly settle on a home and lock in a low rate — savings that are adequate today may not be tomorrow.

Among the 50 largest U.S. metros, down payments are most in reach for potential buyers in Cleveland, where a 20% down payment on the typical home is equal to 5.1 months of income for the median homeowner household. Milwaukee, Pittsburgh and Memphis have the next most affordable homes by this measure, each at 5.2 months of income. Homes are most difficult to save for in high-priced California metros, led by San Francisco (17.1 months of income), San Jose (16.1), Los Angeles (14.9) and San Diego (13.2).

Mortgage interest rates are expected to stay low for the foreseeable future, but if and when they begin to rise again — even modestly — affordability and mobility may both deteriorate. There is the simple math that shows how even small rises in rates can impact monthly payments and ultimately limit buyers' budgets in the face of high prices. But there's also thelong-discussed but yet-to-materialize specter of so-called "mortgage rate lock-in,"in which existing homeowners that already have a very low mortgage interest rate may be unwilling or unable to move as rates rise.

Renters Hit Disproportionately Hard

Renters, of course, cannot take advantage of low mortgage interest rates and finance their purchase over decades. They must spend more of their monthly income on rent than their homeowning peers will spend on a mortgage — and more money spent on rent is less money saved for a down payment. Even so, the share of typical renter income devoted to the typical U.S. rent was 29.9% in September, the lowest share since 2014 and below the 30% threshold at which a household is considered "rent burdened." This improvement can be laid almost exclusively on assumed growth in renter incomes since 2018, which would certainly be welcome news in almost any month…

…Except in our current moment. We have not yet modeled the full impact of COVID-19 on renter incomes, but research shows that renters have been hitdisproportionately hardby unemployment and the lack of comprehensive and lasting fiscal assistance. Given this, it is likely that the current share of typical renters' income devoted to paying their rent is much higher in the current environment. We are currently working to incorporate these effects into a supplemental model of renter incomes, and look forward to publishing the results soon.

Westfield, NJ, a town of grand, restored Victorians and stately mansions perched on tree-lined streets, is the kind of place many folks aspire to one day call home. The downtown features mom and pop shops and bakeries alongside a Williams-Sonoma and Baby Gap stores. Even before COVID-19, busy roads were often closed off so residents could listen to live music while dining outdoors, participate in children’s arts and crafts projects, or take open-air yoga classes. Many who grow up in the affluent suburb, about an hour west of Manhattan, return after college to raise their families there.

The pandemic has boosted its upscale appeal, making it a popular destination for folks escaping nearby cities in search of more space. That’s led to a nearly 13.5% annual surge in home prices, to a median list price of $884,050 in September, according to realtor.com® data.

But most newcomers aren’t immediately aware that Westfield has a macabre side—and a deeply dark history.

A string of high-profile murders has taken place within Westfield’s 6.7 square miles, leaving homes across the city with gruesome footnotes in their property history. They include the sprawling home on a hill where accountant John List murdered his wife, three children, and mother, and then vanished for 18 years—perhaps the most famous “family annihilation” in U.S. history. Then there’s “The Watcher” house, whose new owners were subjected to a campaign of terror by a mysterious letter writer, inspiring a 2016 Lifetime movie and an upcoming Netflix flick.

It seems in nearly every generation, Westfield makes the national news for a sinister crime.

The town’s imposing, Victorian-rich architecture may have even inspired Charles Adams to create “The Addams Family” cartoons, with its spooky mansion and spookier inhabitants.

“It does seem like a lot for a town of 30,000,” says Lauren Barr, editor and publisher of the Westfield Leader, the local newspaper. She grew up here and graduated from Westfield High School in 1998.

But “I don’t think that it has affected the town’s reputation,” she adds.

The thing is, few would expect such heinous acts to occur in such a wealthy, picture-perfect community, says Arthur Lurigio, a criminology and psychology professor at Loyola University Chicago.

The crimes “stand out because of the place,” says Lurigio. “This isn’t supposed to happen. … It’s not a place where you expect violence to occur.”

The infamous ‘Watcher’ house wrenched Westfield back into the spotlight

The previous owners of “The Watcher” house received chilling letters from an anonymous writer.

Clare Trapasso

Westfield’s most recent touch of national infamy was the twisted tale of “The Watcher” house.

A couple purchased the six-bedroom, turn-of-the-century Dutch Colonial for more than $1.35 million in 2014, then spent an additional $100,000 on renovations. But Derek and Maria Broaddus and their three children never moved in.

The family’s nightmare began when they received the first in a series of chilling letters. The anonymous writer claimed to be charged with “watching” the house, just as the writer’s father and grandfather did before. The “watcher” seemed to be particularly interested in the couple’s children, referred to in the letters both as the “young blood” and by their individual names.

“Will the young blood play in the basement? Or are they too afraid to go down there alone. I would [be] very afraid if I were them. It is far away from the rest of the house. If you were upstairs you would never hear them scream,” one of the letters said.

Perhaps most frightening, the writer appeared to be omnipresent and yet nowhere, perhaps hiding in plain sight.

“All of the windows and doors in 657 Boulevard allow me to watch you and track you as you move through the house,” the watcher wrote.

Then later in the same letter: “I pass by many times a day. 657 Boulevard is my job, my life, my obsession. And now you are too Braddus family.”

Another note asked: “Do you know what lies within the walls of 657 Boulevard?”

“It was quite the story at the time,” says newspaper editor Barr. “Everyone put their sleuthing hats on in town. … It was all anyone talked about for a while.”

The Broaddus family found themselves stuck with an expensive home they didn’t feel safe visiting, much less living in.

