Friday, August 30, 2019

Hurricane Dorian Heading for Florida—and President Trump’s Properties

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

$125M Oceanfront Compound in Malibu Reportedly Finds a Buyer

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

No Debate! The Obamas’ Martha’s Vineyard Estate Is This Week’s Most Popular Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, August 29, 2019

$40.5M Mansion With Sumptuous Views in S.F. Is Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

8 Ways to Incorporate Your Passions Into Your Home Decor

Your home reflects who you are, and you're way more than a selection of tasteful paint and furniture. Why not celebrate your passions by incorporating them into your decorating? When your talents, skills, and hobbies are on display as a natural part of your decor, you feel more inspired and more at home.

You don't have to remake your life to incorporate your passions into your home decorating. In many cases, just a small change of storage or placement will make all the difference - and you may even save money because you're using items you already own.

If something makes you happy, bring it out and let it shine.

Store your tools in arm's reach

Many creative hobbies come with beautiful tools. Don't hide your paintbrushes or yarn - show them off with pride of place!

Make sure to put tools you use frequently in accessible places where you can grab them. Nothing's worse than being inspired to create and having to wrestle a guitar off the wall or extract a crochet hook from the back of a cabinet. A good rule is to keep anything you use once a week or more within easy reach.

Display seasonal equipment year-round

Just because you can only ski a few months out of the year doesn't mean you forget about hitting the slopes. Keep your seasonal passions alive by keeping them in sight, but out of the way.

Mount skis or fishing poles over a door in the off season. If you have space above kitchen cabinets, that's a great place for the gorgeous fondue set you only use in winter. You could even ceiling-mount a canoe paddle - or the whole canoe if there's room. The good thing about most seasonal equipment is that you use it outside, so you don't have to worry too much about interim storage.

Put your talents to work

Give your creative passions room to shine in everyday life. If you're great at calligraphy, write a stylish meal-planning list for your week or create a framed school checklist to put by the front door.

Woodworkers can make anything from cutting boards to furniture. If you embroider, make your own cushion covers and embellished hand towels. Potters, once you fill your mug cupboard, branch out into making planters and wall hooks.

For almost any art or craft, there's a practical application, so make it a fun challenge to find yours.

Bring the mass-appeal objects into the conversation

When you have an interest in common with someone, the conversation just flows. That's why it's great to have some pop-culture touchpoints in your living space. Items like framed vinyl albums give your guests an easy way to learn about your interests and start talking.

Not everyone will be able to contribute to a discussion about your 19th-century Japanese chisel, but almost everyone who sees your framed program will remember the first time they heard about "Hamilton.”

For a living room where you entertain friends, or a home office where you have clients, these objects can help create connections.

Let your collection tell a story

When you're a collector, every piece has a story. As a whole, the items in a collection tell a narrative of their own history and how they came into your life.

Keep collections in a place of honor where the whole story can come together. Cabinets and display shelves are great for 3D objects like glassware, figurines and curios, and albums are perfect for stamps, old photos and ephemera.

Active items inspire action

If you need a little motivation to practice your passion, let your decor help inspire action. Match each inspiring object with the place you're most likely to need a boost.

If you aren't feeling your usual gourmet self, display your antique bakeware in your kitchen. To help with writer's block, display your diploma, your first pitch acceptance letter or special first editions of your favorite books over your desk. Hang athletic medals and photos of you at the finish line over the shoe bin near your entryway to encourage you to go for a run.

Match the vibe of the room

In general, keep the purpose of the room in mind when deciding where to display your prized possessions. Don't just go by where you have available wall space; take time to find the right fit.

A shelf of antique clown toys can look great in an office or playroom, but might not feel restful in your bedroom. And your championship soccer cleats or a signed football may be perfect inspiration in your workout room, but they're less than appetizing hanging in the dining room.

Mellow treasures set the mood

Some of your possessions are just for you, and they spark special memories and feelings when you see or touch them. If you have an object that brings your comfort, place it according to how it makes you feel. Does that beach rock make you feel calm? Keep it by your bedside.

If your grandpa's old pipe reminds you of how he taught you to read, keep in in a display case on a bookshelf or by your desk.

These are just a few of the ways you can bring your passions into your home decorating. Hopefully these ideas inspire you to bring your most important possessions into your decor, so you can keep those passions alive in your daily life.

Related:

- 7 Ideas for Personalized Home Accents That Are All About You

- Quiz: What Style Is Your Dream Bedroom?

- Get Hygge: Cozy Up to Scandinavian Simplicity

Originally published April 2018.

via 8 Ways to Incorporate Your Passions Into Your Home Decor

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Quiz: What Style Is Your Dream Bedroom?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

7 Retro Trends Making a Comeback

Each year, fashion leaves a strong impression on the design industry and its offerings for the season. For 2020, the vibe includes handmade organic details paired with the sparkle of the ’70s disco club and the velvety softness of the ’80s.

But beyond the nostalgic hints that those artistic impressions carry, what lies ahead for interiors? How will we change and evolve in our home environment? Read on and see what speaks to your design style as we approach another new year.

Cork and recycled elements

Many manufacturers, designers and architects have focused their products and projects on a sustainable, environmentally friendly approach to home building and design. Thanks to modern technology, sustainable products don't mean inferior quality, comfort or design.

In fact, these products celebrate eco-chic versions of modern or traditional designs in both elevated and affordable versions. While products like linoleum or cork flooring may have been long forgotten, they will see a strong comeback in the new season, thanks to its natural characteristics.

Abloom with florals

The traditional beauty of floral patterns, either abstracted or straight-up chintz, will continue to be the pattern to use, especially when paired with deep luxurious velvets and maximalist styled spaces. But home designer, beware: Chintz can be tricky. Its bold old-fashioned prints can easily turn to frilly English bed-and-breakfast if you’re not careful. When done right, the floral theme can add color, texture and just the right touch of classic elegance to your interior.

Handmade accents

Handmade items made with sustainable materials like jute, rice paper and clay will be all the rage in 2020. These elements go far in grounding a home, allowing its inhabitants to be in touch with the earth and their roots. The incorporation of natural materials popular years ago - like caning, rope, sea grass and bamboo - has a strong influence over modern furniture silhouettes and decor details. Elaborately embossed wall coverings, including gold rivets and metallic accents, give surfaces a beautiful tactile sensation and modern ambiance.

Plastic and acrylic

Increasing social consciousness around climate change has influenced the design industry to produce products accordingly. Plastics are being used for indoor and outdoor furniture frames, while water bottles are being used to create outdoor rugs and accents.

For a more luxe look, acrylic products are having a comeback, giving a room the architectural structure it needs without taking up visual real estate. Acrylic in a small space, like an entryway or sitting area, provides a surface that can be layered with more organic items and not feel fussy.

Authentic construction

The rise of digitally printed fabrics has created a true appreciation for real embroidery, thick wool boucles, linens and other artisan-inspired elements. Rich textural expressions are the theme of the upcoming season. Think velvet upholstery, hemp drapery, cork walls, wicker and jute for furniture and finishes.

Maximal artwork

The surge of minimalism and Scandinavian design, characterized by neutral colors and simple materials, is finally declining. In its place, bright colors and graphic patterns are becoming more prevalent in the home.

Don't be afraid to mix colors, patterns and textures. Take a gallery wall to the next level by having it cover an entire wall, or add a dramatic large-scale piece to your space. In this case, more is more.

Metallic accents

And speaking of timeless metal accents, sparkle is still on the design scene for living room decor compositions. Add a hint of disco glamour and luxury by introducing bronze, gold and chrome details through decorative accents, furniture inlays, hardware, lighting, mirrors and accessories.

Related:

- Creative Ways to Add Color to Your Rental

- 3 Design Tricks That Will Make Your Small Space Feel Big

- A DIY for the Books: How to Get Custom Built-In Shelves on a Budget

via 7 Retro Trends Making a Comeback

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Mortgage Rates Increase Slightly, Pumping the Brakes on the Refinance Boom

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

As Interest Rates Plummet, Should You Refinance Right Now?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, August 28, 2019

Mortgage Rates Split with Treasurys, Stay Flat This Week

Mortgage rates barely budged this week, straying from their typical pattern of moving with bond yields. A shortage of blockbuster trade-related headlines and economic data releases kept Treasury yields within a fairly narrow range over the last seven days, mostly moving on data emerging from Europe. Mortgage rates stayed even tighter, holding near their lowest levels in three years.

The typically steadfast relationship between the two has weakened in recent weeks, as low rates and increased refinancing activity have sapped investor demand for mortgages. As a result, rates haven't dropped as far as the recent fall in Treasury yields would normally indicate. Market volatility is contributing to this changing relationship:

When markets start to stabilize, the link between yields and mortgage rates will return. Looking ahead, markets will be attuned to Federal Reserve Chair Jerome Powell's statements from the Jackson Hole symposium on Friday, and Tuesday's release of consumer confidence data will offer hard evidence of how trade-related headlines are affecting consumers' economic outlook.

