Banks continue to tighten lending standards in the face of persistent economic uncertainty. Mortgage delinquencies and foreclosures are up, but the overall health of the mortgage market is stronger than the headlines suggest. And the rent keeps getting paid at professionally managed buildings.

Lending standards tightened further in 2020's third quarter

In Q3,the share of banks saying they tightened lending standards was, on net, 11.5 percentage points higher than those that said they loosened standards, according to the Federal Reserve.

For-purchase mortgage applications fell week-week again, but remain 16% above last year's pace.

Don't read too much into seemingly big increases in delinquency & foreclosures

1.2% of loans are at least 150 days past due according to CoreLogic, and ATTOM reported that foreclosures increased 20% in October.

The increased long-term delinquency is due to participation in forbearance programs, and foreclosures are down 80% year-over-year.

Rental payment rates continue to hold firm

80.4% of households living in professionally managed apartments paid at least part of their monthly rent through November 6, according to the National Multifamily Housing Council.

That rate is just 1.1 percentage points below last year's levels and ahead of the 79.4% payment rate at this point in October.

So what?

Despite the fact that many sectors of the economy experienced meaningful improvements in Q3, banks further tightened lending standards on all loan types — including mortgages — citing a still-uncertain economic outlook. The net percentage of banks applying more stringent criteria to their mortgage lending practices was far less than the net share in Q2 2020, when the difference between the share of banks tightening standards and the share loosening standards was more than 50 percentage points. Still, the Q3 reading was far above any reading prior to the pandemic.While the still-elevated level of tightening signifies that banks are being extremely cautious given the tentative economic outlook, mortgage lenders' restraint is likely also a product of demand. Mortgage rates have remained at or near all-time lows for months, something that has prompted a surge in demand both for home purchase loans and refinances.Applications for mortgages remain well above last year's levels, as well as levels from the past several years, even as purchase loan applications have slipped recently compared to prior weeks.

Mortgage delinquencies and foreclosures increased in August and October, respectively, but those increases likely exaggerate any claims that the mortgage market is broadly unhealthy — though the data do point to some looming challenges for the market. CoreLogic's measure of "extremely delinquent" loans – those at least 150 days past due – reached its highest level ever in August, twice where it was in January 2010 at the height of the Global Financial Crisis.But the uptick is driven by widespread participation in mortgage forbearance programs, and encouragingly, the share of loans delinquent between 30-and-59 days fell year-over-year. The uptick in foreclosures was maybe more surprising, given participation in forbearance programs, but the notable monthly increase fails to account for the bigger picture. Even though foreclosures increased 20% in October from September, they remain down almost 80% year-over-year.Foreclosure activity remains very low overall, though an increase of some kind should be expected if/when forbearance programs expire in 2021. What impact that will have on the housing market remains to be seen, but early indications suggest that government support and high levels of accumulated home equity should dampen the impact.

The share of households living in professionally managed apartment properties who made a November rent payment in the first week of the month fell slightly from last year's rate but not alarmingly so, continuing a trend that has played out since the early spring. The 1.1 percentage point difference in payment rates through November 6 2020 and 2019 was notably smaller than the annual differences recorded in the summer months. That said, the more-or-less steady payment rate may be masking some underlying issues plaguing the broader rental market.The report doesn't identify what share of the 80.4% of households that made a payment only paid part of their rent and/or were only able to stay current because of an accommodative arrangement made by their landlord that may require larger payments down the road. Additionally, this report only examines payment rates in larger, professionally managed rental properties which, in some cases, may have a larger financial buffer than landlords of smaller operations. Lastly, people's ongoing ability to make rent may fade going forward as savings generated from direct stimulus checks and other measures earlier in the year start to dwindle.Still, the fact that a key measure of rental rates hasn't plummeted is obviously a good sign for the state of the housing market.

Click here to read past editions of Zillow’s Market Pulse updates.

The standard pandemic narrative goes something like this: COVID-19 pushed renters into fleeing their tiny, claustrophobic apartments in the big, expensive cities—in turn causing monthly rents to plummet. However, it turns out that’s only partly true.

Nationally, monthly rents continued to fall for studios, typically the smallest spaces, according to realtor.com®’s October rental report. However, they’re rising again for one-bedroom units and the more desirable two-bedroom abodes. The latter provides extra space, including an extra bedroom, which some folks are turning into makeshift offices.

“We’re seeing the impact of workplace flexibility on rents. Renters are more free to pick up and move,” said realtor.com Chief Economist Danielle Hale. “They’re leaving expensive areas. They’re looking for more space and to cut back on expenses and spend less on rent.”

That makes sense as folks fearing another pandemic-related lockdown are seeking out additional square footage—even if they stay in the big cities.

Nationally, the median rent for a studio fell 0.8% year over year, to $1,316 a month in October, according to the report. But in a twist, rents shot up 1.1% for one-bedroom units, to a median $1,495 a month. For two-bedroom units, rents rose 2.6% annually, to $1,869. While two-bedroom rents are picking up, they’re still below the 3.5% annual growth rate before COVID-19.

Realtor.com looked at rental prices in the 100 largest U.S. counties with at least 20 listings for studios, one-bedrooms, and two-bedroom units on the site. The rentals included apartments, condos, townhomes, and single-family homes.

“Still in a lot of the biggest markets, two-bedroom rents are falling but not by as much. Everywhere people are looking for more space,” says Hale. “If you have the opportunity to trade up, a two-bedroom can make more sense than a smaller [unit].”

Some renters may also be moving in with family and friends to save money—so all of a sudden that extra bedroom becomes a necessity.