They sued the former owners of the home, who had received one letter from the watcher a few days before they moved out, but never told the new owners. The case was dismissed. Next, the couple proposed razing the place and selling the lot for two new homes to be built in its place. The idea was soundly rejected by the town’s planning board. The couple resorted to renting out the home.

Last year, the Broadduses finally sold the place for about $959,000, a substantial loss.

So who was the watcher? At various times, different neighbors came under suspicion. Some residents, unhappy with the unwelcome attention placed on their town, even surmised that the Broadduses sent the notes to themselves (which the couple staunchly deny). The mystery has never been solved.

One longtime Westfield resident walking her two dogs by the home on Tuesday morning said interest in the episode had died down.

“It was really intriguing at the time and very scary,” says Rebecca Jezierski, 70, who lives a few blocks away. But “all of a sudden [the letters] just stopped when these new people moved in.”

John List murders his family—and then disappears

Accountant John List murdered his family and then eluded capture for 18 years.

Courtesy of The Westfield Leader

“The Watcher” house would be a creepy enough local legend for one town. But one day a half-century ago, Westfield accountant John List shot his mother, wife, and three children to death in their 19-room Colonial, known as Breeze Knoll.

List struggled to hold down a job, and hadn’t told his family he’d lost his latest one and was broke. Moreover, he felt his family was turning away from the church (he was a devout Lutheran) and toward temptation.

On Nov. 9, 1971, List shot each one, then wrote a letter to his pastor explaining he was saving them from the embarrassment of losing their home and from endangering their place in heaven.

Then List disappeared.

The original List home burned down in a mysterious fire after the List murders.

Courtesy of The Westfield Leader

He created a new identity, remarried, and moved to Colorado. It wasn’t until an “America’s Most Wanted” episode on the murders aired that he was finally caught—18 years after the murders. List died in prison in 2008 at the age of 82.

“People still remember it. When I was growing up, John List was the ghost story,” says Barr. She used to live two streets over from the List property.

During List’s 1990 trial, townspeople would line up outside of the courthouse as early as 6 a.m. to get a seat in the galley.

A wanted poster seeking the capture of John List, who murdered his family.

Courtesy of The Westfield Leader

The home where the List family perished burned down nine months after the murders, in 1972. Locals traded theories about the suspicious fire. Some believed List returned to torch the mansion, says Barr. Others dismissed it as the handiwork of kids—or Satan worshippers. The property was auctioned off late that year to local newspaper publisher Kurt Bauer for a winning bid of $36,100.

The property itself then became the link to another high-profile killing in town, 25 years after the List murders.

JeffreyBauer, 48, Kurt Bauer’s brother, was shot by his estranged wife, Meta Bauer, in 1996 at the Westfield Leader, the local newspaper where he was the publisher. She then killed herself.

“It was just another very strange thing to happen in what’s usually a quiet, sleepy town,” says Barr, who did not work at the newspaper at the time.

A new home stands in the spot where List’s home burned down in Westfield, NJ.

Clare Trapasso

Several more murders were committed in Westfield

The List murders weren’t the first case of a local parent killing a child in Westfield. In 1959, 17-year-old high school basketball star Raymond Bailey III was stabbed to death with a kitchen knife by his mother in their home. She then stabbed herself 25 times, but survived.

There were other murders in the tony town as well.

In 1974, Dr. John J. Graff, 56, was killed in a mugging after leaving the local train station. Authorities believed he was on his way home, just three blocks away. No one was ever caught.

Two years later, Lena Triano, 57, was hogtied with electrical cords cut out of her appliances, raped, strangled with a tie from her bedroom blinds, and stabbed multiple times in her Westfield home. It took 36 years for authorities to track down the murderer, Carlton Franklin.

More recently, college student Sohayla Massachi, 23, was abducted from Seton Hall University by her ex-boyfriend in 2000. He brought her to his Westfield apartment and shot her to death.

‘The Addams Family’ creator found creepy inspiration growing up here

Cartoonist Charles Addams grew up in this Westfield home.

Clare Trapasso

Maybe it’s fitting that Westfield’s most famous former resident was cartoonist Charles Addams, known for his dark characters and pitch-black sense of humor, as seen in “The Addams Family.”

His beloved characters grace the windows of the town’s downtown shops at this time of year, and the town’s AddamsFest puts on a series of family-friendly, Halloween events (this year with social distancing measures in place).

Addams was born in 1912 and grew up in a modest home with canvas awnings over the windows near the heart of town. On his walks to school, he passed by spooky, abandoned Victorians said to have inspired the “Addams Family” mansion.

“When Charles grew up, a lot of those houses were empty and rotting and falling apart,” says Kevin Miserocchi, executive director of the Tee and Charles Addams Foundation. (Marilyn “Tee” Addams was the cartoonist’s wife.) “That [Victorian] architecture intrigued him.”

The first “Addams Family” cartoon ran in the New Yorker in the late 1930s, after the cartoonist left Westfield for Manhattan.

Addams biographer Linda H. Davis disputed the rumors the architecture in the “lovely town” of Westfield inspired the “Addams Family” mansion.

“It’s a persistent myth,” says Davis, author of “Charles Addams: A Cartoonist’s Life.” She claims he borrowed architectural details from different buildings he saw and used them in new variations of the mansion. “The house is never drawn the same way twice.”

Cartoonist Charles Addams may have been inspired to create “The Addams Family” mansion by the local architecture.

