- Unchecked greenhouse gas emissions would put 3.4 million existing homes worth $1.75 trillion at risk of inundation from a 10-year flood by 2100.

- By 2050, those figures are 802,555 homes worth $451 billion – and 19,250 of those homes were built after 2009. New York, Tampa, Virginia Beach and 21 other cities built at least 100 homes in the risk zone during that time.

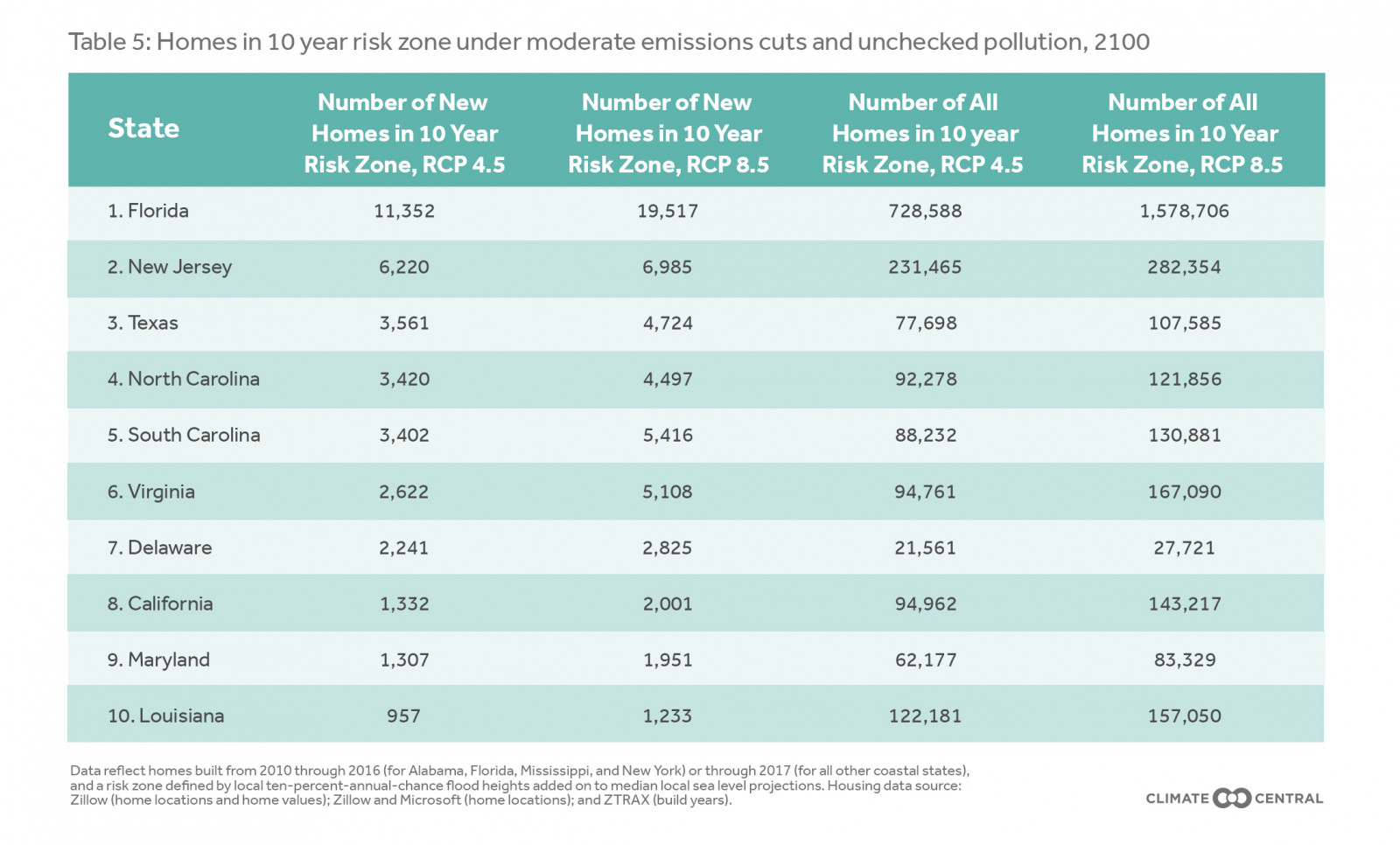

- Florida would have the most homes at risk (1.58 million) by 2100, followed by New Jersey (282,354), Virginia (167,090), Louisiana (157,050) and California (143,217)-assuming levees and other infrastructure defenses hold.

In 2012, Hurricane Sandy slammed into New Jersey, producing a major storm surge and damaging or destroying many thousands of homes. In the years that followed, builders put up new houses and reconstructed damaged ones - in many areas that will be vulnerable to more flooding in the future.