The post Mortgage Rates Split with Treasurys, Stay Flat This Week appeared first on Zillow Research.

via Mortgage Rates Split with Treasurys, Stay Flat This Week

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, August 27, 2019

Listing Photos of Dallas Mansion With ‘Wall of Death’ Create a Stir Again

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wine Country towns you can actually afford

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

June Case-Shiller Results and July Forecast: Phoenix Posts Largest YoY Gains

- U.S. home prices rose 3.1% in June from a year earlier.

- Phoenix replaced Las Vegas as the city with the largest year-over-year gains.

- Six cities in Case-Shiller’s 20-city composite reported higher price increases for the year ended June 2019 than the year ended May 2019.

Annual home price gains continued their gradual slowdown in June, although the pace of those declines has slowed from earlier this year. While prices are still climbing, the rate of annual appreciation appears to have leveled off near its long-term average, after consistently falling from a high point reached in the spring of last year.

Phoenix, Las Vegas and Tampa posted the largest year-over-year gains in Case-Shiller’s 20-city composite with increases of 5.8%, 5.5% and 4.7%, respectively.

Housing demand remains strong as buyers are encouraged by rising wages and by mortgage rates that just keep falling amid growing economic uncertainty. Would-be buyers stand with pre-approved mortgages in hand. However, they've become unwilling to pay escalating prices for the relatively low inventory of homes that are on the market and instead are making sellers wait and even drop list prices.

| Index | Zillow Forecast, Released 7/30/19 | Actual Case-Shiller Indices, Released 8/27/19 |

Historical Median Absolute Error* |

|---|---|---|---|

| 10-City Composite, Month-Over-Month (SA) |

-0.1% | 0.0% | 0.2% |

| 10-City Composite, Year-Over-Year (NSA) |

2.0% | 1.8% | 0.2% |

| 20-City Composite, Month-Over-Month (SA) |

0.0% | 0.0% | 0.2% |

| 20-City Composite, Year-Over-Year (NSA) |

2.2% | 2.1% | 0.1% |

| U.S. National Month-Over-Month (SA) |

0.2% | 0.2% | 0.1% |

| U.S. National Year-Over-Year (NSA) |

3.4% | 3.1% | 0.1% |

| *Calculation of Median Absolute Errors are based on Zillow’s monthly Case-Shiller forecasts. Zillow’s Case-Shiller 10- and 20-City Index forecasts date to 2011. The national Case-Shiller forecasts began in 2014. | |||

Recent increases in sales volume suggest that the housing market has some fight left. As long as signs of growing economic uncertainty do not dissuade people from entering the market, this slower pace of home price appreciation should hold steady as we enter the second half of 2019.

| Index | Actual June Case-Shiller Change |

Zillow’s July Case-Shiller Forecast |

|---|---|---|

| 10-City Composite, Month-Over-Month (SA) |

0.0% | -0.2% |

| 10-City Composite, Year-Over-Year (NSA) |

1.8% | 1.6% |

| 20-City Composite, Month-Over-Month (SA) |

0.0% | -0.2% |

| 20-City Composite, Year-Over-Year (NSA) |

2.1% | 1.9% |

| U.S. National Month-Over-Month (SA) |

0.2% | 0.1% |

| U.S. National Year-Over-Year (NSA) |

3.1% | 2.9% |

| *Calculation of Median Absolute Errors are based on Zillow’s monthly Case-Shiller forecasts. Zillow’s Case-Shiller 10- and 20-City Index forecasts date to 2011. The national Case-Shiller forecasts began in 2014. | ||

The post June Case-Shiller Results and July Forecast: Phoenix Posts Largest YoY Gains appeared first on Zillow Research.

via June Case-Shiller Results and July Forecast: Phoenix Posts Largest YoY Gains

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Home-Price Growth Continued to Slow in June

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Starting Salaries for Teachers Don't Pay the Rent

It's back to school time, and for many teachers that means a return to their regular jobs from the ones they work in the summers to supplement their incomes and help them — literally — pay the rent.

Rent is particularly burdensome for teachers early in their careers: At the national level, the median market-rate rent takes a staggering 46.8% of a starting teacher's salary. That improves to 35.6% for mid-career teachers and to 26.6% for the highest paid teachers — the last group finally falling below the 30% generally accepted threshold that deems housing costs to be affordable.

In 19 of the country's largest 50 metro areas, starting-level teachers would pay more than half their salaries on the market rent.

The situation is generally better for teachers that can buy a home instead of rent one, thanks to the benefit of low mortgage interest rates and decades-long mortgage terms that help keep monthly payments very low, even as housing prices rise. Starting-level teachers pay 26.6% of their salaries on the median U.S. mortgage. Affordability improves for mid-career teachers to 20.2% and for the highest paid teachers to 15.1%.

In some of the country's priciest markets, many teachers literally cannot put together a housing payment on their salaries alone — either to rent or own. The median rent in San Jose. Calif., consumes 108.3% of a typical starting teacher's salary. A mortgage on the median home in that metro area takes even more: 129%.

And it's not just expensive coastal markets that devour teachers' incomes. Only one of the country's largest 50 metro areas — Pittsburgh — requires less than 30% of a starting teacher's salary, and it's close, at 29.5%.

Methodology

Zillow analyzed salary and income data for a selection of full-time working public preschool, kindergarten, elementary school, middle school, high school and special education teacher categories from the U.S. Census Bureau, American Community Survey, 2017 microdata, made available by IPUMS USA, University of Minnesota, www.ipums.org.

We divided the observations into cohorts, considering the 25th, 50th and 75th percentile monthly gross incomes for individual teachers and, separately, households that include at least one teacher. To calculate the typical monthly mortgage payment, we first gathered mortgage rate information from Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US. Then using the most recent available rate (August 1st, 2019), we calculated the typical mortgage payment for the median-valued home in a metropolitan area using the metro-level Zillow Home Value Index (ZHVI) for June 2019. Finally, we considered what portion of each cohort's salary goes toward this monthly mortgage payment.

The post Starting Salaries for Teachers Don't Pay the Rent appeared first on Zillow Research.

via Starting Salaries for Teachers Don't Pay the Rent

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

You Look Like a Million Bucks: 9 Homes for Sale for Exactly $1 Million

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, August 26, 2019

10 Best Labor Day Deals for Your Home That Are Up for Grabs Right Now

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, August 23, 2019

Brace Yourself: How the Coming Recession Will Impact The Housing Market

It seems that whenever you pick up a newspaper or turn on the news these days, a scary word hits you in the face: recession. Germany is already teetering on the brink of recession; an unruly exit from the European Union this fall could cause one in Britain; and in the U.S., the Federal Reserve chairman warned of the risks of an escalating trade war with China.

But although the R-word may be a trigger for those who remember—or even experienced—the mass layoffs, scores of foreclosures, and plummeting home prices of the last downtown, folks shouldn’t panic just yet. And they shouldn’t expect another real estate fire sale.

“This is going to be a much shorter recession than the last one,” predicts realtor.com® Senior Economist George Ratiu. “I don’t think the next recession will be a repeat of 2008. … The housing market is in a better position.”

Federal Reserve Chairman Jerome Powell indicated on Friday that last month’s interest-rate cut would be followed by another in September, but that that might not be enough to counter the trade tensions, which ratcheted up on Friday when China declared it would impose tariffs on $75 billion in U.S. products to retaliate against similar U.S. tariffs. President Donald Trump reacted by raising the tariff rate on existing and planned tariffs even further.

About 2% of economists, strategists, academics, and policy-makers believe a recession will start this year, according to a recent survey of more than 200 members of the National Association for Business Economics. Another 38% believe one will begin in 2020, while 25% anticipate one starting in 2021. Fourteen percent expect it won’t materialize until after 2021.

However, Trump, who had been exploring tax cuts to give the economy a boost but changed his mind, remains confident that there’s no risk of a recession at all. He’s been putting put out a series of positive tweets about the economy for the last week or so.

He responded to China’s announcement on Friday by tweeting, “Our Economy, because of our gains in the last 2 1/2 years, is MUCH larger than that of China. We will keep it that way!”

For sure, unemployment is hovering around the lowest it’s been in the last 50 years. (However, it turns out there weren’t as many jobs in 2018 and early 2019 as previously reported.) Wages are growing, and we’ve entered the longest economic expansion in U.S. history. But a downturn within the next two years still looks likely—particularly if a trade war heats up, making it more expensive to import goods. Those increased costs are likely to be passed along to everyday consumers.

The housing market’s risky mortgages and rampant speculation were blamed for plunging the world into a financial crisis the last time around. But these days real estate isn’t likely to be the cause of a recession.

Will home prices and sales plummet in a recession?

Aspiring buyers hoping that home prices will crash, like they did during the Great Recession, are likely in for a rude awakening. There simply aren’t enough homes being built to satisfy the hordes of buyers. And with more members of the giant millennial generation wanting single-family homes in which to raise their growing families, there isn’t likely to be a drop-off in demand anytime soon.

But the anticipation of a recession in itself could make the housing shortage even worse. Worried, would-be sellers may decide to postpone listing until they can get top dollar for their properties.