Clare Trapasso

Why Westfield’s housing market hasn’t been hurt by these tragedies

The pandemic has spurred buyers from nearby cities, like New York City, Hoboken, and Jersey City, to descend on Westfield. Many are searching for big homes with even bigger backyards to ride out the COVID-19 crisis and any new stay-at-home directives. Westfield’s more unsavory history doesn’t often come up in conversations with these soon-to-be residents.

“People coming to Westfield don’t know anything about ‘The Watcher’ house and don’t care about it,” says local real estate agent Scott Gleason, of Re/Max Select. “I haven’t heard about it in town conversations or real estate conversations in a year. … [And] John List is ancient lore.

“They’re not related to our real estate reality,” he says.

Westfield, NJ, is the site of some unsettling events.

Clare Trapasso

“If you have a spate of burglaries or there are armed robberies on the street in the central business district, you might see people wanting to move out,” says criminologist Lurigio.

But that is not the case here.

Westfield received an A-plus crime rating from AreaVibes, which evaluates the best places to live. It had 96% less violent crime and 71% less crime overall than the national average, according to the site.

“Lots and lots of people want to live here,” says Gleason.

New home sales slipped slightly in September, but remain incredibly strong overall. The stock market suffered its worst day in a month as coronavirus case counts surged to new highs. And protections for renters are being challenged in court.

New home sales fall short of expectations, but remain elevated

September new home sales fell 3.5% from August, but were up 32.1% from a year ago, to 959,000 (SAAR) according to the U.S. Census Bureau.

There were 3.6 months' of supply of new homes available for sale in September.

Financial markets reels as coronavirus cases surge

New COVID-19 cases are rising in the U.S. at their fastest pace yet – more than 83,000 new cases were reported on Friday.

The development, plus stalled negotiations around fiscal relief, caused the S&P 500 to suffer its worst loss in a month.

Eviction moratoriums are being met with some pushback

A national eviction moratorium announced in September is being challenged in court in a case supported by the National Apartment Association.

A win for the plaintiff could force evictions to rise sharply.

So what?

September new home sales fell somewhat short of expectations and represent a small decline from prior months - but at just shy of 1 million sales for the month (at a seasonally adjusted annual rate), it’s clear the new home market overall remains very strong. Year-to-date, new home sales are up 16.8% from the same nine-month period in 2019. A favorable mortgage interest rate environment, an enduring desire for brand-new homes and a longstanding shortage of existing homes available for sale continue to pay dividends for home builders. And builders are clearly taking notice – their expectations for sales volume over the next six months are the highest they've ever been.The question now is whether these goods times can continue and for how long. A lasting inventory drought matters less for new home sales than for the re-sale market – roughly two-thirds (67.6%) of new homes purchased in September weren't even built yet. But broader economic and social factors including persistently high unemployment and the spread of the coronavirus represent considerable potential constraints for new home sales.For now, though, these issues don't seem to be much of a threat to what continues to be a very solid run for new home sales.

Data compiled by Johns Hopkins University showed that the number of new daily COVID cases in the U.S. has risen by an average of just under 69,000 over the last week, a new record and up about 22% from a week ago. Experts acknowledged that testing volume has increased, which would drive up positive numbers on its own, but suggested that this alone can't explain the strong uptick.Daily new case counts are now at record-high numbers in more than 20 states, most of which are concentrated in the Midwest. This surge coincided with talks surrounding the next round of fiscal stimulus coming to a halt — and financial markets clearly took notice. On Monday, the S&P 500 recorded its biggest one-day drop in more than a month. Equity indices overseas fell similarly, and some fears emerged that Europe may be headed towards a double dip recession.As the pandemic nears the end of its seventh month, the developments are a stark reminder of the strong hold the coronavirus still has over the economy.

The federal government issued a national moratorium on rental evictions last month, allowing renters nationwide to file for up to four months of rent payment suspension if their economic well-being had been damaged as a result of the pandemic.But reports suggest that many evictions are still taking place and the eviction ban has been met with a slew of legal challenges in the weeks since. A recent hearing of a case against the moratorium has been supported by the National Apartment Association, a group that represents 85,000 landlords responsible for 10 million rental homes. A ruling in the favor of the plaintiffs could offer landlords more flexibility to work around similar moratoriums and potentially prompt a surge in evictions in coming weeks.As of October 12, more than 8 million households were not caught up on rent payments, according to the Census.

Click here to read past editions of Zillow’s Market Pulse updates.

Past attempts at quantifying housing affordability suffered problems of both timeliness and specificity: Current housing costs were divided by literally years-old income data; and broad, median household income data was aggregated across two groups — homeowners and renters — with very different income profiles.

Traditional housing affordability measures based on income data from the American Community Survey (ACS) do not provide clear insight into the current state of affordability because comprehensive ACS data are published at a lag: Data for 2019, for example, is only just now being published, in late 2020. And while current income data is available through the Bureau of Labor Statistics (BLS), it is also aggregated data and does not discriminate between renter household income and homeowner household income. While BLS data do provide significant detail on industry specific incomes, industry-specific income data presents its own set of challenges for estimating renter and homeowner incomes separately, since the mix of renters and homeowners in each industry may vary significantly across different metropolitan areas.

Zillow's new statistical models aim to address these challenges by predicting renter and homeowner incomes forward from their last published observation, and applying them to current housing costs. We publish this housing affordability data — measured as the share of a typical renters' income spent on typical area rent, and the typical homeowners' income spent on a mortgage for the typical local home — for 100 metropolitan areas and the United States as a whole.