The post-Sandy rebuilding was a striking example of a broader pattern. Across the United States, coastal communities have recently built tens of thousands of houses in areas at risk of future flooding driven by sea-level rise from climate change. That has put homeowners, renters, and investors in danger of steep personal and financial losses in the years ahead.

In 2018, Climate Central and Zillow produced the first nationwide analysis of the number of new homes in areas vulnerable to coastal flooding in all 24 coastal states and the District of Columbia. The research projected how many homes will become exposed to on-average annual ocean flooding in the coming decades - depending on what choices the world makes around greenhouse-gas pollution today. This report improves those results by incorporating full home footprint data instead of point location estimates (see methodology), and also provides results for bigger floods in addition to the annual ones.

The results are clear. If the world makes moderate cuts to greenhouse-gas pollution - roughly in line with the Paris agreement on climate, whose targets the international community is not on track to meet - some 17,800 existing homes built after 2009 will, by the year 2050, risk inundation by a 10-year flood. The figures for 2100 are more than two times higher - and more than three times higher if pollution grows unchecked.

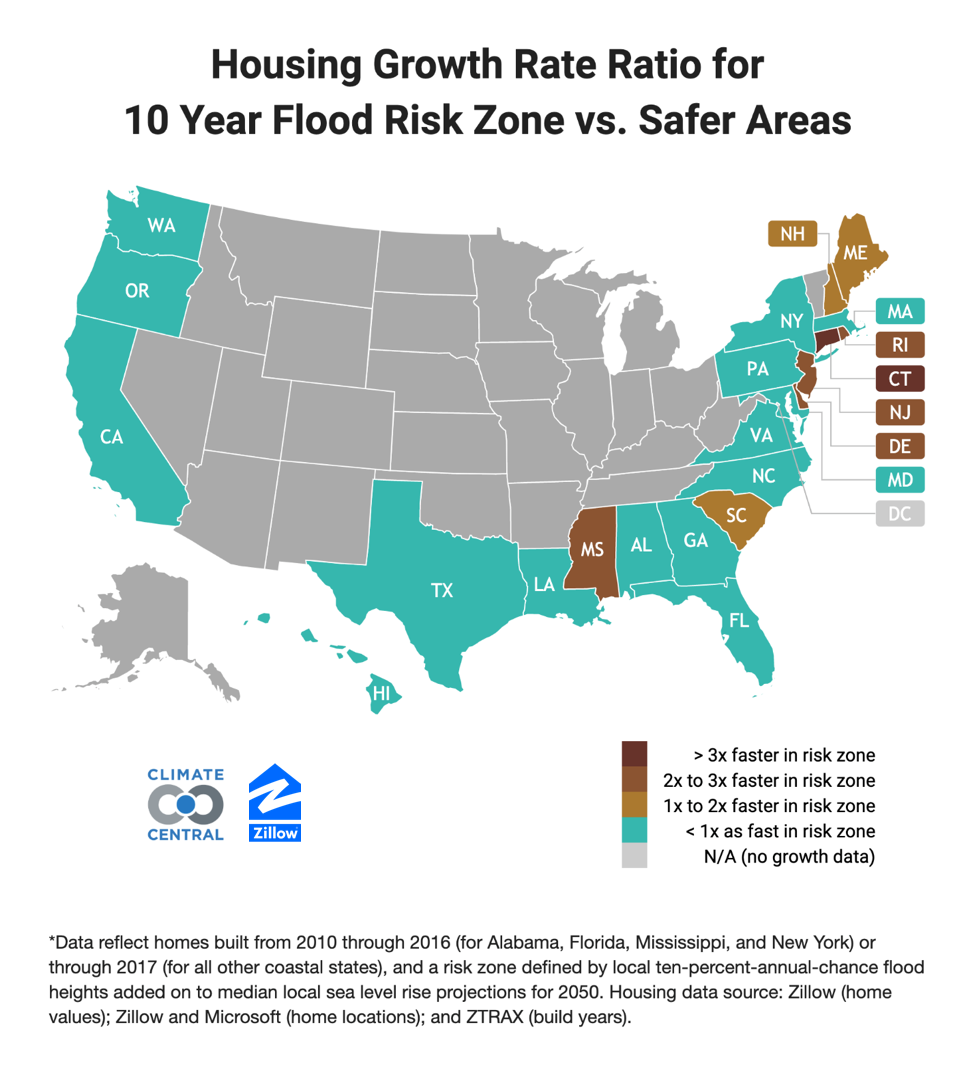

Over the past decade, public interest in sea level rise has grown, tidal flooding has increased in many coastal communities, and global attention has coalesced around the dangers of climate change in international negotiations in Copenhagen and Paris. And yet in the years after the 2009 Copenhagen meeting, a third of the country's coastal states experienced a higher rate of new home building in areas at risk of 10-year floods than in areas not at risk.

