Don't be in a rush to pay this off.

The post Do Student Loans Affect Credit Score? appeared first on RE: Find.

from Do Student Loans Affect Credit Score?https://ift.tt/2FKialB

Don't be in a rush to pay this off.

The post Do Student Loans Affect Credit Score? appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The wounds from January’s disappointing numbers may be still raw, but today's surprisingly upbeat figures offer at least a partial reprieve for the new home sales market and paint a promising picture for the coming months. The Northeast and Midwest were leaders for February. January's figures were released just two weeks ago as the Census Bureau played catch-up from the partial government shutdown-and they were a significant step back after two solid months at the end of last year. In fact, this trend of two steps forward, one step back, has been a consistent occurrence for much of the last twelve months. Declining mortgage rates, slowing home-value growth and stronger wage gains all helped February's figures put their best foot forward, improving would-be buyers' affordability and empowering them to enter the market. And while concerns about an economic slowdown have begun to appear, the builder pipeline is a long one that will take months to respond to these changes. With mortgage rates primed to stay low and more inventory coming on the market, expect rosy buying conditions — although possibly not such rosy numbers as these, given mounting economic uncertainty — to remain as we enter the busy shopping season.

The post February New Home Sales: No More Chill in the Air appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Is there such a thing as a zero score?

The post What Is the Lowest Credit Score? appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

A natural-looking and budget-friendly idea

The post How Accent Stone Can Transform an Older Home appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Even if they were to theoretically put no money down to purchase the median-valued home, a home buyer in 22 of the country's 35 largest metro areas could still make their monthly mortgage payments without spending more than 30 percent of their income (the rule of thumb) on housing.

But not in California.

The cost of housing in most major California metros has risen so high that the median household cannot reasonably afford a median-priced house, even with a 20 percent down payment.[1] To make ends meet on their monthly mortgage, typical California households either need to spend far more than 30 percent of their incomes on housing, or make a much larger down payment than the standard 20 percent.

Median annual household incomes in the pricey San Jose and San Francisco metros sit far above most areas: $124,300 and $107,600, respectively, compared to the national median of $63,300 per year. But that extra income is not enough to compensate for incredibly high local home values – the median home in San Jose has a value of $1.25 million, and in San Francisco it's worth $957,400. Even after putting 20 percent down, the $4,900 monthly payment in San Jose and $3,760 payment in San Francisco on those homes would still consume more than 30 percent of the typical household's income.[2]

To bring that monthly payment in San Jose down to $3,108 per month – within the 30 percent threshold – a home buyer making the median income in the San Jose metro would need to make a ludicrous down payment of almost 50 percent, or $614,100, on the median-valued home. To put that in perspective, the required down payment alone is more than the combined values of a high-priced home in Kansas City ($336,200) and Pittsburgh ($266,800) – to say nothing of the entry-level or even median home in those areas.

And for Silicon Valley home buyers willing to cut their budget and seek out one of the area's less-expensive homes, even affording a typical entry-level home in San Jose is nearly out of reach for a median-earning household. The largest loan they could afford without crossing the 30 percent barrier would be $631,700 — only 80 percent of that typical entry level home's value of $791,500, and still requiring a substantial 20 percent down payment of $159,800 up front.

Fortunately, the typical home nationwide remains largely affordable. The median U.S. home is valued at $225,300 and is well within the affordable range regardless of the down payment size. Even the typical renting household, which earns 18 percent less than the median U.S. household ($51,800/year), could still afford payments on the median U.S. home, regardless of how much money they put down. This is good news for savings-strapped renters who need to scrape together a down payment without the benefit of having proceeds from a prior sale.

But again, the picture for renters isn't so pretty in California, where median home values in all six major metros are so stratospheric that they're affordable only to renters who can make down payments between 30 percent (Sacramento) and 68 percent (San Jose). In those same six metros, to afford even a less expensive/starter home would depend on a median-earning renter having the savings for a hefty down payment.

| Metro Area | Median Household Income | Median Value of Expensive Home | Median Value of Mid-Range Home | Median Value of Starter Home |

|---|---|---|---|---|

| United States | $63,300 | $388,100 | $225,300 | $129,400 |

| New York, NY | $79,400 | $756,900 | $438,300 | $265,800 |

| Los Angeles-Long Beach-Anaheim, CA | $73,600 | $1,125,200 | $652,300 | $449,900 |

| Chicago, IL | $71,500 | $384,600 | $224,800 | $126,300 |

| Dallas-Fort Worth, TX | $70,400 | $405,800 | $242,600 | $152,600 |

| Philadelphia, PA | $71,600 | $404,000 | $232,700 | $119,800 |

| Houston, TX | $66,100 | $364,500 | $205,500 | $132,200 |

| Washington, DC | $103,600 | $700,900 | $406,200 | $251,700 |

| Miami-Fort Lauderdale, FL | $56,500 | $488,300 | $283,800 | $149,600 |

| Atlanta, GA | $68,000 | $404,400 | $217,500 | $131,300 |

| Boston, MA | $90,100 | $768,500 | $467,000 | $304,100 |

| San Francisco, CA | $107,600 | $1,638,200 | $957,400 | $557,900 |

| Detroit, MI | $61,000 | $314,900 | $160,000 | $45,900 |

| Riverside, CA | $65,300 | $531,500 | $367,100 | $246,500 |

| Phoenix, AZ | $64,700 | $436,200 | $264,900 | $183,900 |

| Seattle, WA | $86,100 | $845,100 | $489,700 | $317,300 |

| Minneapolis-St Paul, MN | $79,900 | $410,600 | $268,100 | $190,400 |

| San Diego, CA | $80,600 | $925,100 | $591,400 | $424,600 |

| St. Louis, MO | $64,300 | $305,900 | $167,000 | $72,300 |

| Tampa, FL | $54,100 | $359,800 | $213,600 | $128,400 |

| Baltimore, MD | $79,700 | $471,000 | $267,900 | $134,500 |

| Denver, CO | $80,500 | $604,300 | $405,300 | $299,900 |

| Pittsburgh, PA | $61,300 | $266,800 | $143,900 | $65,200 |

| Portland, OR | $75,900 | $575,400 | $397,300 | $301,900 |

| Charlotte, NC | $63,700 | $374,100 | $206,200 | $119,200 |

| Sacramento, CA | $71,000 | $606,800 | $408,700 | $290,600 |

| San Antonio, TX | $58,600 | $334,200 | $192,800 | $120,600 |

| Orlando, FL | $57,200 | $362,600 | $237,100 | $151,000 |

| Cincinnati, OH | $64,300 | $295,500 | $168,900 | $97,100 |

| Cleveland, OH | $54,200 | $265,900 | $145,600 | $71,400 |

| Kansas City, MO | $65,900 | $336,200 | $191,600 | $95,600 |

| Las Vegas, NV | $60,100 | $407,500 | $277,900 | $192,000 |

| Columbus, OH | $66,800 | $333,000 | $189,900 | $105,600 |

| Indianapolis, IN | $62,000 | $285,800 | $163,900 | $85,300 |

| San Jose, CA | $124,300 | $2,178,000 | $1,245,800 | $791,500 |

| Austin, TX | $76,800 | $502,000 | $308,200 | $213,100 |

[1] Savings and retirement funds make up a majority of down payment funding according to the 2018 Zillow Group Consumer Housing Trends Report https://www.zillow.com/report/2018/

[2] Principal and interest only, plus mortgage insurance for down payments under 20 percent. Otherwise, does not include taxes or insurance costs, which will add to the monthly total.

The post California Home Prices Are So High, Even High-Income Households Can't Keep Up appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

It might be time to go house hunting!

The post The Slowing Housing Marketing Brings Good News for First-Time Buyers appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Be sure to call credit card companies before you go!

The post How to Keep Your Money Safe When You Travel appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Can you up-light an architectural feature?