Yet although a lack of homes for sale typically drives up prices, that effect could be mitigated if there are fewer folks who can afford to buy. In a recession, it could become harder to find a good-paying job or steady freelance work. Even those who remain gainfully employed may worry about their job stability.

“If we do go into a recession, there will be layoffs,” says Ali Wolf, director economic research at Meyers Research, a national real estate consultancy. “If you move from a two-income household to a one-income household, it doesn’t change the desire to own. But it does impact the ability.”

Realtor.com’s Ratiu believes prices will flatten, but likely not fall. Meanwhile, the number of home sales will also remain flat or potentially even dip, he believes.

Other economists expect the recession to take a bigger toll on housing.

“With people having PTSD from the last time, they’re still afraid of buying at the wrong time,” Wolf says. “But prices aren’t likely to fall 50% like they did last time.”

“We do expect prices will fall marginally,” says Wolf. The priciest parts of the country, which saw the biggest price hikes, could see the biggest price corrections. Sales could decline anywhere from 10% to 20%, she predicts.

The luxury market is already seeing price decreases. These high-end homes, usually in the $1 million and up range, are usually considered a bellwether for the greater housing market.

A big wild card in all of this is mortgage interest rates, which were at a super-low 3.55% for a 30-year fixed-rate loan as of Thursday, according to Freddie Mac data. If they continue to fall, it could give the housing market a boost. That’s because low rates translate into lower monthly mortgage payments.

Could rentals become cheaper?

Those hoping for rental prices to be slashed will probably be disappointed as well.

“We expect a little bit of an impact,” says Greg Willett, chief economist at RealPage, a property management technology and analytics company for apartment buildings. “But it’s not doom and gloom.”

He expects apartment price hikes to slow from 3% annually to more minor 1.5% or 2% price increases over the next few years. The rental market is likely to be buffered by those nervous about making what could be the largest purchase of their lives, a home, in uncertain economic times. Those folks may decide to live in a rental until the economy is booming again.

The exception, again, is the luxury rental market. Developers may have to offer concessions, like a free month’s rent, or lower prices a little to attract wealthier tenants. But that isn’t likely to trickle down to the middle or even lower end of the rental market.

Will builders stop putting up badly needed new homes?

A recession could make builders even more reluctant to break ground on new residences, particularly in the priciest markets on the coasts.

A year ago, about 10% of single-family home builders offered buyers incentives, such as discounts, to go under contract, says National Association of Home Builders Chief Economist Robert Dietz. Today, about 40% are turning to incentives to spur home sales. That’s not a good sign.

Tariffs on building materials, such as steel, are already making construction more expensive. And the construction worker shortage is severely limiting the number of homes that can be built. A downturn could make this worse.

“You’ll some local markets when home construction decline,” says Dietz. “Some prospective home buyers could be concerned about making that purchase.”

Will a recession spur another foreclosure crisis?

One of the hallmarks of the Great Recession were the blocks littered with foreclosed properties. Some sold quickly to intrepid young families or investors. However, those with boarded-up windows and overgrown yards blighted many a neighborhood. And losing a home was a devastating blow to many owners.

But foreclosures aren’t expected to be such a problem if a downturn occurs. Lending laws were tightened in the wake of the housing bubble bursting. So now only the most qualified borrowers can secure a mortgage.

“This time we won’t have bad mortgages, just people who are losing jobs,” says Lawrence Yun, chief economist of the National Association of Realtors.

Plus, homeowners these days have a record amount of equity in their homes. That means if someone loses their job and is unable to make their monthly mortgage payments, they’re much more likely to put the property on the market instead of going into foreclosure. And with home prices expected to remain high, fewer folks will find themselves under water on their mortgage. That should make it easier to unload the residences if need be.

And more people own their homes outright today than they did just over a decade ago. About four in 10 homeowners don’t have a mortgage on their abode compared to three in 10 when the last recession occurred, according to Ratiu.

“Foreclosures will definitely increase, but only because [the number of] foreclosures are [already] at rock bottom,” says Andres Carbacho-Burgos, a senior economist at Moody’s Analytics focused on housing. He expects a recession will happen at the end of this year or early next year and only last two or three quarters.

In addition, Carbacho-Burgos expects home improvement spending to remain flat during the recession.

And home flipping, one of the factors contributing to the previous housing market bust, is expected to slow, he says. That’s because slower home price growth makes flipping less lucrative for investors.

The post Brace Yourself: How the Coming Recession Will Impact The Housing Market appeared first on Real Estate News & Insights | realtor.com®.

via Brace Yourself: How the Coming Recession Will Impact The Housing Market

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

New Home Sales (July): A Step Back, But Still on Pace for Best Year Since 2007

- July new home sales fell 12.8% from revised June figures to a seasonally adjusted 635,000 units, according to the Census Bureau and the Department of Housing and Urban Development. That’s 4.3% above July 2018.

- The median sales price of new homes sold in July was $312,800, up 2.2% from June and down 4.5% from a year earlier.

- The seasonally-adjusted estimate of new houses for sale at the end of July was 337,000, up 1.2% from June.

July’s new home figures will be read as a disappointment, as both the number of sales and change from the month before fell well short of expectations. But it's important to keep things in context. Today's figures are on a host of monthly revisions that together indicate a robust trend.

Sales are now up 4% year-to-date, with 2019 on pace to be the best year for new home sales since 2007. With inventory and mortgage rates low, there's still plenty of runway for builders to add new homes to a market that's hungry for housing stock. Homebuilder sentiment remains strong despite persistent headwinds in the form of expensive labor, a shortage of land and growing signs that a recession could be on the horizon.

The post New Home Sales (July): A Step Back, But Still on Pace for Best Year Since 2007 appeared first on Zillow Research.

via New Home Sales (July): A Step Back, But Still on Pace for Best Year Since 2007

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Dirty Secret About Most ‘Fixer Uppers’

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Frank Lloyd Wright’s Cedar Lake House Is This Week’s Most Popular Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, August 22, 2019

$43.9M Mansion Featured on ‘Selling Sunset’ Is the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Taxpayer Alert! U.S. Government Buys $16M Penthouse at 50 UN Plaza

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Living Room Design Fails So Bad, They’ll Scare the Living Daylights Out of You

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, August 21, 2019

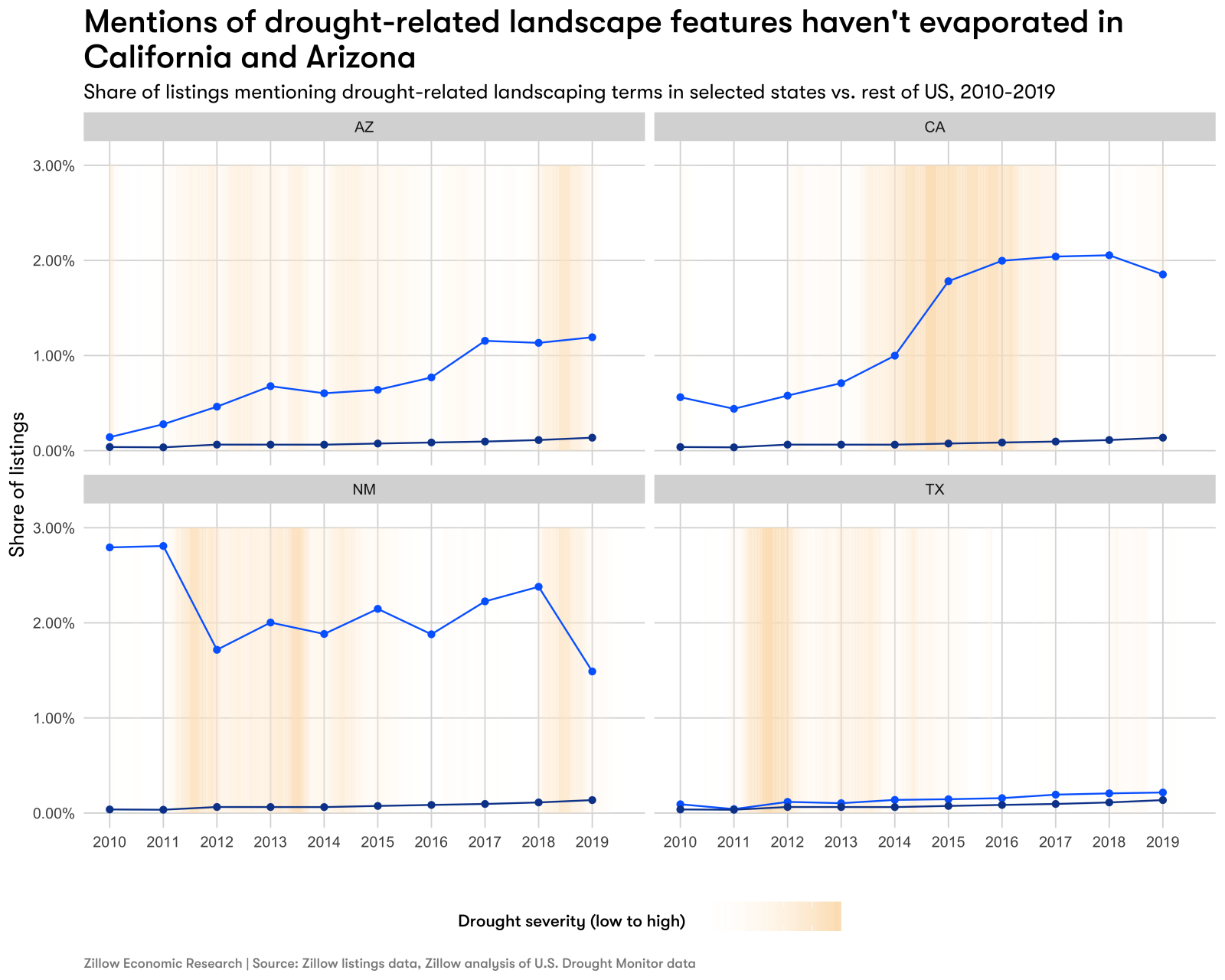

Drought-Resistant Terms Doubled in California, Arizona Listing Descriptions

- Mentions of drought-resistant features in home listing descriptions roughly doubled in California and Arizona during the recent drought, and have yet to return to pre-drought levels.