Location, location, inundation

By boosting the average water height, sea level rise is projected to make the kinds of intermittent floods that coastal communities see on average once a decade - meaning there's a 10% annual risk of this type of devastating flood- reach farther inland than they do today. Those floods can damage and devalue homes, degrade infrastructure, wash out beaches, rust out car underbodies, promote mold, and more.

Future emissions will shape the extent of those harms - and the number of homes in each coastal region's "risk zone" - in the years ahead. Unless otherwise noted, this report defines the risk zone as the area exposed to a 10-year flood threat in 2050, under the moderate emissions cuts known technically as Representative Concentration Pathway (RCP) 4.5, and under the median projections for sea-level rise corresponding to this emissions level as described in Kopp et al. 2017.[1] Other risk zones can be defined with other assumptions, such as unchecked emissions, or by looking to the year 2100, and yield different results. "New homes" refers only to currently existing structures built after 2009 and before 2017 (or before 2016 in Alabama, Florida, Mississippi and New York). "New" does not refer to homes that will be built in the future.

New homes in risk zones are not evenly distributed across the country's coastal states. Local factors, from the size of the population and the condition of the economy to the amount of space available, shape the development of new housing stock in each community. And the size of a risk zone is itself the product of a variety of elements, from land elevation to the presence of protective features such as levees.

Fairly comparing the pattern of new construction in risk zones across different cities, states or counties requires tracking more than just raw numbers. For this analysis, we compared percentage growth in housing within the flood-risk zone with percentage growth outside of it, producing a single, comparable ratio for each place.