Our models include ACS data, the Zillow Observed Rent Index (ZORI), the Zillow Home Value Index (ZHVI) and earnings data from the Bureau of Labor Statistics. The final output (in this example, for renters) is based on this simple equation (with the numerator for homeowners substituted with observed Zillow Home Value Index for a given month):

The estimated monthly rent in the numerator is a weighted average of the reported contract rent in ACS microdata andZillow's Observed Rent Index (ZORI). The weights are the percentage of renters who reported moving in the last 12 months (reported via the MIGRATEPCT variable in ACS microdata). Our estimated monthly rent is:

Our goal is to compute the most timely measure of rent paid by the typical renter in each metro, and we include both ZORI and ACS data to leverage the strengths of different sources of information.

We predict ACS renter incomes in months where it is not directly observed using a Bayesian statistical model — both in months between the annual releases from 2014 to 2018 and months since the last release in 2018. Our Bayesian model provides the statistical machinery to incorporate multiple sources of information and update predictions as new data is released. Our model depends on observed ACS renter income and observed BLS income data. From a statistical standpoint, our main objective is to compute the posterior predictive distribution:

Where:

is monthly renter income from January of 2014 to September of 2020.

is the subsequence of renter incomes corresponding to ACS observations reported annually for 2014 – 2018

is the observed BLS monthly earnings data.

We model, the BLS reported income, as the sum of the renter income latent variable, and latent factor, the metro-specific deviation in general earnings from renter earnings. Latent factor follows a dynamic linear model with a second-order polynomial structure:

The model for latent renter income has three components:

intercept, the expected renter income in December 2013

global trend , the expected monthly increase in renter incomes

a flexible function that models nonlinear deviations in renter income from the linear regression +

Function follows a Gaussian Process prior distribution and has a very important property for this application: the uncertainty intervals in predicted renter incomes widen as the time elapsed from the last observed renter income increases. Overall, this latent renter income model is:

Model parameters are estimated with a custom Markov chain Monte Carlo algorithm, and we compute full predictive probability distributions of renter incomes and rent affordability rather than single point estimates. Given that these estimates are statistical in nature, we believe quantifying the uncertainty in our affordability calculations is an important part of the analysis, and predictive intervals provide additional context to the state of housing affordability in the United States.

We follow a similar process to calculate homeowners' incomes based on ACS and BLS data. Monthly costs for homeowners assume the buyer is purchasing a home valued at the typical level for a given metro (as measured by theZillow Home Value Index), is putting down 20%, and is assuming a 30-year, fixed-rate mortgage at prevailing rates (as measured by Freddie Mac). We also make adjustments for local taxes and homeowner insurance costs.

The S&P CoreLogic Case-Shiller U.S. National Home Price Index® rose 5.7% year-over-year in August (non-seasonally adjusted), up from 4.8% in July.

Annual growth was up from July in the smaller 20-city index (to 5.2%, from 4.1%) and 10-city index (to 4.7% from 3.5%).

Phoenix (+9.9%), Seattle (+8.5%), and San Diego (+7.6%) reported the highest year-over-year gains among markets in the 20-city index.

The remarkable surge in home prices continued into August as prices showed no signs of cooling down heading into the fall.

The national Case-Shiller Home Price Index rose 5.7% year-over-year in August. The smaller 10- and 20-city composite indices grew more slowly, at 4.7% and 5.2% year-over-year, respectively. The annual rate of growth was faster in August than in July in all three main indices. On a monthly (seasonally adjusted) basis, the 10- and 20-city indices were each up 0.5%, and the national index was up 1% from June.

Zillow Forecast, Released 9/30/20

Actual Case-Shiller Indices,

Released 10/27/20

Historical Median Absolute Error*

10-City Composite,

Month-Over-Month (SA)

0.4%

1.1%

0.2%

10-City Composite,

Year-Over-Year (NSA)

3.9%

4.7%

0.2%

20-City Composite,

Month-Over-Month (SA)

0.4%

1.1%

0.2%

20-City Composite,

Year-Over-Year (NSA)

4.5%

5.2%

0.1%

U.S. National

Month-Over-Month (SA)

0.4%

1.1%

0.1%

U.S. National

Year-Over-Year (NSA)

5.3%

5.7%

0.1%

*Calculation of Median Absolute Errors are based on Zillow’s forecasts dating to 2011. The national Case-Shiller forecasts began in 2014.

By some measures, home prices are rising at a faster pace than they ever have – an incredible feat considering the market is rising from an already elevated level. The supply of for-sale homes, already extremely tight, has only become more constrained in recent months, and historically low mortgage rates continue to encourage many buyers to enter the market. This heightened competition for the few homes on the market has placed consistent, firm pressure on home prices for months now, and there are few signs that this will relent any time soon. While the path of the overall economy is likely to be most directly dictated by coronavirus-related and political developments in the coming months, recent trends suggest that the housing market – which has basically withstood every pandemic-related challenge to this point – will continue its strong momentum in the months to come.

Annual growth in September as reported by Case-Shiller is expected to accelerate in all three main indices. S&P Dow Jones Indices is expected to release data for the September S&P CoreLogic Case-Shiller Indices on Tuesday, November 24.

Index

Actual August

Case-Shiller Change

Zillow’s Forecast for the Case-Shiller Sept. Indices

10-City Composite,

Month-Over-Month (SA)

1.1%

0.7%

10-City Composite,

Year-Over-Year (NSA)

4.7%

5.7%

20-City Composite,

Month-Over-Month (SA)

1.1%

0.7%

20-City Composite,

Year-Over-Year (NSA)

5.2%

6.2%

U.S. National

Month-Over-Month (SA)

1.1%

0.8%

U.S. National

Year-Over-Year (NSA)

5.7%

6.6%

Note: Case-Shiller and Case-Shiller Index are registered trademarks of CoreLogic Solutions, LLC. The statements herein are not endorsed by or provided in association or connection with CoreLogic, LLC.