The post Exterior Home Design Ideas: Lighting and Accessories That Modernize appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

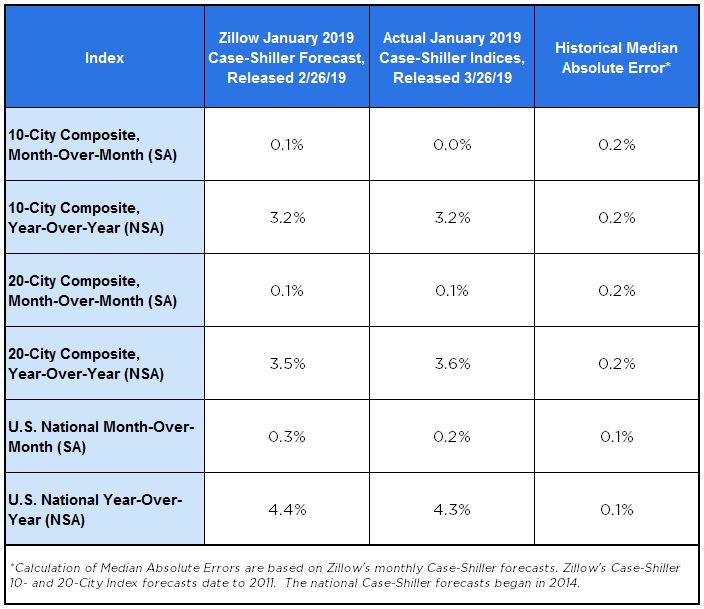

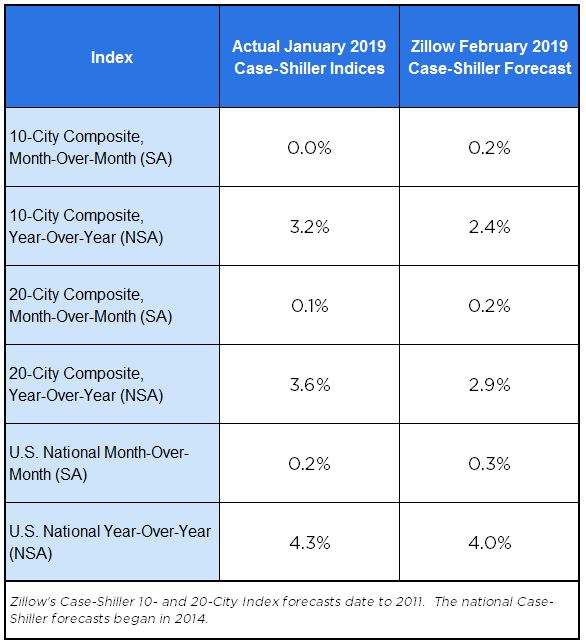

The national housing market's ongoing, slow march back to "normal" is continuing into the start of 2019 — setting up a spring in which buyers will have more power than they have in years, although they still may need to work hard to find a favorable deal.

House prices climbed 4.3 percent in January from a year early, down 4.6 percent from the prior month, according to the Case-Shiller home price index. The last time it advanced this slowly was April 2015.

Las Vegas, Phoenix and Minneapolis clocked the highest year-over-year gains on Case-Shiller’s 20-city composite, with annual growth of 10.5 percent, 7.5 percent and 5.1 percent, respectively.

Formerly scorching hot, in-demand markets have seen home value growth steadily slow over the past few months. In Seattle, annual price gains dropped from 12.8 percent to 4.1 percent from January 2018 to January 2019. San Francisco saw annual price increases shrink from 10.2 percent to 1.8 percent over the same time period.

Inventory levels continue to increase gradually, recovering from historic lows – an increasingly promising turn of events for buyers who had been starved for choice for years. And mortgage rates, continuing to retreat from recent peaks, appear primed to stay low for the foreseeable future.

This all puts would-be buyers in a far more favorable position than last spring. But don't cry for sellers: Prices are still growing, inventory remains incredibly low relative to demand, and buyers are out there in droves competing amongst themselves. The recent slowdown, then, should be viewed more as a healthy rebalancing than a dramatic shift in trends or an impending sign that the strong fundamentals the housing market is enjoying are about to collapse.

Here’s Zillow’s forecast for Case-Shiller’s February data release, which is scheduled for release on April 30.

The post January Case-Shiller Results and February Forecast: Lowest Gains Since 2015 appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

If you are used to getting a tax refund around this time of the year, you may have a surprise in store for you. Either your refund will be less...

The post Using Your Tax Refund to Pay Down Debt? Here’s Where to Start appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Winter weather had an impact on home construction in February, with housing starts taking a step backward from the momentum of January’s report. Many attributed January's strong release — which broke a streak of four straight monthly declines and improved market conditions for buyers — specifically to mortgage rates retreating from multiyear highs, a recovering stock market and a less ambitious interest rate outlook. Today's lackluster release is likely due to poor weather conditions, which led to a decline in construction activity and jobs from the month prior. What starts activity there was was driven largely by the volatile multifamily sector. The outlook for home construction should improve as we turn the corner into spring, but that could take longer in parts of the country where flooding continues into late March. Permits have shown strong increases in the past few months, and rosy market conditions remain.

census link: https://ift.tt/29BDoAx

jobs link: https://ift.tt/2iNRbae

The post February Housing Starts: appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Home shopping season is quickly approaching, which means home sellers are busy cleaning, painting, decluttering, landscaping and deciding which other projects might reap the greatest reward given limited time and money. Their best bet – once the curb appeal projects are done, tackle the bathrooms.

The typical seller has 13 years' worth of wear and tear on their home, and that can make it tough to know where to start. But we know they do: Sellers average 2.2 renovations or improvements to prepare to sell their home, with 79 percent making at least one[i]. And for good reason: Nearly a quarter of sellers who make improvements sell above list price, compared with 16 percent of sellers who don't.

The key is making smart decisions about what to upgrade, because home-improvement projects don't necessarily pay for themselves — and some improvements actually cost more than they return in value. This roundup of research on the return sellers get from a variety of projects shows that a smaller, inexpensive upgrade typically brings a bigger reward than a more involved and time-consuming one.

For the biggest payoff:

Less likely to pay off:

An important thing to consider is that these figures reflect national averages, not local real estate markets. The definitions of "mid-range" and "upscale" can vary widely from Manhattan, New York, to Manhattan, Kansas.

[i] Data from the 2018 Zillow Consumer Housing Trends Report.

[ii] Data from Zillow Talk: Rewriting the Rules of Real Estate.

The post Where Sellers Get the Biggest Bang for Their House-Prepping Buck appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Seek someone who specializes in your area of interest.

The post 5 Best Questions to Ask Before You Hire a Financial Planner appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Everyone needs a special place to get away.

The post Lake Houses for Sale, ‘Cause Summer’s Right Around the Corner appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

After a frigid start to the year, the spring thaw looks to be setting in on the market for existing homes. January's figures were disappointing, but many took solace in the fact that much of the lackluster activity was likely attributable to poor winter weather, uncertainty surrounding the government shutdown and still-high mortgage rates.

Would-be buyers clearly moved past these constraints and confidently stepped into the market across three of four regions reported on Friday. Single-family sales drove the gains, up 13.3 percent from January. With mortgage rates remaining low and inventory continuing to creep up, it's likely that this newfound zeal will carry into the busy spring season, even as home values continue to grow.

The post February Existing Home Sales: Nothing But Net appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