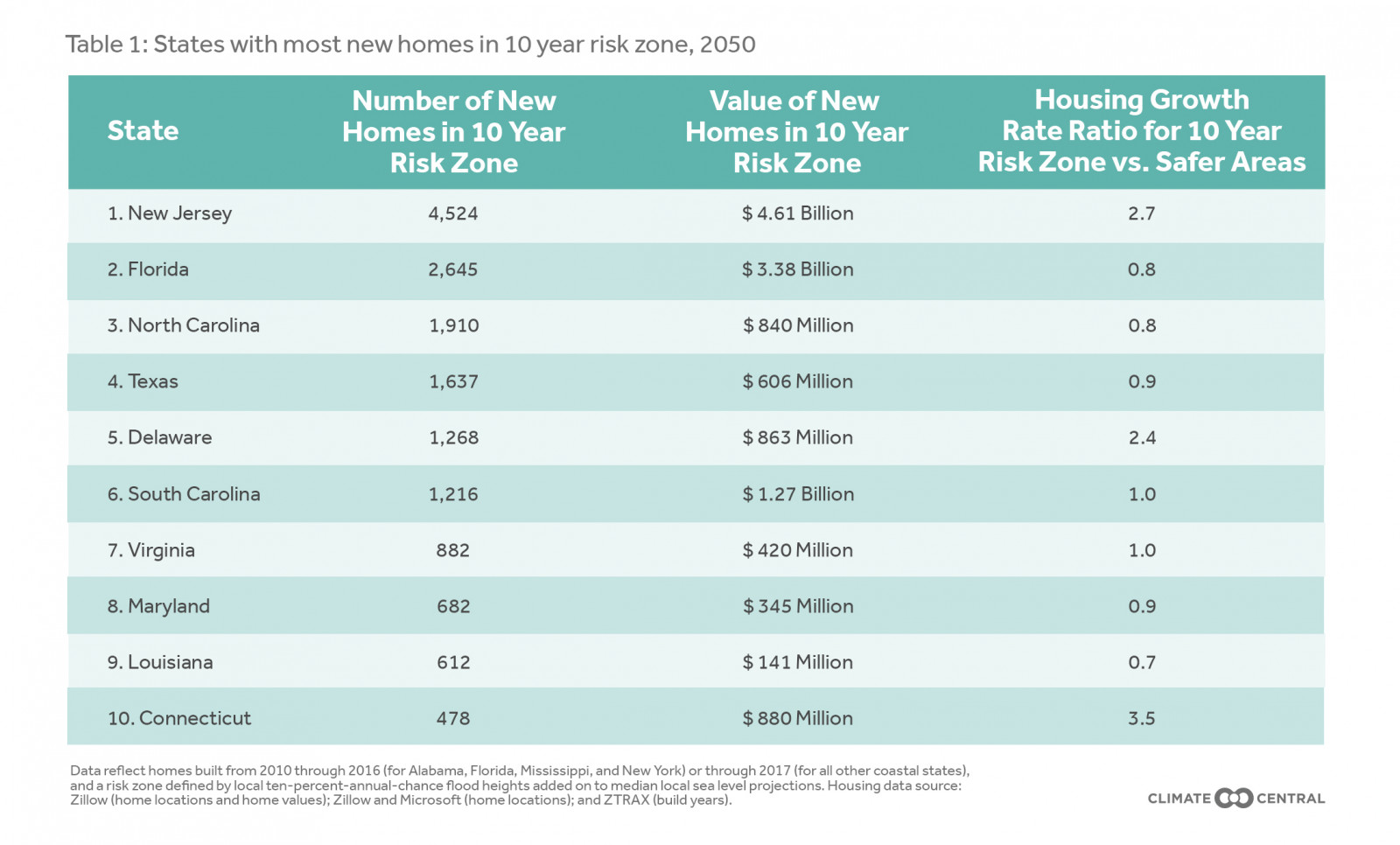

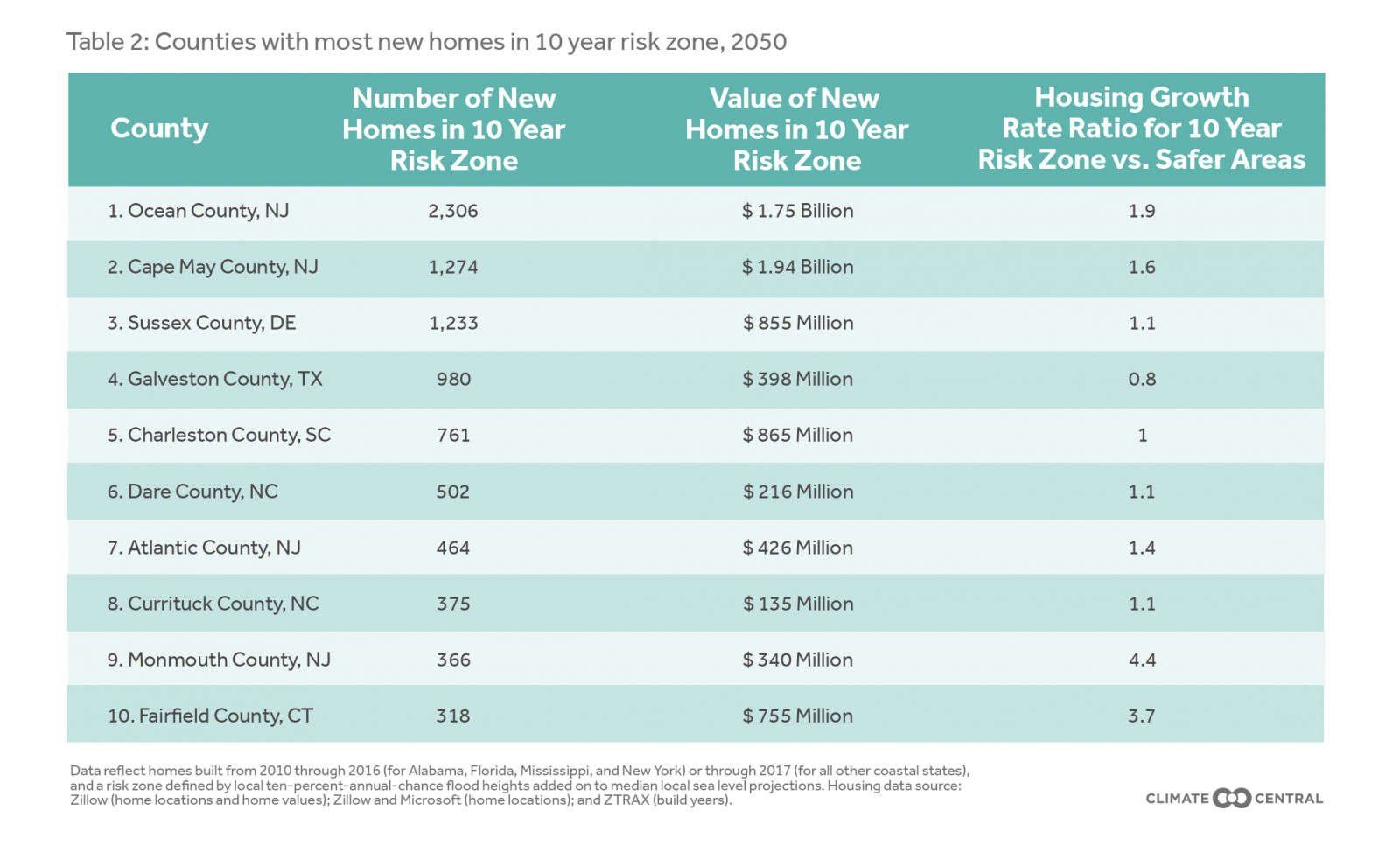

Take the state of New Jersey. After 2009, the housing growth rate was nearly three times higher in the coastal flood risk zone than in safer areas. Around 4,500 new homes, worth some $4.6 billion, were added in the flood-risk zone after that year - most likely driven by reconstruction following Hurricane Sandy. In Connecticut, meanwhile, the ratio of risky growth to less risky growth was even higher, at around 3.5 times. And in Florida, where the recent risk zone growth rate has lagged the growth rate in safer areas, some 2,645 newly built homes are nevertheless in locations at risk of flooding at least once each decade by 2050.