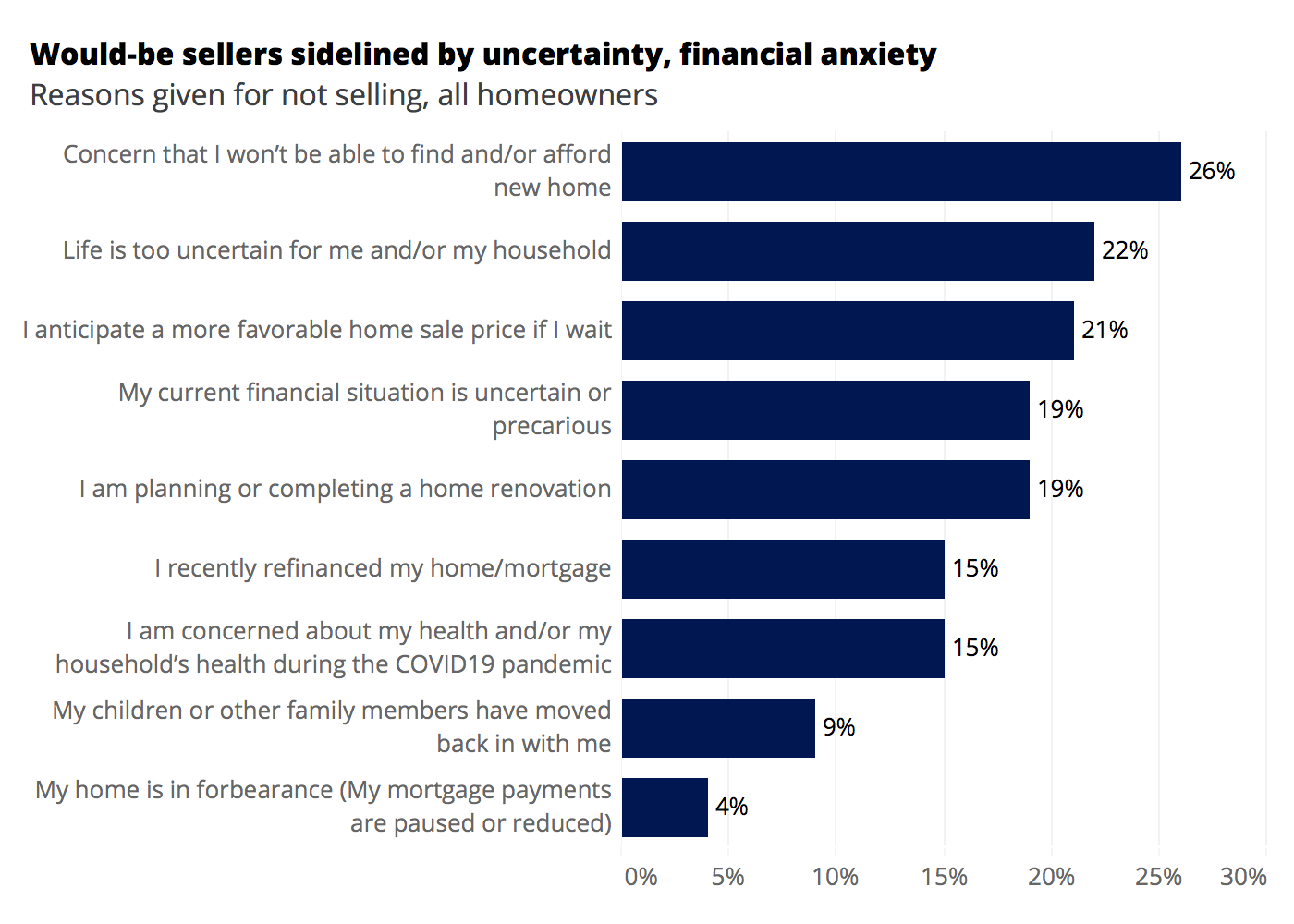

About a third of homeowners who are considering selling in the next three years cite life being too uncertain right now (34%) and financial uncertainty (31%) as reasons they aren't selling.

Nearly 40% of these potential sellers say they anticipate a higher sale price if they wait.

Despite a market tilted decidedly in their favor — with demand sky-high and inventory at rock bottom — potential home sellers are largely staying on the sidelines, citing a variety of personal financial, lifestyle and/or health concerns as major reasons.

Only 1% of homeowners recently surveyed by Zillow said their homes were currently listed for sale. Among the 99% whose homes are not on the market, more than a quarter (26%) said they were concerned they would not be able to find or afford a new home once their current home was sold, the most commonly cited reason for not selling. General life uncertainty (22%) was the second-most common reason, followed by anticipation of a more favorable sale price if they wait (21%).