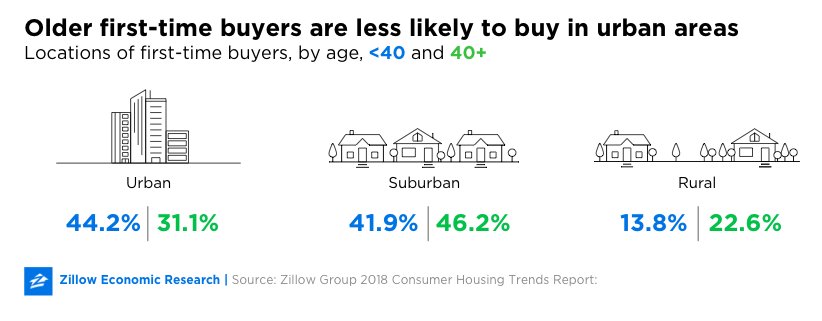

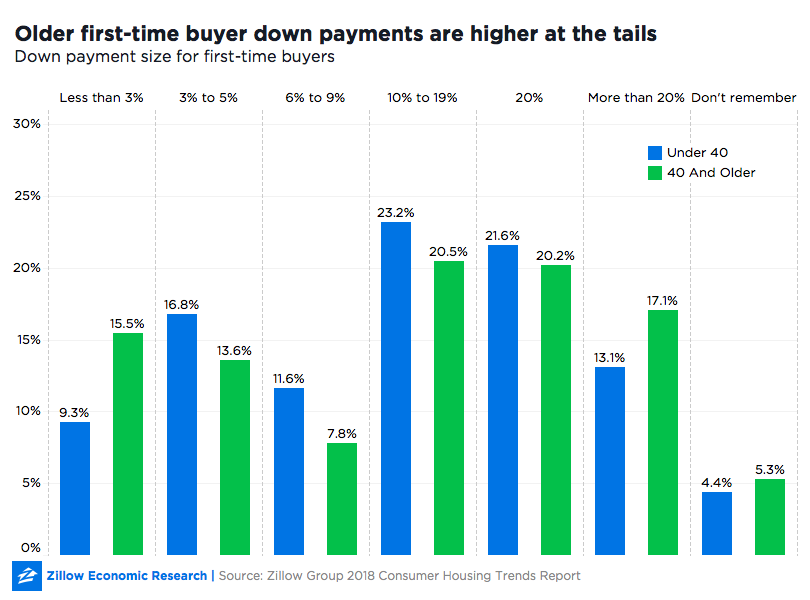

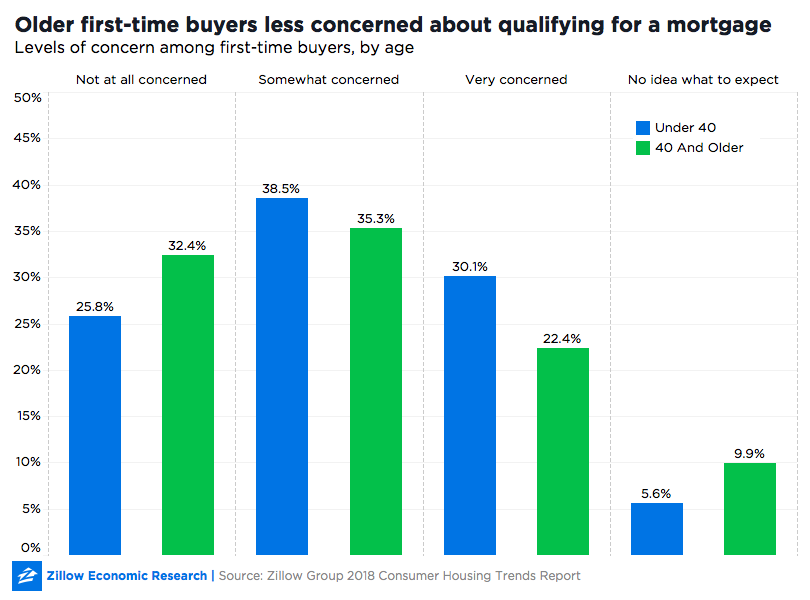

A common misconception is that the typical first-time buyer is in their mid or late 20s-but the real median age is actually 34, according to the Zillow Group Consumer Housing Trends Report. About a third (32.5 percent) of first-timer buyers are 40 and older and a non-trivial share (15.5 percent) are 50 and older. Since most research focuses on the millennial and Gen Z first-time buyer, this misconception can lead to confusion around the home and purchasing needs of older first-time buyers.

A diverse group: Lower incomes overall, and more likely to buy with cash

Younger first-time buyers (under age 40) often become homeowners as they are forming new households with partners and spouses and having children. They have higher median household incomes than older-first-time buyers (40 or older), and they are more likely to leverage gifts from family or friends to help with their down payments.

Older first-time buyers are a more diverse group with varied experiences. Some may have been financially able to purchase a home but continued renting into midlife and beyond for lifestyle reasons, such as wanting to move frequently or not be tied to a mortgage. They are more confident about qualifying for financing, are more likely to be cash buyers (22.9 percent compared to 11.7 percent of younger first-time buyers), and are less likely to go over budget than their younger counterparts.

At the other end of the spectrum, some could have been waiting until they saved enough for a down payment. As a group, older-first time buyers are less likely to have sources besides savings for down payments. They have lower median household incomes ($57,500 compared to $72,500 for younger first-time buyers)[1] and buy more modest homes than their younger counterparts. This group may lack social networks to help them through the process for the first time-the way many younger first-time buyers lean on their parents.

Older first timers also lean more toward suburban and rural areas than the younger cohort.

Buying a home comes with large upfront costs, and couples are often better positioned to save for a down payment because they are more likely to have two incomes. It's not surprising that the majority of first-time buyers are married or living with a partner or spouse, no matter what their age.

Beyond that, the family dynamics of older and younger first-time buyers diverge. Younger first-time buyers are more likely to never have been married (23.2 percent versus 16.8 percent of older first-time buyers), and the older group is much more likely to be separated, divorced or widowed (14.9 percent versus 1.2 percent of the younger group). Older first-time buyers also are less likely to have children under 18 living in the home (48.1 percent of older first-timers versus 59.9 percent of younger ones).

Family help with a down payment could be one reason younger first-time buyers are purchasing homes earlier in life: Almost half of them used a gift from family or friends toward down payments, compared with only about a third of older first-timers. In fact, about 60 percent of older first-time buyers funded their down payments from a single source, typically savings.

The size of their down payments also indicates a range of life experiences: Among first-time buyers who have mortgages, older first-time buyers are more likely to make down payments that are unusually low and unusually high.

Less than a quarter of older first-time buyers said they were "very concerned" about qualifying for a mortgage, compared with almost a third of younger first-timers. And their experiences with lenders match those expectations: Only 21.9 percent of first-time buyers at midlife and beyond were denied prior to qualifying for a mortgage versus 35.5 percent of first-time buyers under 40.

Still, almost twice as many older first-time buyers said they didn't know what to expect when applying for a mortgage (9.9 percent versus 5.6 percent for the younger group). Perhaps older first-time buyers are experienced enough to know when they don't know something. It's also possible this segment of older buyers may lack social networks to help shepherd them through the process the way parents can help younger buyers.

More than a quarter (27.4 percent) of younger first-time buyers go over budget in buying their starter homes, compared with about a fifth (19.9 percent) of older first-time buyers. The homes they end up with reflect that difference: Older first-time buyers purchase somewhat more modest homes (1,931 square feet with 3.1 bedrooms and 2.7 bathrooms) than their younger counterparts (2,000 square feet, 3.2 bedrooms, 3.5 bathrooms).

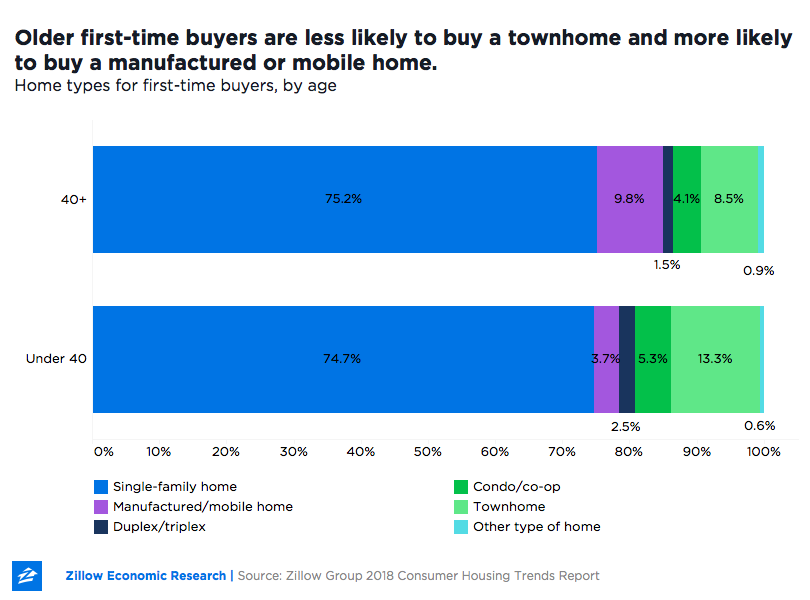

The single-family home is still the standard among first-time buyers of any age. The difference comes at the margins, with older first-time buyers more likely to buy a manufactured or mobile home-which could be related to their stronger preference for suburban and rural areas. Similarly, younger first-timers more likely to buy a townhome-which could be related to their propensity for urban living.

[1] Older first-time buyers have lower incomes if they are retired or in the later stages of their career. They also could have additional sources of assets and wealth.

The post Older First-Time Buyers Lean Suburban/Rural, Have Lower Incomes, More Likely to Pay With Cash appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

An overhyped stereotype about millennials is that they're entitled narcissists who can't be bothered to do homework, legwork or even stash a few dollars in the bank (see avocado toast). That caricature can be taken apart in many ways – including by research from the Zillow Group Consumer Housing Trends Report that shows millennial home buyers and sellers are extremely motivated: They go on more tours, give more open houses, do more research on real estate professionals, and fix up their homes at higher rates than older generations.