- Environmental norms could explain some of this trend: California's coastal markets have the highest share of listings that mention drought-tolerant features, even though the drought was no more severe there than in markets farther inland.

After the wettest 12 months in U.S. history, the threat of drought might seem like a mirage. But the frequency with which drought-resistant features are mentioned in home listings is still elevated in hard-hit western states, suggesting that these features remain desirable for home buyers even as drought pressures have eased.

What are drought-resistant landscaping features?

Around a quarter of water consumption among single-family residences goes to outdoor use, but in hotter, drier parts of the country, outdoor water usage can be twice that in wetter areas. In places that don't get much rain, maintaining a lush green lawn can suck up tens of thousands of gallons of water per year – a heavy environmental burden. In fact, some researchers argue that lowering outdoor water use has the greatest potential for urban water savings.

Instead of conventional grass lawns, the U.S. Environmental Protection Agency (EPA) recommends choosing native plants that require water only from normal rainfall, using mulch to help aid water retention, and installing water-efficient drip irrigation systems. Alternatively, homeowners can replace their lawns with artificial turf, saving on yard maintenance costs as well as water use.

Under normal circumstances, maintaining a conventional lawn might not seem expensive, especially when compared with the upfront cost of converting to more water-efficient landscaping. But when state and local governments impose conservation measures or offer incentives to help save water during droughts, that financial calculus can change. What's more, social pressure to conserve water also can motivate people to make the switch – after all, most people don't want their neighbors to think they're irresponsible water-guzzlers.

It's not hard to imagine that both these forces would be temporary, with interest waning once normal rainfall returns. However, an analysis of home listing descriptions tells a different story.

Drought-related terms are still popular in California and Arizona, but they never took off in Texas

California and Arizona both saw an uptick in mentions of drought-resistant features[1] during or after periods of intense drought. Since the end of the California drought, that spike tapered somewhat but has remained elevated.

Meanwhile, New Mexico and Texas – both of which experienced drought in 2009 and early 2010 – show disparate trends. Mentions of drought-resistant features in New Mexico were consistently high over the last decade, but have dropped recently, while listings mentioning these features in Texas remained few and far between.

Of course, the share of listings that mention these features probably doesn't reflect their actual prevalence across different geographic areas, because their presence is less likely to be notable in drier climates. But an increase in mentions over time could signal that they are becoming more common, or at least more in-demand.

Different vocabulary in different states

Listings in different states use somewhat different terms in reference to these features, perhaps providing a clue to whether environmental motivations are at play. The phrases "drought friendly," "drought tolerant," and "drought resilient" are most common in California, whereas the term "hardscape" has much wider geographic reach, with mentions appearing in along the East Coast states and in the Southwest. Meanwhile, the technical term "xeriscape" crops up in New Mexico and Colorado. And in Georgia, which also experienced a drought in the last decade, mentions of drought are often in reference to lakes that are deep enough that homeowners can continue to use their docks during dry spells.

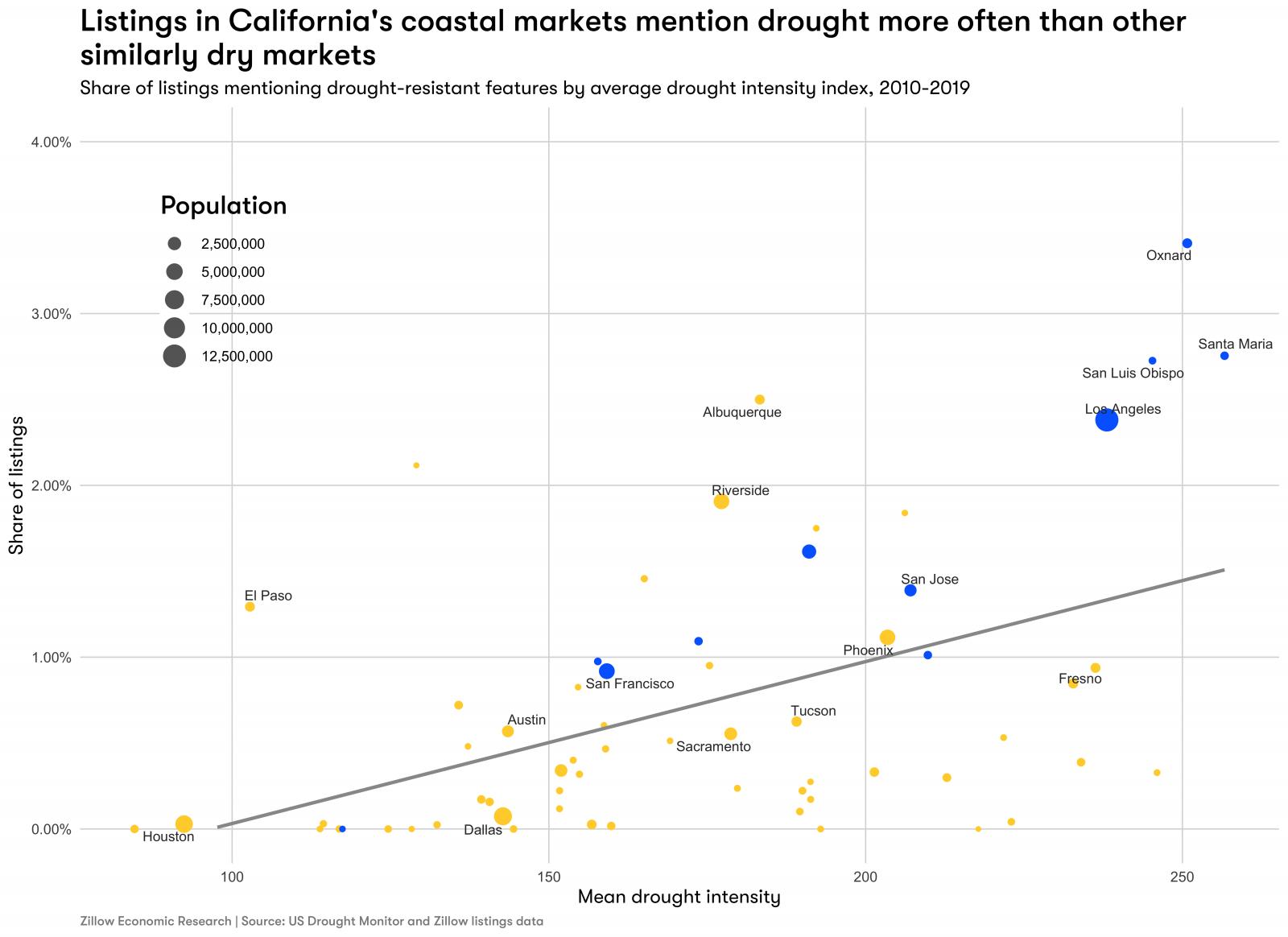

Environmental values might play a role

California's coastal markets have the highest share of listings that mention drought-tolerant features, even though the most recent drought was no more severe there than in markets farther inland. For example, Los Angeles experienced roughly the same average drought intensity as Fresno, but its listings mention drought about twice as often. This geographic pattern could reflect a stronger culture of environmentalism along the coast. And greater environmental awareness might also help explain why mentions of drought-resistant features have remained high even after the drought.

Data from the California State Water Board show that the state's coastal regions also have had lower residential water use per capita than its inland regions, although it's worth noting that per-person water use inland dropped by much more during the drought.

While drought concerns are sporadic right now, recent research indicates that climate change will make rainfall less frequent (but more extreme when it does happen) in California and other West Coast states. In combination with rising temperatures, which tend to increase landscaping-related water needs, this greater variability could make investing in more sustainable landscaping now a smart financial move as well as an environmentally friendly one.