Six other coastal states likewise saw their construction growth rates in the risk zone outpace growth rates in safer areas. (In addition to the states listed in Table 1, these include Maine, Mississippi, New Hampshire, and Rhode Island.) A third of the country's coastal states, in other words, have recently seen higher housing growth rates inside the 10-year flood-risk zone than outside it.

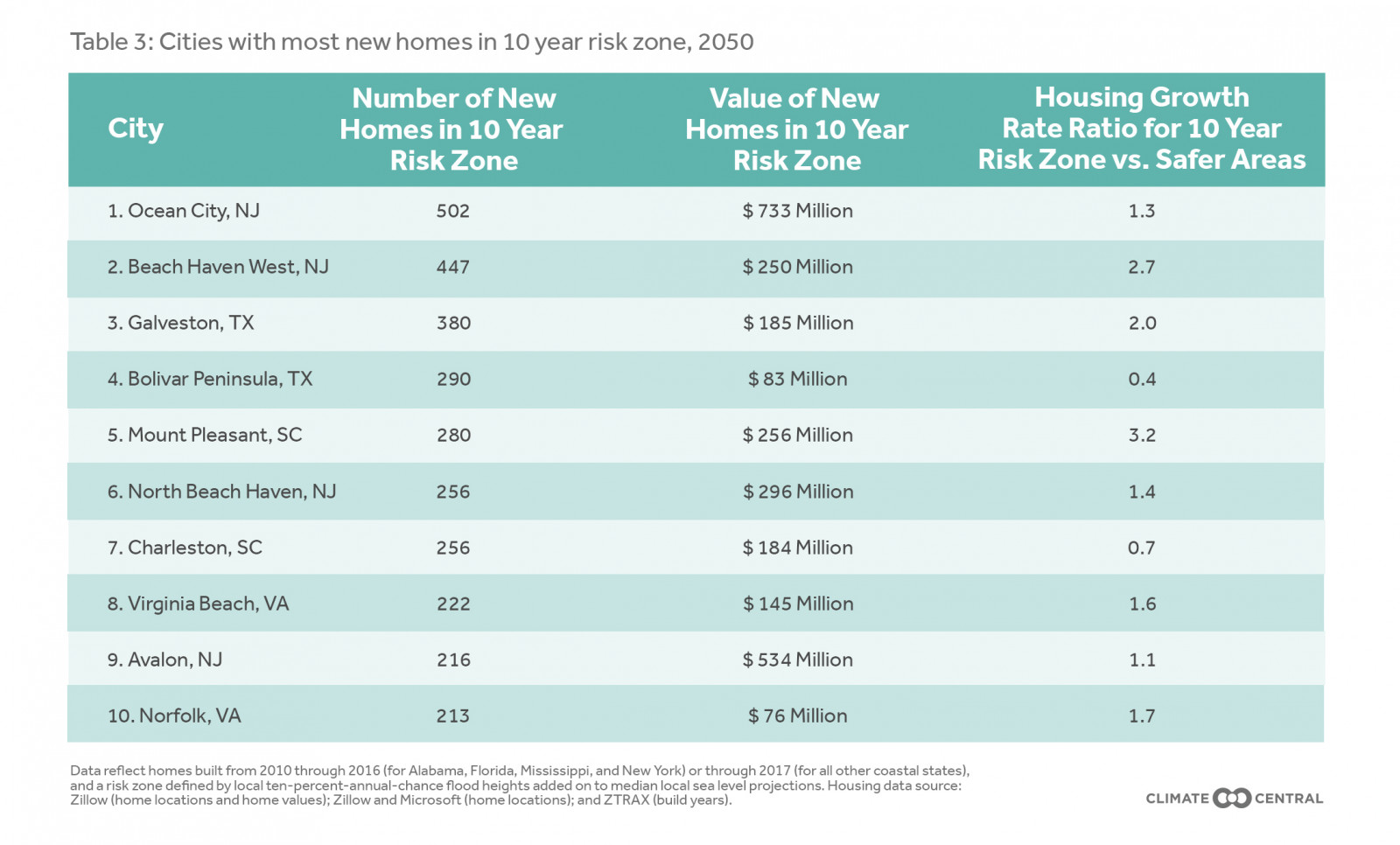

Counties and cities

Just as the growth in new risk-zone housing is unevenly distributed across states, so it is unevenly distributed within them. There are 37 counties where more than 100 at-risk homes were built after 2009. All those counties are in 12 states: Connecticut, Delaware, Florida, Louisiana, Maryland, Mississippi, North Carolina, New Jersey, New York, South Carolina, Texas, and Virginia.