When buying a home, millennials go on more tours than their older counterparts. The average millennial goes on 4.4 tours — slightly more than Gen X and Baby Boomers — and outdoes the average of 2.7 for the Silent Generation.[1] They also attend more open houses: 42.7 percent of millennials go to at least two – a higher share of buyers than Gen X (30.4 percent), Boomers (24.9 percent), and the Silent Generation (16.3 percent).

When millennials use an agent, they still do more themselves. Among millennials that use an agent, 20.2 percent go on tours themselves, higher than the 12.2 percent of Gen X, 10.4 percent of Boomers, and 3 percent of the Silent Generation who do the same. Millennials selling their homes also give more tours on their own before getting their agents involved: 30.3 percent of them give tours to potential buyers before engaging an agent, compared to 18.1 percent of Gen X, 8.5 percent of Boomers and 10.1 percent of the Silent Generation.

Millennial buyers also do more research throughout the process. Among those who enlist the help of an agent at some point in their search, 37 percent of them preview or screen homes themselves, compared to 28.3 percent of Gen X, 29.6 percent of Boomers and 14.5 percent of Silent Generation buyers. More millennial buyers also identify the homes they consider: 42.6 percent, compared to 32.7 percent of Gen X, 29.5 percent of Boomers, and 10.3 percent of the Silent Generation.

When hiring the many professionals that play a part in the buying and selling processes, millennials are more likely to research and evaluate agents, contractors, inspectors, and other professionals. When looking for an agent, the average Millennial seller contacts 2.5 agents before settling on one – more than the 1.7 agents that Gen X and Baby Boomer sellers contact and more than the 1.4 that Silent Generation sellers reach out to.

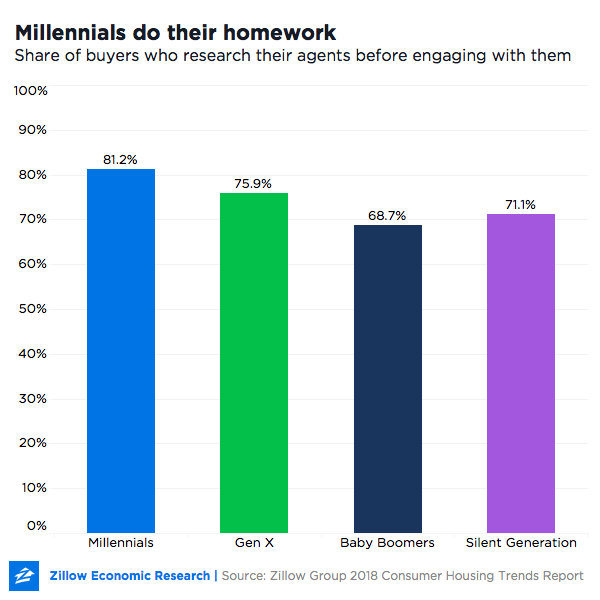

When searching for an agent to help them buy a home, 81.2 percent of Millennials do at least one of the following to evaluate them:

Older generations also research their agents, but at lower rates than millennials: 75.9 percent of Gen X buyers do at least one of the above, as do 68.7 percent of Boomers and 71.1 percent of the Silent Generation.

Among buyers who use an agent, millennials are more likely to find their own inspector than older generations: 22.5 percent of millennials find their own, compared to 17.2 percent of Gen X, 11.7 percent of Boomers and 11.6 percent of the Silent Generation.

The average millennial buyer also outdoes other generations when it comes to contacting lenders: Millennials contact an average of 2.8 lenders before choosing one, more than the 1.7 lenders contacted by Gen X, 1.8 by Boomers and 1.3 by the Silent Generation.

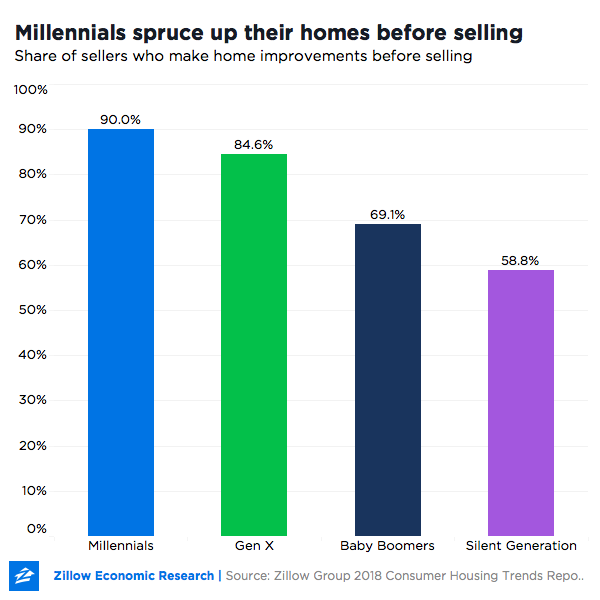

Millennials are more likely than all older generations to fix up their homes for sale. They outdo Baby Boomers and the Silent Generation when it comes to painting, redecorating, landscaping, replacing or buying new furniture, and kitchen and bathroom improvements. Ninety percent of Millennials do some sort of improvement, compared to 84.6 percent of Gen X, 69.1 percent of Boomers and 58.8 percent of the Silent Generation.

You might think millennials are doing more work because of the kinds of houses they own: If the houses are older, for example, they might need more repairs. But the data show that millennials sold homes that are on average about eight years newer than homes sold by older generations.

Millennial sellers that use an agent are also more likely than older generations to do a lot of the work that agents often handle. For example, millennials are more likely to have photographs taken of their home: 31.7 percent do, compared to 18 percent of Gen X sellers, 11.4 percent of Boomer sellers and 4.3 percent of Silent Generation sellers. In addition to photos, millennials also make print ads and have video or other media taken of their homes at higher rates. Given how tech savvy they are, it's no surprise that they're big on promoting their homes on real estate sites (22.7 percent) at nearly triple the rate of older generations (8.5 percent) and on social media (38.0 percent compared to 15.5 percent for older sellers).

Seventy-eight percent of millennial sellers are doing so for the first time; this is their first rodeo. The fact that they're overwhelmingly learning the ropes for the first time may partially explain why they are doing more work: 58.1 percent of them have at least one offer fall through, compared to 37.9 percent of Gen X sellers, 30 percent of Boomer sellers and 22 percent of Silent Generation sellers. Because a large proportion are first timers, they also are less likely to have an established network of professionals to rely on, which means they have to do more research to find a team.

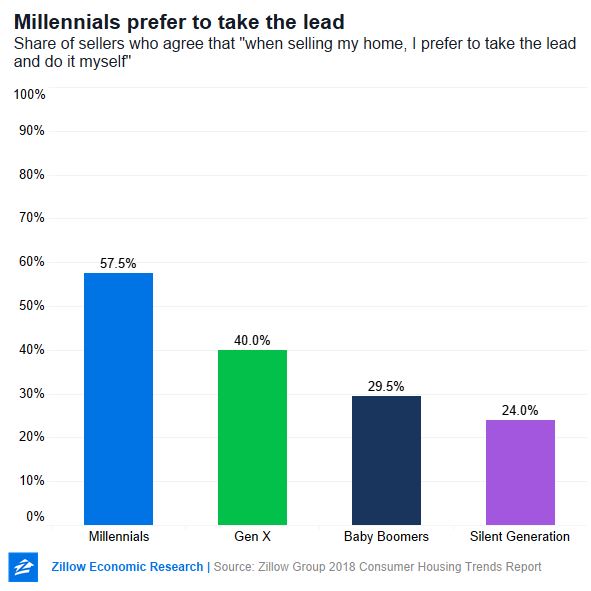

Even so, they are more eager than older generations to do work themselves. When asked whether they prefer to take the lead themselves or rely on guidance from professionals, 57.5 percent of millennial sellers say they are more inclined to take the lead themselves – a higher percentage than older generations. Among Gen X sellers, 40 percent report taking the lead, compared to 29.5 percent for Boomers and 24 for the Silent Generation. This preference may explain why millennials often outdo older generations when it comes to the homework, fixing up and other jobs associated with the home selling process.