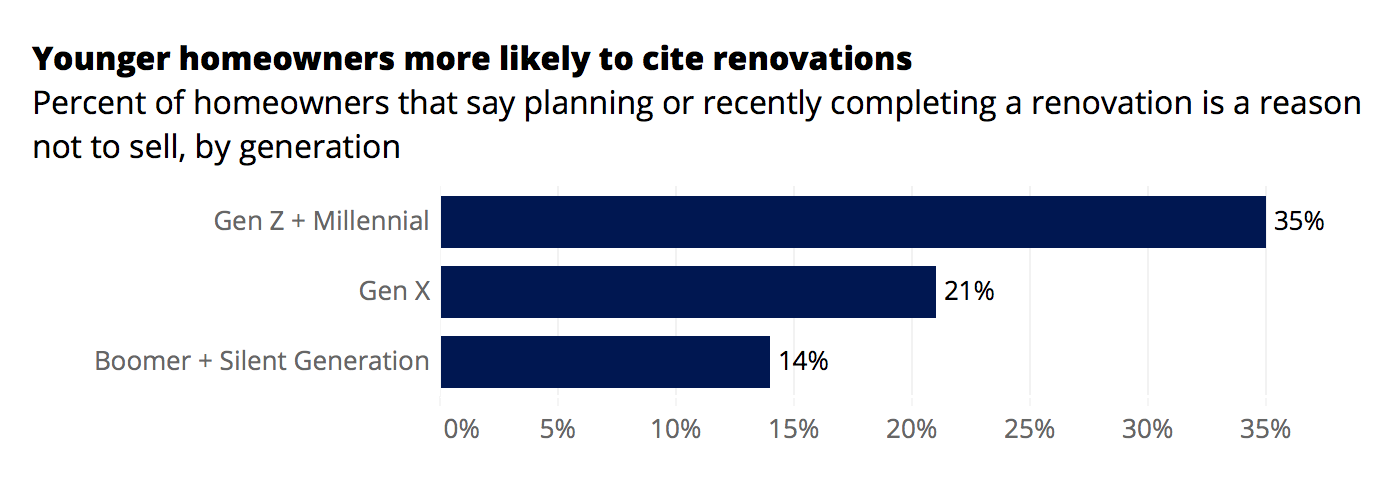

Reasons for not selling vary by age group: More than a third (35%) of Gen Z and Millennial homeowners said their plans for or completion of a home renovation was a main reason to stay put, compared to just 21% and 14% of Gen X and older homeowners, respectively. Younger homeowners were also more likely to cite concern about COVID-19 (20% of Gen Z and Millennial and 18% of Gen X) as a reason for not selling than Boomer and Silent Generation homeowners (11%).

Some homeowners realistically may simply enjoy their current home and have no need or desire to sell and move any time soon. But among homeowners considering selling within the next 3 years, 39% said they anticipate a better price if they wait. Among those who are not currently considering selling, but may be open to it after 3 years, 39% cite concern that they won't be able to find or afford a new home.

Concern over finding or affording a new home among those more likely to sell in the near-term was a bit more muted, but still very real: Almost a third (31%) of homeowners considering selling in the next three years say their plans are paused because they are concerned about finding or affording a new home. The findings are a clear example that selling a home can sometimes cut both ways: According to the 2020 Zillow Consumer Housing Trends Report, almost two-thirds (63%) of sellers are also buyers. But while these dual-track homeowners may be able to sell their home for top dollar, they will also turn around and enter an extremely competitive buyers' market wherehomes are going under contractin 12 days.