In 24 cities, at least 100 homes were built in the risk zone after 2009. None built more than Ocean City, N.J., a popular resort town in Cape May County, which put up some 500 new houses in the risk zone.

The larger cities of New York City, Tampa, and Virginia Beach also rank among the cities with more than 100 new homes in areas of future 10-year flood risk.

Flooding the market

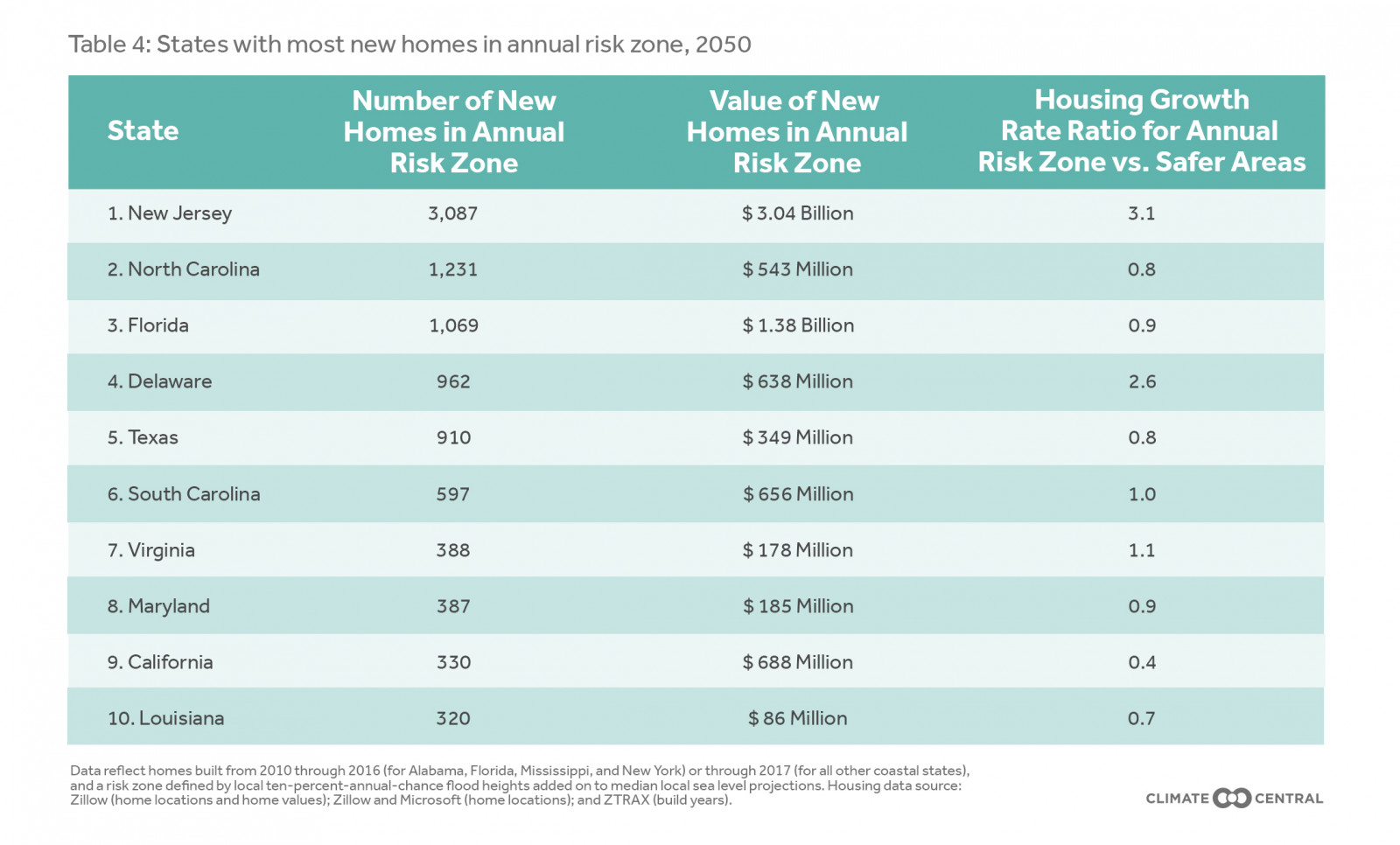

This report has so far focused only on the 10-year flood zone. But it is also possible to look at annual floods, occurring on average once per year - less extreme events that inundate less land than do decadal floods, but on a more frequent basis.