[1] Millennials refers to people between the ages of 24 and 38. Gen X is 39 to 53. Baby Boomers are 54-73. Silent Generation refers to people age 74 and up.

The post 'Lazy' Millennials Do More Work When Buying & Selling Homes appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

| Median Home Value: $213,600 |

| Share of Listings With a Price Cut: 24.8% |

| National Population Rank: 19 |

| Median Home Value: $277,900 |

| Share of Listings With a Price Cut: 23.9% |

| National Population Rank: 30 |

| Median Home Value: $264,900 |

| Share of Listings With a Price Cut: 20.9% |

| National Population Rank: 14 |

| Median Home Value: $217,500 |

| Share of Listings With a Price Cut: 15.9% |

| National Population Rank: 9 |

| Median Home Value: $237,100 |

| Share of Listings With a Price Cut: 21.3% |

| National Population Rank: 27 |

| Median Home Value: $283,800 |

| Share of Listings With a Price Cut: 18.6% |

| National Population Rank: 8 |

| Median Home Value: $160,000 |

| Share of Listings With a Price Cut: 16.5% |

| National Population Rank: 12 |

| Median Home Value: $242,600 |

| Share of Listings With a Price Cut: 18.7% |

| National Population Rank: 4 |

| Median Home Value: $253,500 |

| Share of Listings With a Price Cut: 14.9% |

| National Population Rank: 35 |

| Median Home Value: $206,200 |

| Share of Listings With a Price Cut: 16.4% |

| National Population Rank: 24 |

The post Best Metros for First-Time Buyers appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

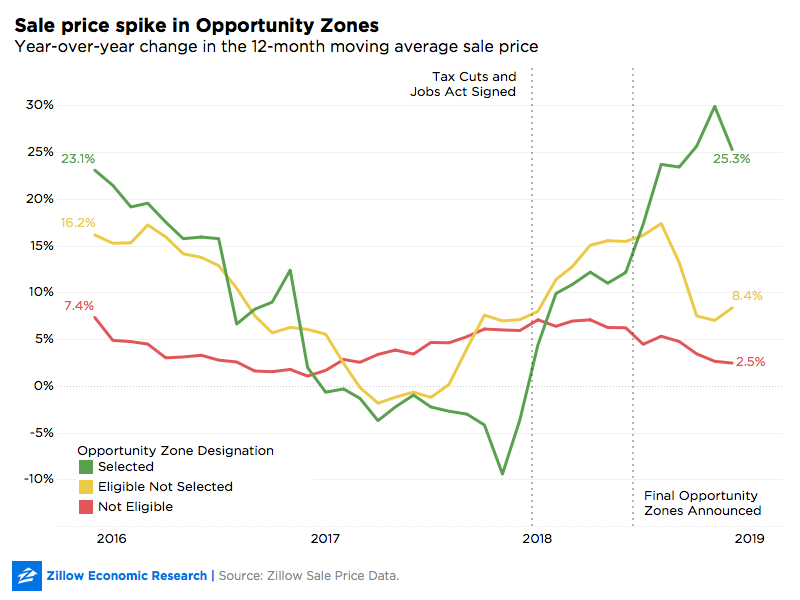

Sale prices ticked up sharply in some of the nation's lowest-income and highest-poverty communities near the end of last year-but mostly in the neighborhoods now eligible for newly created tax breaks.

Tucked within the Tax Cuts and Jobs Act of 2017 (TCJA) is a somewhat overlooked, but potentially massive, program: Opportunity Zones. Investors have flocked to these designated zones since last summer, when the Treasury Department certified the final batch of 8,700 census tracts selected by state governors.

The zones – a collection of low-income or high-poverty census tracts scattered across all 50 states and Washington, D.C. – offer potentially large tax savings for investors who fund projects in these communities. A laundry list of rules and regulations detail the precise qualifications for eligible investments, but the bottom line is that capital gains from other ventures that are funneled into Opportunity Zones eventually can be rewarded with up to a 15 percent discount on taxes they would have owed otherwise. And if that deal wasn't sweet enough, investors who keep their money in the Opportunity Zone for at least 10 years avoid all capital gains taxes on profits from the Opportunity Zone investment.

The rationale behind the zones is relatively simple. Proponents argue that a lot of the wealth currently generated as capital gains could be put to good use as seed money in traditionally neglected communities shut out of investment – ideally revitalizing infrastructure, fueling economic growth, and spurring job creation and overall prosperity. But whether this tax break will direct funds to the communities that need them the most – or what happens when money arrives – are open questions.

Researchers contend that the particular tracts that were chosen as Opportunity Zones could determine whether the policy succeeds. Skeptics of Opportunity Zones argue a lax regulatory system and selection criteria can provide costly tax breaks for developments in areas already attractive to investors, essentially subsidizing projects that would have happened regardless of a tax break. Others fear the incentives may concentrate residential redevelopment in communities already vulnerable to gentrification and displacement, without many guardrails to mitigate undesirable outcomes.

We are still in the program's infancy, so these promises and fears are mostly theoretical. While it's still early, we already see some signals that folks have begun to take up Uncle Sam on his generous offer. Compared to similar tracts that were not selected, real estate sale prices are increasing at a faster rate in Opportunity Zones following their selection.

It appears the year-over-year change in sale prices for all eligible zones (selected or otherwise) were increasing months before the TCJA was passed, but the divergence after the final selection of Opportunity Zones provides an early signal of demand. In other words, the yellow and green lines moving upwards together in late 2018 may not have been solely due to TCJA and may indicate broader real estate trends in low-income areas. However, after the tracts composing the green line actually became Opportunity Zones, their sale prices took off. Similar analyses found surging sale values in land categorized as development sites within Opportunity Zones.

We calculated the 12-month moving average sale price in each month through the end of 2018 for each category, including all arm's length transactions where sale price data were recorded. We then calculated the year-over-year change in that moving average. Because real estate data are subject to seasonal variation, a 12-month moving average avoids putting too much weight on any one month that might have been subject to idiosyncratic shocks not related to market fundamentals.

For the most part, until selection of all Opportunity Zones, the selected tracts and the rejected tracts displayed generally similar price trends. During the period between the passage of the Tax Cuts and Jobs Act and the selection of Opportunity Zones, the year-over-year change in average sale prices grew between 10 and 15 percent in the eligible tracts, regardless of whether they were ultimately chosen as Opportunity Zones. However, in the months immediately following the final selection of Opportunity Zones, the price trajectories diverged. Sale prices in eligible but not selected tracts began growing more slowly and by single digits, whereas sale prices in Opportunity Zones started growing by more than 20 percent year-over-year.

It's crucial to note that Opportunity Zones are still very much in their infancy, and we are measuring very early signals of how the tax breaks may correspond to real estate trends. It remains to be seen whether this uptick in Opportunity Zones is a flash in the pan, or the start of something larger.

It's also very likely that the big money hasn't even started pouring into these zones yet, as many funds may watch from the sidelines until more rules and regulations are hammered out. If that's the case, signals we see in transaction data now might be drowned out in the coming months if waves of new capital begin pouring in.

Finally, while changes in average sale prices provide one lens for viewing investment demand for certain types of property, they are an incomplete measure that will need to be expanded upon as we track this policy in the coming months.

The post Sale Prices Surge in Neighborhoods With New Tax Break appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Are you making the most of your rewards?

The post 3 Smart Ways to Use Your Credit Card Points appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

And what to do if you lose them!

The post What Documents to Keep After Buying a Home appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Today's data are a bit of a kick to the gut after the market seemed to have built some momentum last month, but it shouldn’t come as too much of a surprise given the state of the country in January. The partial federal government shutdown and the harsh winter weather that affected much of the country both weighed on economic activity. But our bet is that buyers will prove resilient as winter turns to spring, and throw their hats into the ring with the benefits of falling mortgage rates, falling home prices and rising inventory. As the weather warms, accompanied by still-falling mortgage rates and additional new homes, the icy conditions that buyers faced in the fall and winter appear to be thawing.

The post January New Home Sales: A Kick in the Gut appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

For a while last year, it looked like the U.S. rental market might be headed for a serious slowdown. Year-over-year rent growth dipped below 1 percent – and then it stopped growing altogether. In September and October, the U.S. median rent was lower than it had been the previous year – the first time the market had posted annual declines since July 2012.