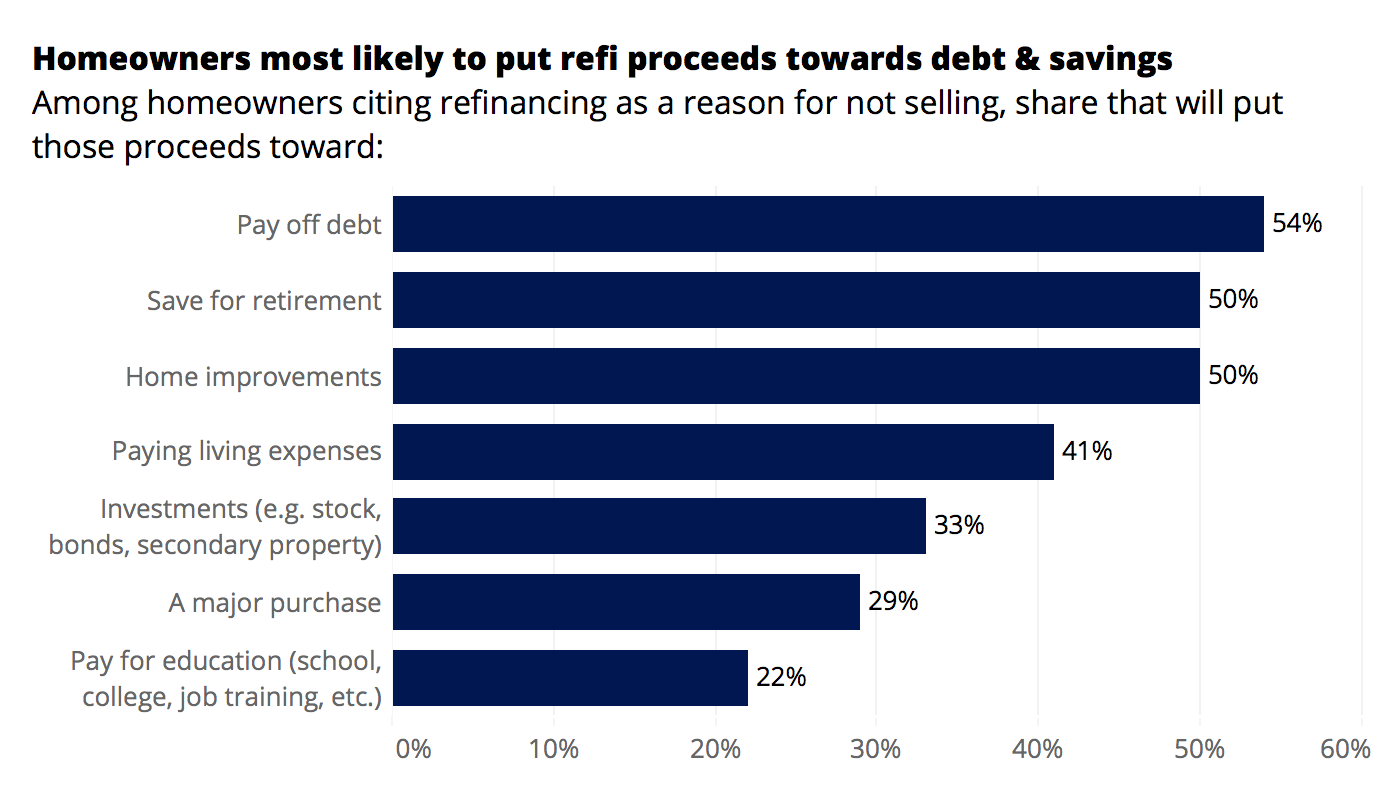

Given the historically low mortgage interest rates that many home buyers and homeowners can enjoy these days, it may come as little surprise that 15% of homeowners report a recent refinance as a reason for staying put — but their planned uses for their newfound financial flexibility are very different. Among respondents that cited a recent refi as a reason to stay put, a majority (54%) said they would use their savings to pay off debt. Exactly half said they would use the savings for home improvements or saving for retirement.

General life uncertainty, especially given the ongoing pandemic, high unemployment and volatile economic conditions,is a main factor keeping more than a third (34%) of those considering selling in the next three years out of the market. Among these homeowners hesitant to put their home on the market now, a quarter said they weren't selling because they were concerned about their household's health and safety during the pandemic.

Financial anxiety, again likely attributable at least in part to the pandemic, is another big factor keeping those that might sell sooner on the sidelines: 31% of homeowners considering selling in the next three years said a currently uncertain or precarious financial situation is a reason to stay put. More than a quarter of these would-be sellers (27%) reported a recent change in employment with a decrease in hours or pay, and 17% said they or their spouse/partner were laid off or involuntarily unemployed. Among sellers who may be considering putting their home on the market in the next three years, 6% said they are currently taking advantage of mortgage forbearance programs that allow them to delay or defer monthly mortgage payments.

Methodology

In this brief, "homeowners" refer to household decision makers who own their primary residence and have not moved in the past year.

Zillow Group Population Science collected a nationally representative sample of more than 1,000 homeowners (household decision makers that own their home and did not move in the past year). From September 29thto October 5th, 2020 the survey asked homeowners questions about their plans to sell and recent life events. Among those who did not have their home listed for sale (99% of the sample), the survey also asked why they were not currently selling.

To achieve national representativeness, quotas for age, ethnicity/race, education, income, region, relationship status, and sex limited oversampling of any given demographic group. In addition to quotas, ZG Population Science used statistical raking to weight the sample to the US Census Bureau American Community Survey 2018 sample of homeowners. Weighting used the same variables as the quotas. Margins of error are at a 95% confidence interval.

Existing home sales kept their summer surge rolling into September. Mortgage rates have increased recently, but by less than other data would suggest. And U.S. business activity rose strongly in October, raising hopes for a solid fourth quarter.

Existing home sales stayed hot in September

September existing home sales rose to 6.54 million (SAAR), up 9.4% from August and 20.9% from a year ago, according to the National Association of Realtors.

The median existing-home price in September was $311,800, up 14.8% from September 2019.

Stimulus talks and progress on virus treatment pushing U.S. Treasury yields up

The yield on the U.S. 10-year Treasury has risen steadily in the last week, and now sits at its highest level in 4 months.

Mortgage rates have also moved upward, but only slightly.

Business activity improved in October

The IHS Markit U.S. Composite Purchase Managers Index (PMI) – a measure of business conditions – rose 1.2 points from September to October, to 55.5.

A comparable index for the eurozone fell to 49.4 in October, suggesting activity abroad is contracting.

So what?

The impressive run for existing home sales continued into September, as buyers stayed their course in the face of the ongoing pandemic and an unrelenting inventory shortage. Building on an already strong pace set in July and August, sales figures in September rose at their fastest annual rate since 2010, when the housing market was just beginning its slow recovery from the Great Recession.Red-hot competition for the few homes available – fueled, in part, by low mortgage rates and a wave of millennials graduating into their home-owning years – has placed remarkable upward pressure on prices, particularly for single-family homes. Annual growth of single-family home prices has risen by more in the last three months than in any previously recorded period dating back to 1969. This torrid growth in sales may ultimately be done in by an inventory crunch that's only getting worse - its hard to keep setting sales records when there's so little for sale - forcing a slowdown in transactions in the coming months.But with demand for housing as high as it is, it's unlikely that a slowdown in sales will be substantial.

Recent optimism surrounding discussions about a new fiscal spending package, as well as positive developments regarding an approved treatment for COVID-19, are among the factors that have prompted a steady increase in U.S. Treasury bond yields over the last few weeks. The current yield on the U.S. 10-year Treasury bond sits at about 0.83% — still historically low, but the highest level in four months.Normally, an increase in Treasury yields would coincide with rising mortgage rates — but while mortgage rates have trended higher in the last week, the upward movements have been modest. One reason is that the normally-reliable relationship between Treasurys and mortgage rates has frayed during the pandemic: Mortgage rates have remained very low for the past several months, but they aren't as low as Treasury yields suggest they should be. The surge in mortgage demand has forced many lenders to keep rates higher than they otherwise could in order to keep the volume of requests manageable and also account for perceived levels of risk.While this limits the potential for mortgage rates to move notably lower, it also limits the risk of a sharp uptick in mortgage rates should this upward momentum in Treasury yields accelerate.