Overall, some 10,500 newly built homes are on land that will lie within the annual flood zone by 2050 - some 7,000 fewer than will lie in the 10-year flood zone. In New Jersey alone, about 3,100 will lie in the annual flood zone by 2050.

What's more, pollution scenarios beyond the moderate emissions cuts described in this report are possible. Instead of making the kinds of moderate emissions reductions pledged in Paris, the world might achieve deep cuts. Alternatively, humanity could pour greenhouse gases into the atmosphere unchecked.

How would these alternatives affect the 10-year flood risk to recently built U.S. homes? By 2050, not a lot. Moderate cuts to pollution would leave just over 17,800 new homes in the risk zone. Deep cuts in emissions - what the Intergovernmental Panel on Climate Change calls RCP 2.6 - would trim that figure to about 17,250. And unchecked pollution, or RCP 8.5, would place 19,250 homes in areas in danger of flooding at least once per decade, on average.

By the end of the century, however, there will be significant differences in the dangers that these emissions scenarios pose for coastal homes. Deep cuts would leave about 27,750 recently built homes at risk. Moderate reductions akin to those pledged in the Paris agreement would boost that number to 40,800. If greenhouse-gas pollution rises unchecked, 60,500 of today's new homes would lie in the ten-year flood-risk zone by 2100.

More striking still is that those 60,500 just-built homes would represent a tiny fraction of the total number of homes at flood risk. Unchecked pollution would give each of 3.4 million existing homes a risk of inundation by a 10-year flood by 2100. That figure is 802,555 homes by 2050. Those properties are currently worth some $1.75 trillion - an amount equal to about nine percent of the U.S. economy.

No state has more to lose from such an outcome than Florida, where about 8,150 more new homes are projected to be in the flood-risk zone by century's end if greenhouse-gas pollution continues unabated than if moderate cuts are achieved. When all home vintages in the state are considered, the difference is even starker. Unchecked pollution would put about 850,000 more Florida homes in flood-risk zones than would moderate cuts - and 1.2 million more than deep cuts.

Methodology

Sea level and flood projections

This analysis determines the maximum local land elevations that define risk zones by projecting future local sea levels and adding the height above sea level that local floods exceed on average once per year.

Local sea level projections are based on a recent peer-reviewed research paper (Kopp et al. 2017)[1] building off of global projections from the Intergovernmental Panel on Climate Change and emerging research on the potential instability of Antarctic ice sheets (DeConto and Pollard 2016)[2], which could lead to significantly more sea level rise in the second half of the century. Climate pollution scenarios modeled include "unchecked pollution" (technically, Representative Concentration Pathway 8.5, or RCP 8.5), "moderate carbon cuts" (RCP 4.5), and "deep carbon cuts" (RCP 2.6), this last choice meaning a peak in emissions near the year 2020 followed by a sharp decline to zero near 2070 and then by net negative emissions. The sea level model was run for thousands of simulations given each scenario. Median projections under each scenario for the years 2050 and 2100 are used, reflecting mid-range sea level sensitivity to climate pollution. Lesser or more severe outcomes are possible, with 5th and 95th percentile results available in the Risk Finder tool (scroll to the "Future Flood Risk to Homes" section of the tool after typing a city, county, or state name, and click on the gear-shaped settings icon at the top right of the panel).

Levels for annual average and decadal floods were derived using methods from Tebaldi et al. 2012[3], with water level station data updated through the end of 2015 for 71 stations around the United States. This approach assumes no future changes in the frequency or severity of coastal storms or tides, as compared to past decades. Some research indicates climate change will worsen future storms. Storm surge associated with major hurricanes has already been increasing over the last century.

Defining risk zones

"Risk zones" are first classified as areas with elevations below local projected sea levels plus annual or decadal flood heights. Assessment is based on accurate, high-resolution, lidar-derived elevation data provided principally by the National Atmospheric and Oceanic Administration (NOAA). Initial risk zones are then refined by removing low-lying areas that appear to be protected from the ocean by natural topography or by levees. This approach is called using a "bathtub model," since it relies only on how still water would fill a landscape, like water filling a tub, without accounting for factors such as wind, waves, or rain that give actual floods dynamic and uneven surfaces. Bathtub models are appropriate for mapping pure sea level projections, and make reasonable approximations for more modest floods, such as average annual or decadal ones.

Dynamics play a larger role in rarer and more violent storms, such as "hundred-year floods," so bathtubs are less appropriate for these. More sophisticated methods using hydrodynamic simulations can take many factors into account that bathtub models cannot, but require large amounts of computing power to characterize well the thousands of combinations of sea level, tides, wind, waves, and rain that any location might experience in the future.