Now that rent growth has picked up again – to a moderate pace compared to the breakneck growth of earlier years – it appears we're in for a more vanilla, slow-growth market going forward. During last year's short-lived correction, landlords began to contend with the fact that rental supply finally started to catch up with demand. As we enter the 2020s, the number of 20-somethings will fall and more millennials will move on to homeownership, which could translate into less demand for rentals.

Nationally, median rent rose 2.4 percent ($34) year-over-year to reach $1,472 a month in February.

Many of the country's largest metro areas posted modest year-over-year gains of less than 3 percent in both January and February. The fastest gainer in both months was Orlando, Fla., where the median rent rose 7.4 percent year-over-year in January and 7 percent in February. Phoenix was not far behind, climbing 6.2 percent in January and 6.8 percent in February. The third fastest-growing market was Riverside, Calif., climbing 6.1 percent year-over-year in January and 6.2 percent in February.

New York renters have yet to see an effect from Amazon's decision to not build a new headquarters in Long Island City. Its rent prices, along with those in Washington, D.C., and Nashville – two markets where Amazon still intends to build large office spaces – have largely followed national trends since the November announcement.

The priciest major metro in the country remains San Jose, Calif., at $3,547 in February, up 1.4 percent from a year earlier. It's followed by San Francisco at $3,448 a month (up 1.6 percent), Los Angeles at $2,835 a month (up 3.5 percent), San Diego at $2,643 a month (up 4.2 percent) and New York at $2,419 (up 1.2 percent).

The lowest rent prices among major metros in February were Pittsburgh at $1,100 a month (up 4.9 percent), St. Louis at $1,155 a month (up 1.6 percent), Cleveland at $1,162 a month (up 1.7 percent), Detroit at $1,225 a month (up 2.3 percent) and Indianapolis at $1,234 a month (up 2.7 percent).

Home values nationally continue to soar – up 7.2 percent in February from the prior year. That's slightly below January's year-over-year growth rate of 7.8 percent but remains a strong clip, putting the median U.S. home value at $226,300.

Four major metros posted double-digit annual growth in February, led by Indianapolis, which climbed 12.8 percent to $165,600. It was followed by Atlanta, up 11.1 percent year-over-year to $218,600; Las Vegas, up 10.5 percent to $279,600; and Dallas-Fort Worth, up an even 10 percent to $244,400.

The priciest large markets in February featured the usual West Coast lineup – and also happen to be the only major markets without month-over-month appreciation: San Jose at an eye-popping $1.23 million (up 3.3 percent year-over-year), San Francisco at $955,200 (up 3.5 percent), Los Angeles at $652,200 (up 2.5 percent), San Diego at $590,500 (up 2.1 percent) and Seattle at $491,500 (up 3 percent).

The list of least expensive major markets for home values is the same as for rents, but in a different order: Pittsburgh at $144,400 (up 5.2 percent year-over-year), Cleveland at $146,300 (up 6.2 percent), Detroit at $161,300 (up 8.2 percent), Indianapolis at $165,600 (up 12.8 percent) and St. Louis at $167,100 (up 5.4 percent).

After starting the year on a strong note for buyers, inventory climbed even faster in February – albeit still at a modest 1 percent from a year earlier – an increase of 16,137 homes for a total of 1.6 million listings.

Mortgage rates listed on Zillow were mostly flat in February. Rates ended February at 4.16 percent, down one basis point from the start of the month.

The post Rent Growth Climbing Again After Brief Slowdown (February 2019 Market Report) appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Is it taking forever to tour the home?

The post 8 Signs of a Difficult Home Seller appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Better scores = better financing.

The post Consequences of Bad Credit: Beyond Sky-High Interest Rates appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

In a bidding war, this could give you an edge.

The post Right of First Refusal and the First-Time Home Buyer appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

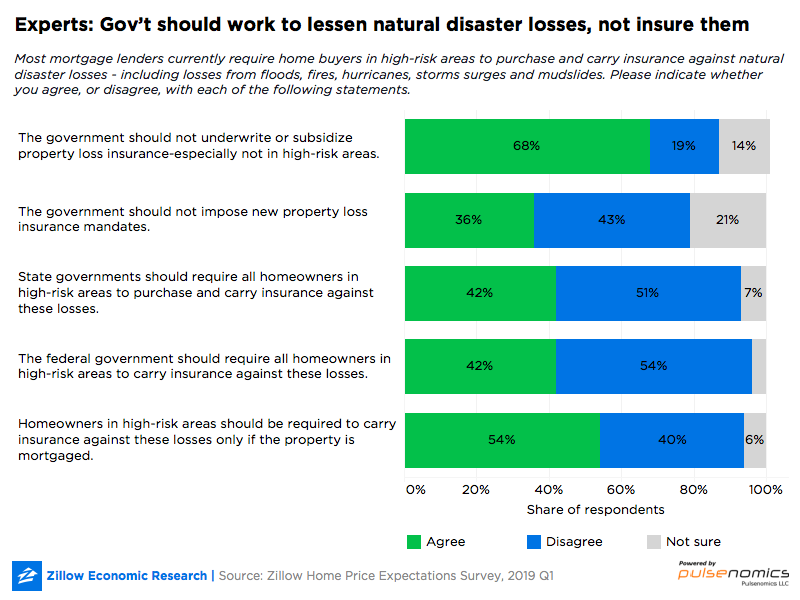

There are two sides of the coin when dealing with potential residential losses from more frequent natural disasters in coming years – trying to prevent those losses in the first place, and insuring them if and when they do occur. Federal and state governments can help with the former but should largely refrain from the latter, according to a Zillow survey of economists and real estate experts.

Panelists were asked for their opinions of different approaches to insuring and mitigating the impact of natural disasters; to offer their expectations for home value growth over the next five years; and for their expectations around the impact of a spate of expected 2019 IPOs on the Bay Area housing market. The Zillow Home Price Expectations Survey is a quarterly survey of more than 100 real estate experts and economists, sponsored by Zillow and conducted by Pulsenomics.

More than two-thirds of panelists (68 percent) said they agreed with the statement that "the government should not underwrite or subsidize property loss insurance – especially not in high-risk areas." Similarly, less than half (42 percent) of respondents said they agreed that federal/state governments should require all homeowners in high-risk areas to carry insurance for natural disaster losses.

Nor did the panel say they thought the government should provide financial assistance to help homeowners afford adequate insurance coverage; offer affordable coverage for a wider variety of disasters beyond floods; and/or require private insurers to offer affordable insurance to homeowners. Only 26 percent of the panel favored these insurance-based options.

"I think there is a role for government in the disaster insurance market, particularly in zones of some risk or as a backstop to private insurance," said one panelist.[1] "But subsidizing building in high-risk zones by providing cheap insurance is not one of them."

Instead, for those homeowners in high-risk areas that can't find coverage and/or can't afford higher premiums, a large plurality (47 percent) of the panel suggested a direct, if difficult, alternative: Those homeowners should sell their homes and move to a lower-risk/more-affordable place. Given the high expenses associated with moving, this would be particularly challenging for lower-income Americans who live in high-risk areas.

But the experts were more supportive of pre-emptive policies designed to prevent or mitigate damage in the event of extreme natural disasters, including floods, fires, landslides and storms:

Over the past several years, California's Bay Area – largely encompassing the San Francisco and San Jose, Calif., metro areas – has been among the nation's hottest housing markets. But while home value appreciation there remains robust, it slowed considerably in 2018 – from an annual pace of 8 percent to 7 percent in San Francisco, and from 16.8 percent to 9.9 percent in San Jose.

But a number of local tech firms – including Uber, Lyft, Airbnb and Slack – are preparing to go public this year, which could inject a lot of wealth into the area as employees cash in on long-held equity. Many of those employees may choose to purchase homes, which may impact the local housing market – as has happened in the past following large IPOs. Given this, panelists were asked to offer their expectations of the impact of these IPOs on the Bay Area real estate market.

A large majority – 82 percent of those offering an opinion – said any IPO-related stimulus will be modest and temporary and not enough to reverse the localized slowdown. Just one in 10 said the IPOs would stimulate the local market enough to reverse the slowdown.

Finally, panelists said they expect U.S. home values to grow 4.3 percent in 2019, on average – down from current annual growth of 7.5 percent (as of January 2019). Growth is expected to slow to 2.8 percent in 2020 and to 2.5 percent in 2021, before picking up to 3 percent and 3.4 percent in 2022 and 2023, respectively.

[1] Panelists' open-form responses to ZHPE supplemental questions are kept anonymous.