[1] The list of terms includes the following words or phrases: drought tolerant, drought resistant, drought resilient, drought friendly, drought proof, xeriscape, hardscape, gravel landscaping, gravel beds, tan bark, desert garden, desert plants, artificial turf, artificial lawn, and artificial grass. This list was generated from common terms referenced in guides to improving landscaping's water efficiency, and also used regular expressions to account for slight variations on the exact term.

The post Drought-Resistant Terms Doubled in California, Arizona Listing Descriptions appeared first on Zillow Research.

via Drought-Resistant Terms Doubled in California, Arizona Listing Descriptions

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The ‘Fixer Upper’ Curse: Why Chip and Joanna Gaines Homes Can Be Hard to Sell

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

July Existing Home Sales: Far From Stellar

- Existing home sales rose 2.5% from June to a seasonally adjusted annual rate of 5.42 million in July and were up 0.6% from a year ago, according to the National Association of Realtors.

- The median price for existing homes was $280,800, up 4.3% from a year earlier ($269,300).

- Inventory fell 1.6% from June to 1.89 million homes for sale in July. That’s also a 1.6% decrease from a year ago.

Despite today’s win, sales are falling short of the stellar performance you’d expect from a market with enticing mortgage rates and strong employment. Sales have been sluggish for a while now despite favorable conditions. Buyers are letting listings languish rather than diving into a market whose offerings — or price points — don't suit them. Although the busy spring shopping season has now come and gone, there are still signs of momentum. Recent boosts in mortgage applications and listings suggest that the housing market has some fight left.

The post July Existing Home Sales: Far From Stellar appeared first on Zillow Research.

via July Existing Home Sales: Far From Stellar

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Magnetic Metros: The Top 10 Places Luring Out-of-Towners to Move In

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, August 20, 2019

Forecasts for Existing and New Home Sales (July 2019)

- Zillow expects July existing home sales to rise 1.9% from June to 5.37 million units at a seasonally adjusted annual rate (SAAR). That would represent a 0.4% decrease from July 2018.

- We estimate new home sales will climb 0.2% to 647,000 units (SAAR).

Mortgage rates have fallen dramatically over the last nine months, almost to three-year lows, but so far have not been followed by an uptick in existing home sales. With the busy spring shopping season come and gone, it's unlikely that we'll see a sharp increase in sales volume. However, there are signs of mounting sales momentum. Inventory levels have started to grow, driven largely by an influx of new listings on the market. Mortgage rates have been low for months now, but recent declines appear to have (finally) incented people to enter the market, and for-purchase mortgage applications have risen steadily. It's not the steep increase that some experts had hoped for, but July's sales figures may well show that the housing market still has some fight left.

For now, it's steady as she goes for sales of new home sales, which have been buoyed by low mortgage rates but hindered by low construction. And as always, look to the revisions: Despite a positive headline figure, June's new home sales – up 7% from May – came on heavy downward revisions to May's figures. New home sale counts are still ahead of where they were last year, but volume failed to build on the positive momentum generated in the winter. Home construction levels continue to languish, although encouraging building permits, strong home completions trends and steady builder confidence, suggest that activity may pick up in coming months.

The post Forecasts for Existing and New Home Sales (July 2019) appeared first on Zillow Research.

via Forecasts for Existing and New Home Sales (July 2019)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

This Is How Cool You Should Keep Your House—Spoiler: Not Very

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Ugly Truth About Amazon’s Gorgeous $100K House

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Measuring Up: What a 2,500-Square-Foot House Costs Around the Country

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, August 19, 2019

8 Best Back-to-School Organization Ideas That Are Unbelievable Bargains, Too

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

How Much Would It Cost to Buy Greenland—and How Would You Calculate That Price?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Burner Boom: As Reno Reinvents Itself, It Looks to Burning Man

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, August 16, 2019

7 Scarily Organized Refrigerators That’ll Make You Worry What This World Has Come To

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

July Housing Starts: Still Languishing

- Housing starts in July dropped 4% from June to a seasonally adjusted annual rate of 1.19 million, according to the U.S. Census Bureau and the U.S. Department of Housing and Urban Development. That’s 0.6% above July 2018. Single‐family housing starts in July climbed 1.3% from June to 876,000 (SAAR), a 1.9% boost from a year earlier.

- Building permits in July rose 8.4% from June to 1.34 million (SAAR). That’s 1.5% above July 2018.

- Housing completions in July were up 7.2% from June to 1.25 million (SAAR), which was 6.3% higher than a year earlier.

This monthly decline isn’t the first indication that the housing market is flagging. Construction has languished all year — with starts down 3.6% for the first seven months of the year compared to a year earlier.

Scarce land and high labor costs have plagued builders for much of the year, factors that have been exacerbated by unrelenting uncertainty in the global markets. This week's flare-up, with bond markets flashing recession warnings, does not provide fertile ground for new housing investment.

Consumers stand ready to snap up new homes, particularly at the entry level, and mortgage rates are cooperating — but new construction is not. That could change, given the lift in July housing permits, which was higher than expected.

The post July Housing Starts: Still Languishing appeared first on Zillow Research.

via July Housing Starts: Still Languishing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Millions Check Out Tom Brady’s Mansion—It’s the Week’s Most Popular Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Home Value Growth Continues Steady Normalization as Inventory Creeps Up (July 2019 Market Report)

- The rate of year-over-year home value growth has fallen in each of the past seven months. The median U.S. home is worth $229,000, up 5.2% from this time last year.

- Rents grew 1.9% on an annual basis. The median monthly rent in the U.S. is $1,592.

- For-sale inventory grew 1.3% year-over-year, and new listings are up 5.7% from a year ago.

The annual pace of U.S. home value growth slowed for the seventh straight month in July as the market continues to normalize and slowly find more balance between home buyers and sellers after years of seller control.

The typical U.S. home was worth $229,000 in July, up 5.2% from a year ago – the slowest annual appreciation recorded in any month since October 2015. In the same month last year, home values rose 7.7% year-over-year. Despite the slowdown, home values are still showing healthy growth after a brief stall earlier in the year. Monthly home value growth flatlined in both April and May, but bounced back to 0.3% in both June and July – exactly in line with long-term monthly averages.

Among the 50 largest U.S. markets, home values grew the most last month in Salt Lake City (up 9.4% since July 2018), Indianapolis (up 8.1%) and Charlotte (up 7.3%), though growth in all three is slower than a year ago – a trend echoed in a majority of large metros nationwide. Annual growth in July was slower than a year ago in 47 of the nation's 50 largest markets. The three large markets in which home value growth has accelerated (New Orleans, Birmingham and Oklahoma City) are notable for their relative affordability – the median home value in all three is well below the national median. Markets in which home value growth has slowed the most include pricey west coast markets and a couple of traditionally more-affordable markets: San Jose, San Francisco, Las Vegas, Seattle and Dallas.

In the once red-hot and still ultra-pricey Bay Area, home values aren't just growing more slowly, but have actually fallen – the value of the typical home fell 10.5% last month in San Jose and 1.1% in San Francisco compared to July 2018. For reference, at the same time last year home values grew 24% annually in San Jose, a 34.5 percentage point difference.

Ultimately, this ongoing slowdown is a good sign that the market is adjusting in response to the growing difficulty of saving for a down payment as prices rise. And for those with adequate savings, low mortgage rates are helping keep them interested in homeownership, despite the potential for softer appreciation in their investment during the first few years of ownership.

A 'Good & True' Increase in Supply

There were 1,575,892 U.S. homes listed for sale in July (seasonally adjusted), up 1.3% from a year ago. This modest annual increase breaks a stretch of four consecutive months in which inventory fell year-over-year. Inventory was also up year-over-year in 30 of the nation's 50 largest markets. For-sale inventory grew the most from a year ago in Las Vegas (up 53.5% year-over-year), San Jose (32.6%) and Denver (26.9%).

Unlike prior months, recent inventory gains look to be driven largely by growth in newly listed homes – and not necessarily homes lingering longer on the market. Sellers put more than 385,000 homes on the market in July, up 5.7 percent from a year ago and the first annual gain of the year. At the same time, the number of days a home spent on the market before selling remained steady in June (the latest month for which data was available) at 66 days, the same as in May and just one day more than June 2018.

This uptick in the rate of homes coming onto the market – for the first time in a while, a good and true increase in supply – should be a balm to inventory-starved home buyers still on the market as the home shopping season turns from spring to summer.

Rent Growth Stabilizing

After a period of breakneck annual growth in the 6% and 7% range as recently as 2015, annual rent growth has stabilized around 2%. The median U.S. rent grew 1.9 percent year-over-year in July, to a Zillow Rent Index of $1,592/month.[1] On a monthly basis, the median U.S. rent grew 0.5% from June (up $8/month from $1,584). Rent was up year-over-year in 47 of the nation's 50 largest markets.

For the eighth consecutive month, rents rose the most in Phoenix (up 6.1% from a year ago), followed by Las Vegas (up 5.9%). Rents fell in only three of the 50 largest markets – Houston, Buffalo and Baltimore.

[1] Beginning with publication of July data, we have adopted a revised methodology for calculating the Zillow Rent Index. These changes were made to better reflect the stock of homes that actually rent in a given month, and will offer more visibility into smaller changes in the rental market going forward. We invite you to take a deeper look into our new methodology here.