Levees, walls, dams, or other features may protect some areas, especially at lower elevations. Data limitations, such as an incomplete inventory of levees and a lack of levee height data, make assessing the protection afforded by levees difficult. Levees are particularly prevalent in Louisiana and in the Bay Area and San Joaquin delta region of Northern California. Missing or mischaracterized levee data in these areas may have important effects on results, including known overestimates of exposure due to missing levee data in Northern California. We use data from the FEMA/USACE Midterm Levee Inventory for our national flood control structure dataset, and supplement this with local data from Louisiana and Massachusetts. This analysis does not account for future erosion, marsh migration, or construction. As is general best practice, local detail should be verified with a site visit.

We assume for purposes of this analysis that levees are always high and strong enough for flood protection. However, the American Society of Civil Engineers rated only eight percent of monitored levees as in "acceptable" condition, and some areas and assets that appear to be protected by levees, ridges, or other features may not actually be protected. Areas may have hidden connections through porous bedrock geology, as is common in South Florida, another area with plentiful levees that line drainage channels and canals. Low-lying areas may also be connected by channels, breaks in levees or seawalls, or drainage passages that are not captured by the elevation data, such as sewers. There is further no guarantee that existing levees will be maintained through 2050 or 2100. On the other hand, new defenses could also be built within these timeframes.

Housing data

Homes whose geographic coordinates lie within or outside of risk zones were separately counted and their values, which were estimated by Zillow, were summed. Zillow provided location, value data (Zestimates), and build years for homes built through 2016 (for Alabama, Florida, Mississippi, and New York) or 2017 (for all other coastal states). Separate tallies were made for homes built in 2010 or later, versus 2009 or earlier. The data do not include build year for some homes; these homes were included in analyses for all homes. Only homes with known build year were included in calculations of housing growth rate, which was computed as homes built in 2010 or later, divided by homes built in 2009 or earlier.

Geographic coordinates of homes within the Zillow database may also contain errors, especially in low-density rural areas. However, we have empirically found such errors to be virtually random with nearly zero bias, so exposure totals aggregated to larger administrative boundaries, such as cities and counties, are expected to accurately reflect actual vulnerability.

For our 2019 update, Zillow data were further refined using Microsoft’s U.S. Building Footprints database (accessed via a Creative Commons Attribution 4.0 International Public License). If any part of a building was lower than a flood's height, then the entire structure was considered vulnerable. For each building footprint, we determined the lowest land elevation within it. We then associated each home's point coordinates, from the Zillow database, to its closest building footprint, and assigned the structure its corresponding elevation.

Zillow property and Zestimate data were refined to ensure a set of unique properties with complete addresses and home valuations (Zestimates). Zillow data include single-family homes, condominiums, and other homes in multi-unit properties, such as duplexes and triplexes - in other words, units where the tax parcel is a single dwelling unit. Buildings zoned for commercial residential use, such as apartment buildings, are not included, and so total housing counts using these data are generally lower than corresponding estimates using the 2010 census.

Address and built year data were provided by Zillow through the Zillow Transaction and Assessment Dataset (ZTRAX). More information on accessing the data can be found at http://www.zillow.com/ztrax. Proprietary Zillow data, such as Zestimates, were provided under strict confidentiality.

[1] Kopp, R. E., DeConto, R. M., Bader, D. A., Hay, C. C., Horton, R. M., Kulp, S. , Oppenheimer, M. , Pollard, D. and Strauss, B. H. (2017), Evolving Understanding of Antarctic Ice‐Sheet Physics and Ambiguity in Probabilistic Sea‐Level Projections. Earth’s Future, 5: 1217-1233. doi:10.1002/2017EF000663

[2] DeConto, Robert M., and David Pollard. “Contribution of Antarctica to past and future sea-level rise.” Nature 531.7596 (2016): 591.

[3] Tebaldi, Claudia, Benjamin H. Strauss, and Chris E. Zervas. “Modelling sea level rise impacts on storm surges along US coasts.” Environmental Research Letters 7.1 (2012): 014032.

[1] Kopp, R. E., DeConto, R. M., Bader, D. A., Hay, C. C., Horton, R. M., Kulp, S., Oppenheimer, M., Pollard, D., & Strauss, B. H. (2017). "Evolving Understanding of Antarctic Ice-Sheet Physics and Ambiguity in Probabilistic Sea-Level Projections." Earth's Future, 5, 1217–1233, https://ift.tt/2BVVXfj

The post 802,555 Homes at Risk of 10-Year Flood Inundation by 2050 appeared first on Zillow Research.

via

802,555 Homes at Risk of 10-Year Flood Inundation by 2050