The post Experts: Gov't Should Work to Lessen Natural Disaster Losses, Not Insure Them appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

It didn't take long for the wounds left by December's starts and permits data to heal. The previous month's disappointing release – announced just ten days ago – showed single family starts sink to their lowest level in over two years. We’re still seeing some year-over-year declines, but it takes some time for builders to adjust to different market conditions, and it’s likely real progress won’t be seen in the data for a few months’ yet, once the headwinds from late 2018 are fully in the rear view. But today's figures were a marked improvement and a signal that builders are finally in the position to take advantage of more forgiving market conditions created by easing headwinds such as retreating mortgage rates, the stock market's recovery and a less ambitious interest rate outlook. What's more, January new home sales ticked up, albeit to still historically low levels, allowing builders to offload inventory that had been piling up for much of the last year. It was a difficult end to 2018, but builders appear primed for better days ahead.

The post January Housing Starts: Wounds Continue to Heal appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Establishing "conditions" protects you from disaster.

The post The Art of the Home Sale Contingency appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The cooling of the housing market that started last year — more of a normalizing than an actual correction — is actually the third time the market has slowed since it bottomed out in 2012. The first came in early 2014 and early 2016 — and this most recent cooling began in May 2018.

The latest dip is widespread, happening across 30 of the largest 35 metro areas, according to the Zillow Buyer-Seller Index. It shows San Jose, Calif., is the fastest-cooling major metro area, which is down 7.1 points to 2.2 on a 10-point index that compares markets to their own performance over time. That precipitous drop makes San Jose a downright cold market, favoring buyers over sellers.

Even if the locals remember hotter times, to the rest of the world, San Jose continues to appear white-hot — and compared to other metros, it is: On the cross-metro index, it's at 9.99 out of 10.

While home values and prices are starting to reflect the slowdown within markets as well, the buyer-seller index is a more robust measure encompassing three metrics: the share of listings with a price cut, how long listings sit on the market, and sale-to-list price ratios.

Among the largest 35 metro areas, there are three general trends since 2012:

All three sets, like the national market, started to slow in the spring of 2018.

In fact, only five of the country's 35 largest metro areas have not cooled since May: Recession casualties Detroit and Phoenix continue to heat up, likely because home prices there took such a tremendous hit during the housing bust. The other three that are not cooling are New York, Philadelphia and Pittsburgh.

Over the past year (since January 2018), the U.S. housing market has cooled by 5.1 points to 8.7 on the index. The dip has been far more precipitous in some metros: In 6 of the 35 largest markets, conditions have swung from favoring sellers to favoring buyers, compared to historical norms. Denver and Dallas join four California markets on this list.

As the San Jose example shows, markets can look a lot different compared to each other than compared to themselves over time. New York is another example: While the New York metro area tops the list of best markets for buyers when compared to other metros, it's heated up a touch in past year compared to its own history, climbing from 8.8 to 9.4 on that 10-point index.

Sellers markets are a similar story. While San Francisco, San Jose and Seattle lead the list of major sellers markets — they are among the fastest cooling markets compared to their own histories.

Here's a more detailed description of the Zillow Buyer-Seller Index. For this analysis, unsupervised clustering on the largest 100 U.S. metro areas was performed using hierarchical clustering and a Euclidean distance matrix. Inner-cluster variance was used to inform threshold decisions.

The post Most Major Metros Have Cooled Since May 2018 appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

A steady paycheck is so important.

The post What Income Can Be Used to Qualify for a Mortgage? appeared first on RE: Find.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Today’s new home sales data from December likely reflect closed transactions that were pending in November, transactions begun when interest rates were near their recent highs and builders were aggressively cutting prices in response. The strategy largely appears to have worked, with sales volumes coming in better than expected — at least on the surface. Prior months’ activity was revised sharply downward, and sales ended 2018 below where they ended 2017. New homes selling in December were likely permitted for construction in the Spring or early Summer, when the 2019 economic outlook was worse than now. But more favorable conditions may be on the horizon: Building permits increased in December, and buyers appear responsive to conditions that are more favorable now than they were just a few months ago, when rates were climbing and the government shutdown loomed large. And price cuts are still relatively frequent, particularly in larger markets, which may goose sales volumes as prices fall within the budget of more buyers. Its been a disappointing fall and winter, but the sun is coming back soon.

The post December New Home Sales: Better Days Ahead? appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

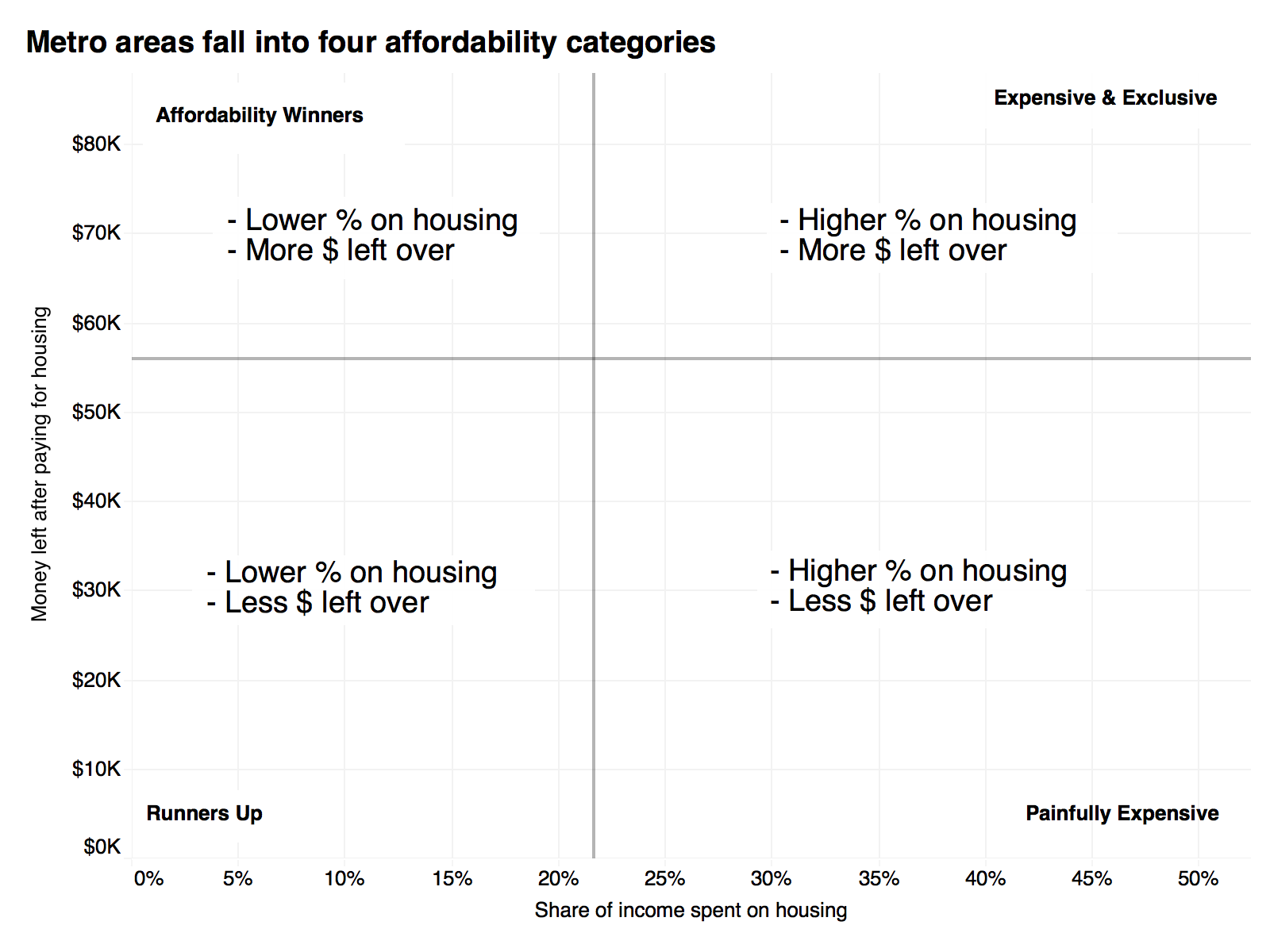

It's a general guideline that people should not spend more than 30 percent of their incomes on rent or a mortgage. That ratio leaves room to buy food, clothes and other items without creating too much financial stress.