The post Home Value Growth Continues Steady Normalization as Inventory Creeps Up (July 2019 Market Report) appeared first on Zillow Research.

via Home Value Growth Continues Steady Normalization as Inventory Creeps Up (July 2019 Market Report)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Methodology: Zillow Rent Index (2019 Update)

Note: The Zillow Rent Index initially debuted in early 2012. Beginning with publication of July 2019 data, the methodology was updated to better reflect the true rental stock and to capture small market changes. For comparison’s sake, our original methodology can be found here.

The Zillow Rent Index (ZRI) is a dollar-valued index intended to capture typical market rent for a given segment (IE, multifamily or single-family units) and/or geography (IE for a given ZIP code, city, county, state or metro) by leveraging Rent Zestimates.

Historically, the ZRI was essentially calculated as the median Rent Zestimate of that segment. Recently, we revisited and updated this methodology to both better account for the stock of homes that actually rent and to capture small but important changes in rent levels.

These changes, summarized below, have been incorporated into a new Zillow Rent Index methodology that will apply to all published ZRI data series going forward. The largest changes include:

- Reweighting to better reflect the rental housing stock

- Taking the mean of the middle quintile instead of a median

Individual Rent Zestimates are computed for all homes, whether or not those homes are currently or ever were available for rent. Indeed, many of the homes for which we compute Rent Zestimates, especially single-family homes, are neither for-rent nor renter-occupied. Because single-family homes are, on average, higher-valued than apartments, including all of them in the ZRI and computing a median based on that full universe of homes creates an upward bias in the index. With our recent adjustments, we now reweight subsegments by the Census Bureau's American Community Survey (ACS) counts of units of different housing types so the sample is representative on the dimension the survey captures, namely number of units in the building and decade the building was built.

We also re-worked our methodology to calculate ZRI as the mean of the middle quintile of included Rent Zestimates, rather than the median. Doing so better captures small changes in the market, while also reducing noise. Rents are unevenly distributed and cluster around round numbers just below changes in the leading digit: there are many listings at $900/mo, for example, but few at $1013/mo or $842/mo. This is reflected in the algorithm that computes individual Rent Zestimates, but is somewhat problematic when creating a median-based index.

Imagine a region with 10,000 rentals where the median rent value was $900/month. If 1,000 of those rentals had exactly $900 as the median rent, the distribution could change quite a bit before the median would change. Conversely, if the median is near the $900/$1000 boundary, with no rents in between, index figures thrash back and forth between $900 and $1000 even if there is little change in the distribution. Taking the mean of the middle quintile alleviates this problem. Why not just take the mean? Rent price distributions are very skewed, so the mean is heavily influenced by a small number of expensive properties, and therefore does a poor job capturing changes in 'typical' rents.

We believe these changes will better reflect both the actual level and predominant trends in the rental market, while also reducing noise. Because of re-weighting, the ZRI level in most regions has shifted down by about 10% compared to prior index calculations. Otherwise, the effects are heterogenous and mostly small.

Methodology

Property Universe

Every month, a Rent Zestimate is created for more than 100 million U.S. housing units for which Zillow has sufficient data. The sources of this data include public records (property taxes, transactions), real estate listings and user-generated data. Real estate listing data comes from local Multiple Listings Services and/or direct feeds to Zillow from real estate brokers. User-generated data includes rental listings and for-sale listings posted directly on Zillow, and user corrections to incorrect and/or out-of-date data from listings and public records. Properties enter and leave this 'universe' due to many reasons, the most important of which are discussed below.

As the Zillow rental business and our data sources expand, we may become aware of more individual units within a building and add them to our “rental universe.” Periodically, these are retroactively given Rent Zestimate histories using attributes of the unit and the Rent Zestimate model. We take advantage of these retroactive histories in the first calculation of the Zillow Rent Index using our updated methodology.

Index creation

To create the index, we consider every home within a given region for which we have a Rental Zestimate for that period, then reweight and aggregate those estimates.

Weights are derived from the most recent 5-year ACS counts of renter-occupied housing units by decade built and number of units in the building available at the reported date (ACS file B25127, “TENURE BY YEAR STRUCTURE BUILT BY UNITS IN STRUCTURE”). These counts are compared to the number of units for which we have Rent Zestimates in the same region. For instance, if ACS states that 30% of rented units in a given county are in 2-4 unit buildings, but only 15% of our rent zestimates in that county are for 2-4 unit homes, the weight for each of those rent zestimates is 2. For regions where ACS data does not exist, we use county-level weights.For regions that overlap multiple counties, we sum over all counties overlapping with that region to compute weights. Therefore the weights are subject to:

And:

![]()

Where w is the weight and r is the rent zestimate, with i ranging over properties in the region. Using the weights, we can now compute weighted n-tile cutoffs:

![]()

Where t1 and t2 are tier thresholds (for low tier: 0.15, 0.35; high: 0.65, 0.85; middle and all others: 0.4, 0.6). For properties with weights satisfying the above, we compute a mean:

Which is our unsmoothed index for a given region and date.

After the index is produced, an exponentially weighted moving average is applied to smooth the series. Finally, we use a set of heuristic rules based on statistics of the time series in order to identify time periods within each series that likely have low signal-to-noise. We do not publish those time periods, which may cover the entire time series.

Tiers

The middle tier is the same as the headline number (mean of rent zestimates between the 40th to 60th percentiles). The low tier is the mean of the rent zestimates falling between 15th to 35th percentiles within a given region and the high tier is the mean between the 65th and 85th percentiles.

Available Segments

Currently, we compute indices at multiple geographic region levels: National, State, Metro, County, City, Zip, and Neighborhood.

At each region level, we compute for several home types:

- Single-family

- Condo/CoOp

- Single-Family + Condo/CoOp (“all homes”)

- Multi-Family

- Single Family + Condo/CoOp + Multi-Family (“all homes plus multifamily”)

Additionally, for “all homes plus multifamily,” we compute tiers (“low,” “middle,” “high”) and cut by bedroom count.

The re-weighting procedure is only done for “all homes plus multifamily” and the multi-family series. Not all computed series are published, and all are subject to revision.

The post Methodology: Zillow Rent Index (2019 Update) appeared first on Zillow Research.

via Methodology: Zillow Rent Index (2019 Update)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, August 15, 2019

$100M Malibu Home Under Construction Is the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, August 14, 2019

A Sneak Peek at Chip and Joanna Gaines’ Fall Collection at Target—and 9 Items You’ll Fall For

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Most popular lakeside towns you can actually afford

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Secret Curse of Owning a Frank Lloyd Wright House

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, August 13, 2019

America’s ZIP Codes Are Becoming More Economically Segregated—Here’s How It’s Already Hurting the Middle Class

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

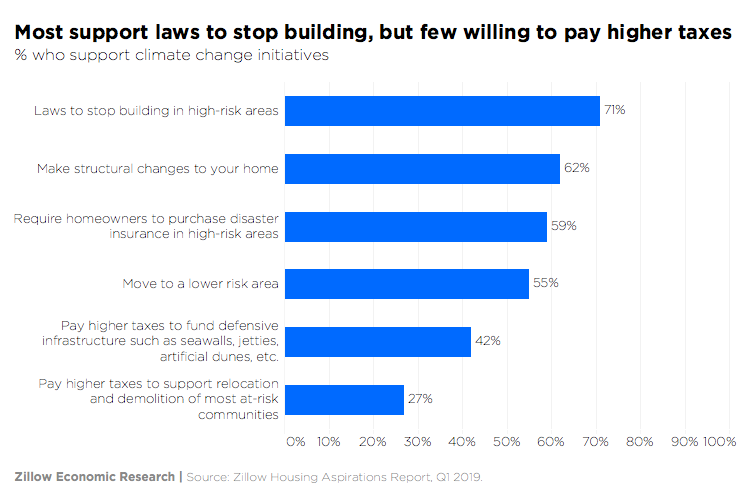

Young Adults See Climate Change Affecting Them and Support More Solutions - But Not Necessarily Taxes