The IHS Markit PMI's October reading of 55.5 was its highest since February 2019 (any reading greater than 50 suggests conditions are improving from the previous month). But the report wasn't all rosy — companies noted that demand slowed slightly in October from September, particularly from overseas buyers.New business growth in the services sector also took a slight step backward on the month, continuing to improve but at a slower rate than in September. Still, these minor setbacks don't appear to have derailed business optimism – confidence in both the U.S. services and manufacturing sectors improved in October to their highest levels since May 2018. The picture overseas, meanwhile, is far less optimistic.Surging case volumes across Europe have placed new restrictions on commercial activity and prompted some fears of a double-dip recession. So while the improved business outlook is undoubtedly good news, developments elsewhere are a reminder that the virus will continue to dictate the path forward for the economy.

Click here to read past editions of Zillow’s Market Pulse updates.

With an epic Election Day coming up on Nov. 3, many homeowners may be inspired to express their political hopes and dreams by planting a presidential yard sign on their front lawn.

But is that really a good idea?

Given how dicey and divisive this political cycle has been, maybe we don’t need another reminder to vote for President Trump or former Vice President Joe Biden, because, let’s face it, a lawn sign won’t change anyone’s mind.

However, we think it’s safe to say that what we could all stand for is a little levity and laughter right at this point. It turns out that there are plenty of lawn signs that can deliver!

If you want to express your state of mind, while keeping politics out of it and preserving your relationship with your neighbors, consider getting one of these funny, fairly inoffensive lawn signs below. They’re guaranteed to get a chuckle from all who pass by without ruffling any feathers.

1. For those who just can’t take it anymore

Pandemic cry for help

Etsy

No matter where you fall on the political spectrum, we can all agree that this year has been rough.

Between a global health crisis (we’re looking at you, coronavirus), devastating natural disasters, an economic downturn, and a mountain of political mudslinging, if you’re so over 2020 (and we think that includes just about everybody), here’s the perfect sign to bring us all together (Etsy, $5.09).

2. For dog lovers

At least 50% of the neighborhood will agree.

Amazon

Now here’s a yard sign we can really get behind.

When you think about it, dogs have some really great traits that would make them great presidents—they forgive easily, offer unconditional love to those around them, advocate for naps, and don’t take life too seriously.

If you’re an animal lover, you need to let the world know with this humorous sign (Amazon, $24)—and you won’t offend anyone in the process (except maybe cat lovers). And they can always get their own version, shown up top, from Etsy for $37.49).

3. For ‘Star Wars’ fans

Get out your light saber!

Etsy

Even if you haven’t watched a single “Star Wars” movie, you’ve probably heard the quote: “Help me, Obi-Wan Kenobi. You’re my only hope.” (And in case you’re now curious, it’s from “Star Wars: Episode IV—A New Hope,” made in 1977.)

The expression seems fitting this year, especially when you consider all the chaos and turmoil that 2020 has sent our way. Can even Obi-Wan help us now, or are we too far gone?

Fingers crossed. Either way, this cinematic yard sign (Etsy, $16.90) just might make you feel better about our prospects.

4. For people who love to hate Karens

If you think your neighbors can take a joke

Etsy

We apologize to all the real Karens out there (it’s been an extra rough year for you, hasn’t it?), but this one was just too funny not to share.

The name Karen has recently become synonymous with a particular type of woman, typically a white, wealthy (or at least middle-class) woman, who isn’t afraid to exercise her privilege.

She might call the police on you for nabbing the last packet of organic tofu, or for just breathing too loud or standing too close while waiting for your latte at Starbucks. Suffice it to say, if you don’t vote for her, she’s going to need to speak to your manager, just like this sign says (Etsy, $12).

5. For rickrollers

Rick Astley’s a good stand-in.

Etsy

If you’ve never been “rickrolled” before, allow us to explain this joke. You see, there’s this funny prank that started on the internet but later made its way into real life.

To “rickroll” someone, all you have to do is trick someone into watching Rick Astley’s 1987 hit song “Never Gonna Give You Up” (this is usually accomplished by a misleading hyperlink that promises to deliver something else).

You can also pull off the prank by subtly incorporating the lyrics of the song into everyday conversation or by buying this yard sign (Etsy, $8.99). Sure, it might go right over some neighbors’ heads, but the ones who do get it will think you’re hilarious and hip with the times.

6. If you’re sick of presidential elections

At the end of your rope

Amazon

Or perhaps you think the Trump vs. Biden debate misses the bigger point.

If so, this sign (Amazon, $15.99) could help vent your frustrations and send out a clarion call: Is there anyone out there, anywhere, who can help lead us in the right direction?

7. If you wish the world would just end already

A cataclysmic choice

Etsy

Look, surely the world was in much better shape when the asteroid that killed the dinosaurs pummeled the Earth, right?

Somebody call NASA and see if they can work something out.

In the meantime, you can express your utter lack of hope in 2020 with this despairing yard sign (Etsy, $12.60).

8. If you’re sick of all the conspiracy theories

Let’s embrace the counterfactual.

Etsy

Conspiracy theories are rampant right now. So while we’re at it, why not revive the legend of Bigfoot? Stranger things have caught on (Etsy, $12.60).

9. If you’re not sure what to say

Calling anyone out there!

Etsy

You want to take a stand—but aren’t sure what’s worth fighting for anymore—or for whom.

If that sums up your feelings, this sign can help express your utter lack of direction (Etsy, $24).