In some parts of the country, staying below 30 percent is a breeze. In others, it's all but impossible. Rather than just report what the percentages were for each market in the fourth quarter 2018, we decided to look at how much money is left over after the median-earning household pays the typical rent or mortgage in the largest metro areas. Those dollars clearly go further in some places than in others – but seeing how much people have left in the bank after housing is covered each month tells the story from a different angle.

The major U.S. metros fall into four affordability categories:

In these markets, median-earning households spend a high percentage of their income on the typical rent or mortgage, but still have a solid amount of money left over.

These metros prove that having a lot of cash left over does not necessarily mean an area is affordable.

A good example is San Jose, Calif., the major metro where median-earning households have the most money left over – $81,880 a year – after paying the median rent. The median rent takes up 34.1 percent of the median income – making San Jose one of the least affordable major metro areas in the country.

Even that 34.1 percent figure is low for many San Jose renters: For lower-income households in the metro area, a lower rent price still would consume 99.8 percent of their incomes[1] – which is financially impossible and requires people to find roommates and make other lifestyle decisions to live there.

Other expensive and exclusive metros include Boston, San Francisco and Seattle.

These are markets where households earning the median income and paying the median rent price spend a smaller share of their income on housing and have more dollars left over.

The market with the second highest amount of money left over after rent is Washington, D.C., at $77,738 a year – but median-earning renters in D.C. pay just 25 percent of their incomes on the typical rent. That's partly because the median household income is so high, and because the metro area covers much of Virginia and Maryland, where median rents are not as high as they are in the city center.

Other metros where typical renters have at least $50,000 a year left over – after spending no more than 27 percent of their incomes on rent – are St. Louis, Kansas City, Mo., Atlanta, Columbus, Ohio, Dallas-Fort Worth, Philadelphia, Chicago, Baltimore and Minneapolis-St Paul.

In these metros, people typically pay a smaller share of their incomes on the average rent or mortgage — and have fewer dollars left over.

They include a handful of metros in the Southwest and Midwest, including Pittsburgh, where the median-earning household spends 21.4 percent on the area's typical rent and has $48,172 left over. It's possible that that amount of money goes further in some metros than it would in markets with higher costs of housing – but that's not necessarily the case and will vary by market, along with taxes, childcare and other costs.

These metros have the worst of both worlds: median-earning households spend a higher share of their income on housing and have less money left over.

In Los Angeles, renters spend 45.7 percent on the typical rental and $39,926 a year left over. And while homeowners at the national level tend to spend a smaller share of their incomes on mortgages than renters do on rent, the situation for homeowners in Los Angeles is almost as bad: They pay 43.7 percent of their incomes on the typical mortgage – using current home values, so this applies mostly to people who recently bought a home – and still have just $41,426 left over.

The situation for lower-income renters and homeowners is predictably worse: People earning lower incomes in Los Angeles would have to pay 121.2 percent of their incomes on a typical lower-priced rental. They would have to pay 83.8 percent of their incomes on a mortgage for a lower-priced home priced.

While this analysis excludes federal, state and local taxes, it's important to note that taxes mean that a homeowning household in Austin, Texas, would keep more of its income after taxes than one in San Diego.

The calculation for a household in San Francisco making the median income shows it would be left with $71,152 after paying income and payroll taxes. Spending the typical 44.2 percent of its income on a mortgage would leave it with $26,674 in spending money — less than half of what it would have after subtracting the mortgage cost alone.[2]

That same calculation can be done for a variety of services, including childcare. According to a Hotpads analysis, in some metros, households pay more for childcare than they do for rent.

Even in areas where childcare is cheaper than housing, it still represents a large chunk of a household's budget. The average household in San Francisco pays about $24,000 for the service. A typical renter there paying that amount would see their post-housing income drop from $66,423 to $42,423.[3]

Following up from the tax example above, a San Francisco homeowner with the median income paying the typical mortgage would be left with $2,674 a year to cover all other expenses after paying for childcare, taxes and the mortgage.

Metros with high fuel costs and less transit, like Los Angeles, also represent a higher cost of living than those with more robust transit systems, like Chicago or New York.

While San Francisco households pay, on average, $1,676 a year on public transit and $8,276 on transportation in general, including for cars, they still spend less overall on transportation than their Los Angeles counterparts — who pay 21.9 percent more on transportation. For a median-income household there with all the expenses mentioned above, this added cost would put them in the red.

Transportation also chews into household budgets in metros like Detroit with high car insurance costs. Detroit residents spend, on average, $4,458 a year on vehicle expenses like insurance (excluding car payments and fuel) — 85 percent more than households in Chicago, a fellow midwestern city.

The grand sum of expenses in high-cost metros can be a financial burden, even to middle-income households. In some metros, the typical sum of housing, taxes, childcare and transportation can exceed the median income, without even factoring in other necessities like the cost of food, education, and healthcare.

[1] SmartAsset Income Tax Calculator for a household filing as Single https://ift.tt/1IhBWQq

[2] According to Care.com's Care Index from https://www.care.com/care-index. These are 2017 numbers adjusted for 2018 inflation.

[3] Base on the most recent tiered data, from the second quarter 2017.

The post Which Metros Leave Households With the Most Money After Housing? appeared first on Zillow Research.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

We all love a house-flipping reality show - we shout our opinions and weep when we see the final reveal. It’s an innate human instinct to want to make things better. And when it comes to selling your own home, it’s often a good instinct to follow.

But while it may be OK to max out the budget on a reality TV show, pulling out all the stops in your own home renovation might not be the best choice. Depending on the real estate market, your neighborhood and what buyers are looking for, you may need to do less - or more - than you think.

Before you demolish all the walls, take these four considerations into account.

Does your local market favor buyers or sellers? You can tell the difference by looking at trends on Zillow, talking to a real estate agent or checking out nearby neighborhoods.

If a lot of nice for-sale homes in your area haven’t sold, it’s likely a buyers market. This means that shoppers have many homes to choose from, so the ones with the nicest updates, lowest prices and better neighborhoods will go first, leaving a lot of homes sitting idle on the market.

If homes are selling right and left, then it’s a sellers market. In this case, there aren’t as many homes for buyers to choose from, so sellers can often get above asking price as a result of bidding wars.

If you’re thinking about selling your home, understanding what the market is doing will help you determine how much you need to upgrade your home.

If it’s a buyers market, you’ll likely need to do more to your home to stand out. The average garage door replacement costs around $1,600, but if it makes your home stand out and sell faster, it may be a good move.

If it’s a sellers market, you can get away with upgrading less, since homeowners will be competing for your home regardless of how tricked out it is. Spend your money wisely on things like new counters or fixtures, and spruce up the rest with a fresh coat of paint and some elbow grease.

The next important factor is your neighborhood, because you don’t want to price yourself out of it. Do you live in a new development? Or an older one where the homes are 40, 50 or 60 years old? Do you have a homeowners association that will limit what you can do? Or can you renovate at will?

In older neighborhoods, you don’t want to renovate your house so much that it looks out of place or becomes a target for theft. You want to find a nice balance.

If most homes in your area have dated finishes, focus on a few crucial updates that’ll help your house stand out and stay within your neighborhood’s average pricing. People are less willing to buy a $475,000 house in a neighborhood where homes don’t usually sell for more than $300,000.

A good rule of thumb: Don’t raise your home’s value any higher than 10 percent of the average cost of homes in your neighborhood.

However, if you live in a nicer area and your house is the shabbiest on the block, you’ll want to spend a little more to keep up. Take a look at homes in your neighborhood that have sold in the last 90 days (you can find this right here on Zillow). Emulate the finishes those homes have while remaining within your budget.

Give your home the features buyers look for most. Many homeowners look for updated kitchens, master bedrooms and bathrooms. These three spaces alone can sell your home, so consider investing extra money in these areas.

If you have additional funds, consider replacing flooring or upgrading small things like lighting, fixtures and doorknobs.

Use your budget wisely, and consider going the DIY route - some projects can recoup a large part of your investment! If brand-new kitchen cabinets are out of your budget - or if they’d price you out of your current neighborhood - consider painting your current ones.

Of course, watch for sales or deals on things you can use in your renovations. Regardless of how old or new your neighborhood is, choose timeless styles and colors that will appeal to a wide range of home buyers.

If you do your market research and follow the trends, you’ll end up with a beautifully renovated home that will appeal to a large range of buyers.

Related

Originally published April 25, 2016.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.