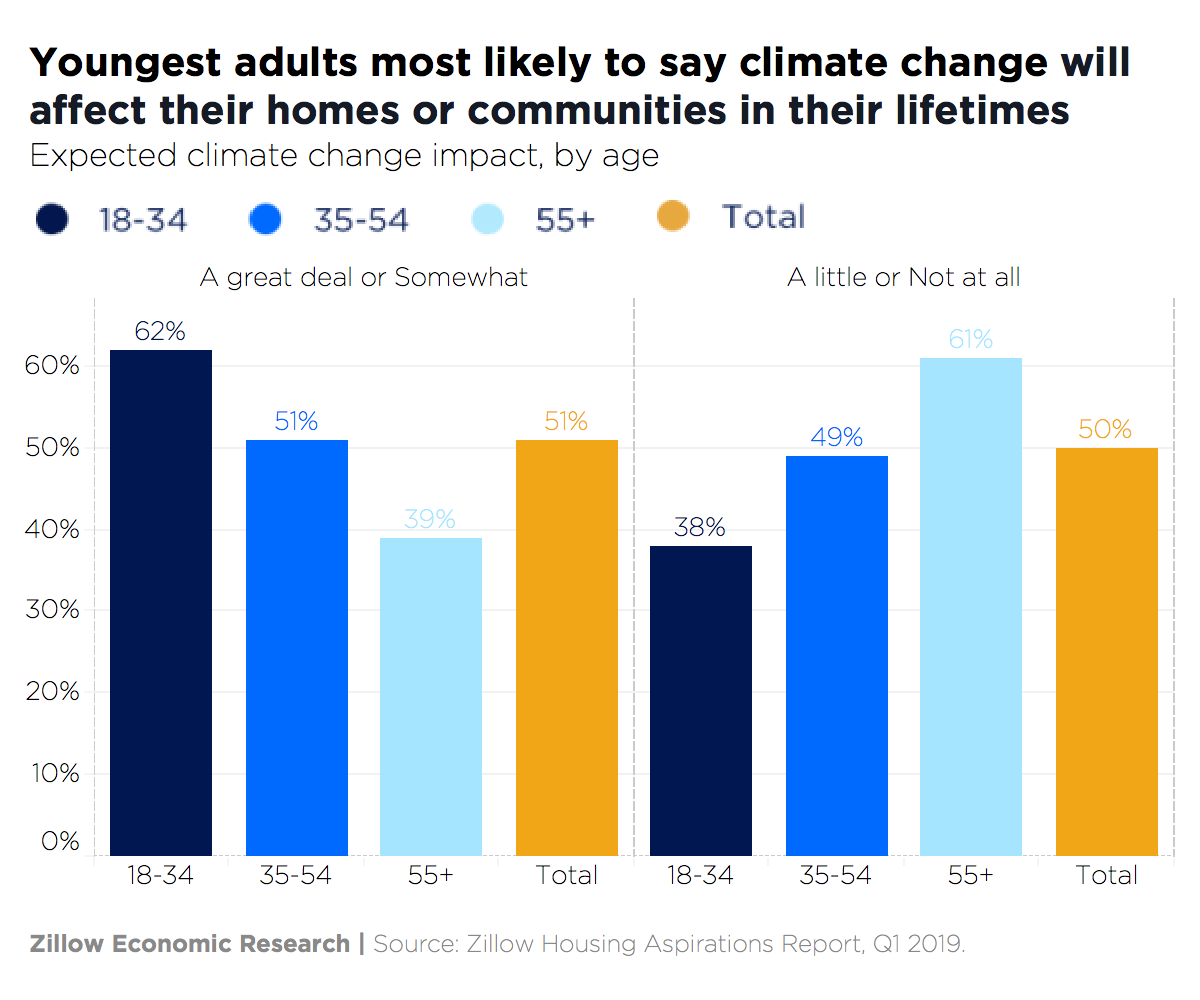

Precisely half of people who live in major U.S. metro areas say climate change will affect their homes or communities in their lifetimes, according to the Zillow Housing Aspirations Report.[i] The other half says it won't have much impact while they're alive.

While they're divided about the near-term effects of climate change, they share common ground regarding how the issue should be addressed: Taxes are nearly universally unappealing, while a surprising majority think we should stop building in high-risk areas or make structural changes to homes.

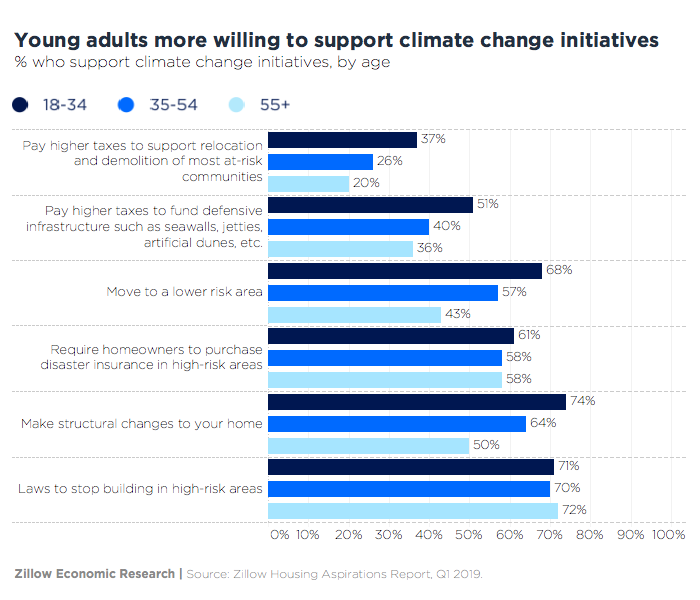

Young adults and people who live in coastal metros are the most likely to anticipate their lives will be affected by climate change.

Most young adults expect climate change to affect them personally

Not surprisingly, young adults are the most likely to perceive they will be affected by climate change. Almost two-thirds of 18- to 34-year-olds say their homes or communities will be affected either "somewhat" or "a great deal" in their lifetimes, compared to about half of 35- to 54-year-olds and 39% of those 55 and older.

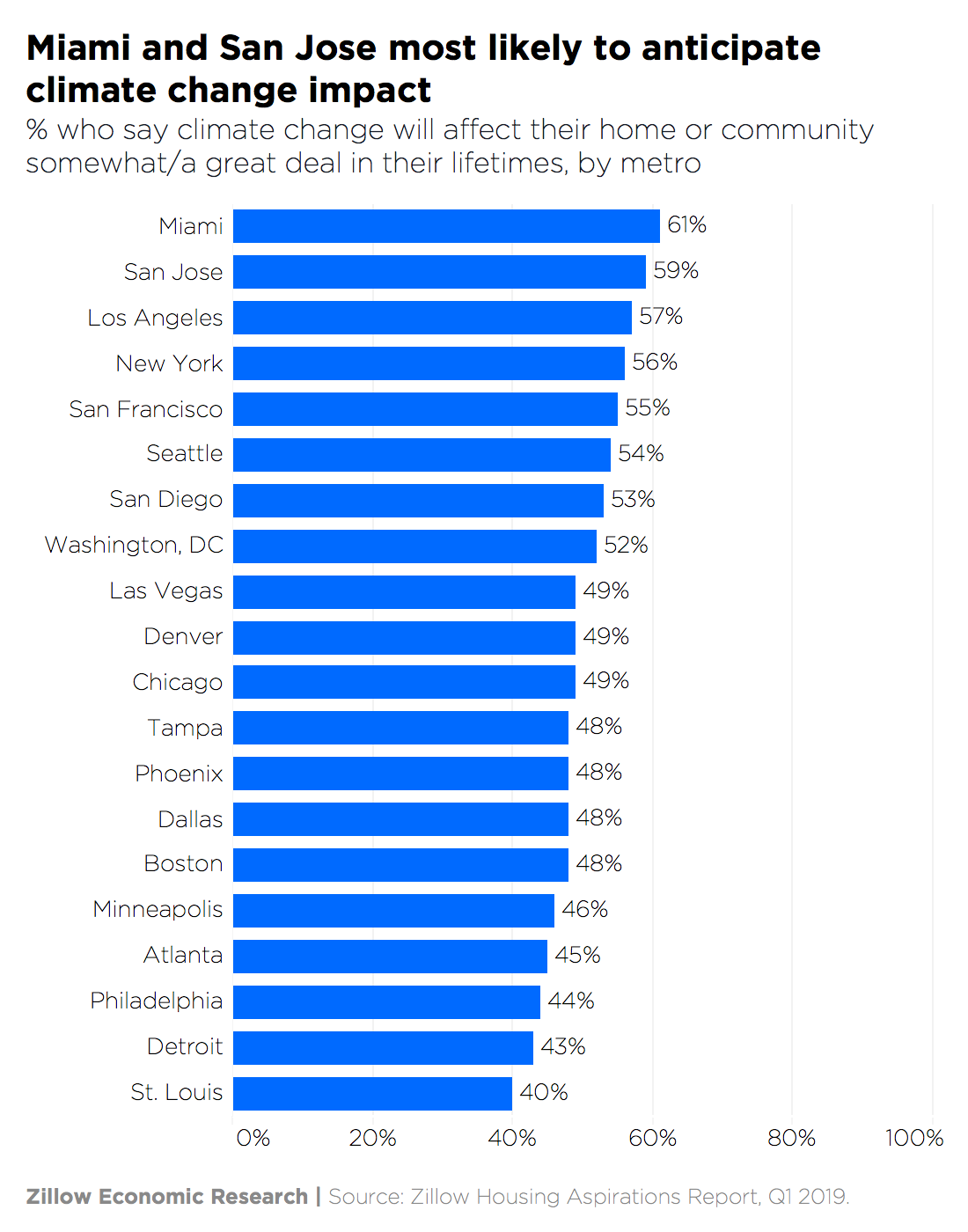

Coastal areas anticipate the most impact

People in Miami and San Jose, Calif., top the list of metros who say climate change have more than a minor impact on them – not surprising given that sea-level rise is already affecting Miami and that wildfires have plagued California in recent years.

Midwest respondents are the least likely to say they will be affected, although their numbers are still substantial: 40% in St. Louis and 43% in Detroit think climate change will have an impact on their home or community over their lives.

Consensus on a fix: Stop building, but don't increase my taxes

What the country disagrees on regarding effects, it makes up for in agreement over possible fixes.

On both sides of the political spectrum, most respondents support laws that would restrict building in high-risk areas: 78% of Democrats, 62% of Republicans and 70% who identify as independent voiced support, making it the option chosen by the largest share of respondents in each political group.

The majority also support making structural improvements to homes or enacting policies that require homeowners in high-risk areas to buy disaster insurance.

What they don't want, the majority agree, is for higher taxes to fund infrastructure such as seawalls or relocation for the most at-risk communities. Only about a quarter (27%) support increasing taxes to pay for relocation while 42% would be willing to pay higher taxes to fund infrastructure.

Young adults support more climate change solutions

Younger adults support a wider variety of initiatives to address the impacts of climate change. More than half of people ages 18 to 34 could get behind anything but raising taxes to relocate at-risk communities – although they favored that option more than other age groups.

[i] A semiannual survey conducted by Ipsos of 10,000 homeowners and renters in 20 of the country's largest metro areas.

The post Young Adults See Climate Change Affecting Them and Support More Solutions - But Not Necessarily Taxes appeared first on Zillow Research.

via Young Adults See Climate Change Affecting Them and Support More Solutions - But Not Necessarily Taxes

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Rock On! 10 Woodstock-Area Homes for the Festival’s 50th Anniversary

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, August 12, 2019

Inside the Luxe Texas Mansion the NRA Nearly Bought for CEO Wayne LaPierre

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

People Want A/C More Than They Want to Be Near Family and Friends

Shopping for a home to buy or rent is always an exercise in compromise. Maybe you get the better commute, but not the big back yard. Maybe the style is exactly right, but kitchen storage space is lacking.

It's a juggling act, and one that air conditioning wins a lot of the time.

More than three-quarters (76%) of home buyers say air conditioning is "very" or "extremely" important, and two-thirds (66.4%) of renters agree, according to Zillow Group 2018 Consumer Housing Trends Report. A far smaller share of each group says it's similarly important to be near family or friends: 46.7% of buyers and 36.2% of renters.

The divide is especially stark in hot parts of the country. In Phoenix, which at certain times of year is more hospitable to saguaros and javelinas than to humans, nearly all buyers – 96.5% — say air conditioning is "very" or "extremely" important. Being near family and friends? 31.9% say it is similarly important. Renters aren't quite as polarized, with 89.1% in Phoenix saying A/C is that important and 32.3% saying the same of being close to friends and family.

In the South – known for being hot and sticky in the summer – almost twice the share of buyers value A/C (87.6%) over being near family and friends (44%). Again, renters are less adamant: 82.2% of renters in the South consider air conditioning "very" or "extremely" important, and 37.6% say the same of being close to family and friends. Not surprisingly, the spread is similarly pronounced in Southern hotspot Atlanta, also known as "Hotlanta," where 88.6% of buyers dig their A/C compared to 41.9% who put a high value on being near family and friends.

San Francisco buyers and renters have a far less significant gap in wanting air conditioning versus valuing proximity to friends and family, which makes sense for the city that rarely sees temperatures reach 80 degrees. While more than half (55.7%) of buyers there say A/C is "very" or "extremely" important, 46.4% value being near friends and family. San Francisco renters are the only group surveyed for which the share who view close proximity to friends and family (30.3%) is greater than the share who place a high value on A/C (28.3%).

The differences vary by generation as well, with Silent Generation buyers showing a high preference (89.5%) for air conditioning over family and friends (56.7%) — possibly because they're more likely to live in warmer climates.

The post People Want A/C More Than They Want to Be Near Family and Friends appeared first on Zillow Research.

via People Want A/C More Than They Want to Be Near Family and Friends

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Drew Barrymore’s Crazy-Affordable Furniture Line Will Knock Your Socks Off

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

A Danish Bank Is Offering Mortgages With Negative Interest Rates—Why You Shouldn’t Wish for That to appen in the U.S.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hitting the Mark: What You Need to Save Daily to Buy a Home in 11 Top Cities

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, August 9, 2019

Amazon’s Selling a House for $37K? Why This ‘Bargain’ May Be a Bust

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Burnin’ Up! This Week’s Most Popular Home Was Truly on Fire

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, August 8, 2019

Even After 25% Discount, $48.5M SoHo Penthouse Is the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Foreclosure Filings Are Falling Fast—Except in These Cities

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

America’s Hottest—and Most Unexpected—Real Estate Markets in July 2019

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, August 7, 2019

Mississippi’s Most Expensive Mansion Burns Down—Declared a ‘Total Loss’

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

High Times: Cannabis the New Secret Ingredient for Luxury Real Estate Sales

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Is Baltimore ‘the Worst in the USA’? That Depends on Where You Live

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, August 6, 2019

Skip the Trip to Bali? 8 Balinese-Style Homes for Sale in the U.S.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, August 5, 2019

Drew Barrymore’s Line of Kids Furniture Is So Cute It Hurts—and It’s Full of Surprises

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

San Francisco’s Hottest Neighborhoods Aren’t Exactly Where You’d Expect

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, August 2, 2019

Which Grocery Store Boosts Home Values More: Whole Foods or Trader Joe’s?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Musicians Struggle to Afford Housing in 'Music City' Nashville

Nashville is known as Music City, but many homes on both the for-sale and rental market remain out of reach for musicians and singers. In the entire Nashville metro area, musicians could afford the monthly mortgage payment in about three-quarters of ZIP codes, thanks to low mortgage interest rates. But the typical musician could afford rent in just five of the Nashville metro area ZIP codes.

Using the median salary for a musician or singer in Nashville, and the median home value and median rent in each Nashville metro ZIP code, we calculated the percentage of income a musician or singer looking to live on their salary alone would have to spend on housing in each area. Using the rule of thumb that no more than 30% of income should go toward housing, we came up with a list of ZIP codes where musicians or singers looking to live on their salary alone were priced out. We also compared that to two other major sectors of employment in Nashville – healthcare (registered nurses) and tech (software developers).

Share of salary needed to cover the typical…

| Type of home payment | Employed individual | Musician | Registered nurse | Software developer |

|---|---|---|---|---|

| Monthly mortgage payment | 31.4% | 28.1% | 21.0% | 13.7% |

| Rent payment | 47.2% | 42.2% | 31.6% | 20.6% |

On the whole, musicians and singers are better off than the typical employed Nashvillian. They could afford the monthly mortgage payment on the median home for the metro, while the typical employed Nashvillian could not. Mortgage interest rates have remained near historically low levels, making the monthly payment more affordable. Of course, the down payment on a home is increasingly a huge hurdle for buyers across the board-and musicians are no exception. A 20% down payment on the median-valued home in Nashville is more than an entire year's salary for the typical musician.

While the typical monthly mortgage payment may be within reach, the typical monthly rent payment is largely unaffordable with a musician's and registered nurse's salary.

While the affordability of the Nashville metro area might look pretty grim for individuals, especially for musicians who come from all over for their big break, it's worth noting that many people ultimately live with at least one other person, such as a spouse, partner or roommate. In many instances, there is more than one income-earner in a household, which helps to ease some of these affordability concerns and puts more homes within reach.

Here are the ZIP codes where musicians are priced out. The monthly mortgage payment associated with the median-valued home in all other ZIP codes in the Nashville metro area fall under the 30% threshold for people earning the typical income for all three professions. In some cases, the typical mortgage payment is unaffordable even for the majority of registered nurses and software developers, who tend to have higher salaries.

Areas where a typical mortgage payment is unaffordable for musicians and singers

| ZIP Code | Primary City/Town/Neighborhood | Musician/Singer | Registered Nurse | Software Developer |

|---|---|---|---|---|

| 37027 | Brentwood | No | No | No |

| 37046 | College Grove | No | No | Yes |

| 37064 | Franklin | No | No | Yes |

| 37067 | Franklin | No | No | Yes |

| 37069 | Franklin | No | No | Yes |

| 37075 | Hendersonville | No | Yes | Yes |

| 37085 | Lascassas | No | Yes | Yes |

| 37118 | Milton | No | Yes | Yes |

| 37122 | Mount Juliet | No | Yes | Yes |

| 37135 | Nolensville | No | No | Yes |

| 37174 | Spring Hill | No | Yes | Yes |

| 37179 | Thompsons Station | No | Yes | Yes |

| 37201 | Nashville (Riverfront) | No | Yes | Yes |

| 37203 | Nashville (The Gulch) | No | No | Yes |

| 37204 | Nashville (Melrose) | No | No | Yes |

| 37205 | Nashville (Belle Meade) | No | No | No |

| 37206 | Nashville (East Nashville) | No | Yes | Yes |

| 37209 | Nashville (Sylvan Park) | No | Yes | Yes |