Nationally, the largest price cuts were in San Francisco, one of the nation’s priciest housing markets. Many renters who stuck around after some of the largest tech companies announced employees could work remotely until the summer or even indefinitely were able to score steep discounts.

San Francisco studio rents fell 33.5% year over year, to a median $2,180 in October. The tech hub also saw drops of 26.3% for one-bedroom units, to $2,800, and decreases of 23.4% for two-bedroom rentals, to $3,810.

Manhattan’s rental market also took a hit in a boon for renters. The median rent for a studio dropped 20%, to $2,395 a month. One-bedroom rents fell 16.7%, to $3,250, while two-bedroom rentals were 11.1% cheaper, at $5,333 a month.

“These cities are expensive. They have a lot of workers who are working remotely now,” says Hale. “These are [also] cities that tend to attract a lot of students and recent graduates, and they’re probably not setting out for these cities right now.”

A heavenly conversion of a historic Minnesota church made a divine impression on home shoppers. The transformed house of worship ascended to the top of this week’s 10 most popular homes on realtor.com®.

Former churches make for intriguing single-family homes thanks to their impossibly tall ceilings, wide-open spaces, and stained-glass windows that let in streams of colored light. There’s also the connection with living in a home that served as a sacred space for so many. We’ve seen quite a few converted churches arise in our weekly accounting of the most popular properties—and for home buyers who want a home unlike any other, these holy houses make perfect sense.

This example in Minnesota features cozy, carved-out spaces; a modern kitchen; and a smart use of space and existing architectural elements. Peep at the listing photos to see if you feel the spirit of inspiration move you.

Aside from the converted church, you also clicked on a home owned by New York Yankees legend Andy Pettitte, a Washington, DC, mansion made for megafundraiser events, and a sprawling Bucks County farm dating to 1704.

And, of course, there were a couple of quirky contenders this week, including a Kansas hunting lodge with a private gun range and an unfinished, solid cement house in Texas.

However, it’s the church transformed into a family home that gets all the praise this week. And to that, we say, “Amen!”

Price: $1,750,000 Why it’s here: Sitting at the end of a private cul-de-sac on 1.5 acres, this estate is built for fun. It features an outdoor sport court, custom playground, 50-foot party pavilion, and in-ground chess board. Built in 1994, the six-bedroom house measures 8,582 square feet, which is plenty of space to accommodate friends and family.

Price: $199,000 Why it’s here: An Alpine-style resort in the Carolinas?! This rustic three-bedroom mountain retreat is just minutes from Beech Mountain Ski Resort.

Highlights of the house in the woods include large windows, an oversize deck, wood-burning fireplace, as well as a sleeping loft accessed by a spiral staircase. The two loft bedrooms are separated by privacy panels and share a bathroom.

Price: $8,900,000 Why it’s here: This 33-acre Bucks County property is known as Finale Farm and dates to 1704. One room, believed to be the original log cabin on this parcel, features Dutch doors and a walk-in fireplace (yes, really!).

But the rest of the 6,323-square-foot, seven-bedroom home is strictly modern. The grounds include a patio, formal gardens, two-story bank barn, and lake house overlooking the lake and creek.

Price: $374,000 Why it’s here: Historic and stately, this Greek Revival dates to 1912. It combines two lots for a total footprint of a third of an acre.

The interiors could use some love, but they possess plenty of potential. There are a number of charming, one-of-a-kind details, including the outdoor meditation pond and bar, a greenhouse with shower, and wraparound porches. It even comes with a shed that could be converted into a guesthouse.

Price: $12,800,000 Why it’s here: Built in 1840 to accommodate a crowd, this prestigious 10-bedroom home in the heart of Georgetown measures in at a whopping 11,100 square feet.

The grounds are meticulously groomed and feature greenhouses, a bowling green, herb garden, and boxwoods. Hosting large-scale events for visiting dignitaries is a breeze thanks to the entertaining pavilion with fireplace, a pool, and a four-bedroom guesthouse.

Price: $350,000 Why it’s here: This concrete structure on a 5-acre lot isn’t done, which might be attractive to a buyer looking to create something unique.

Whatever the finished product looks like, it’ll be a perfect spot to create the rooftop deck of your dreams. The listing notes that the concrete home can support up to 50 people on the roof or even a hot tub.

The proposed five-bedroom structure was started way back in 1999, and it could be turned into a business, bar, or anything else a new owner dreams up.

Price: $3,499,999 Why it’s here: This gorgeous Colonial is being sold by former Yankees ace Andy Pettitte. The six-bedroom beauty sits on an acre lot at the end of a cul-de-sac. Built in 2002, the home includes lavish touches like a two-story foyer, library, large rec room, and an unfinished basement.

Price: $390,000 Why it’s here: Jazzy and modern, this striking home from 2016 sits in the Faubourg Delassize neighborhood. Petite and perfect, the three-bedroom home is not only beautiful—it’s functional, too. It’s also wired for security and includes a lovely backyard with privacy fence.

Price: $1,100,000 Why it’s here: The current owners of this lodge have a passion for exotic animals, which is apparent in the parrot-themed stained glass, tiger skin rugs, and lions emblazoned across the double front doors. The 13,554-square-foot house was built in 1964 and would make a good bed-and-breakfast, according to the listing.

There’s also an observation tower and a huge entertainment space used as the “trophy room” with bar and sound system. Most important for a marksman who doesn’t want to leave the house, this place comes with an indoor rifle range.

Price: $269,900 Why it’s here: This historic church from 1900 has undergone a gorgeous transformation. It’s now a modern two-bedroom, 3,027-square-foot home that artfully incorporated the structure’s architectural history.

And there’s even some customization work left for a buyer. A partly finished basement beckons a new owner to bless it with whatever her heart desires.

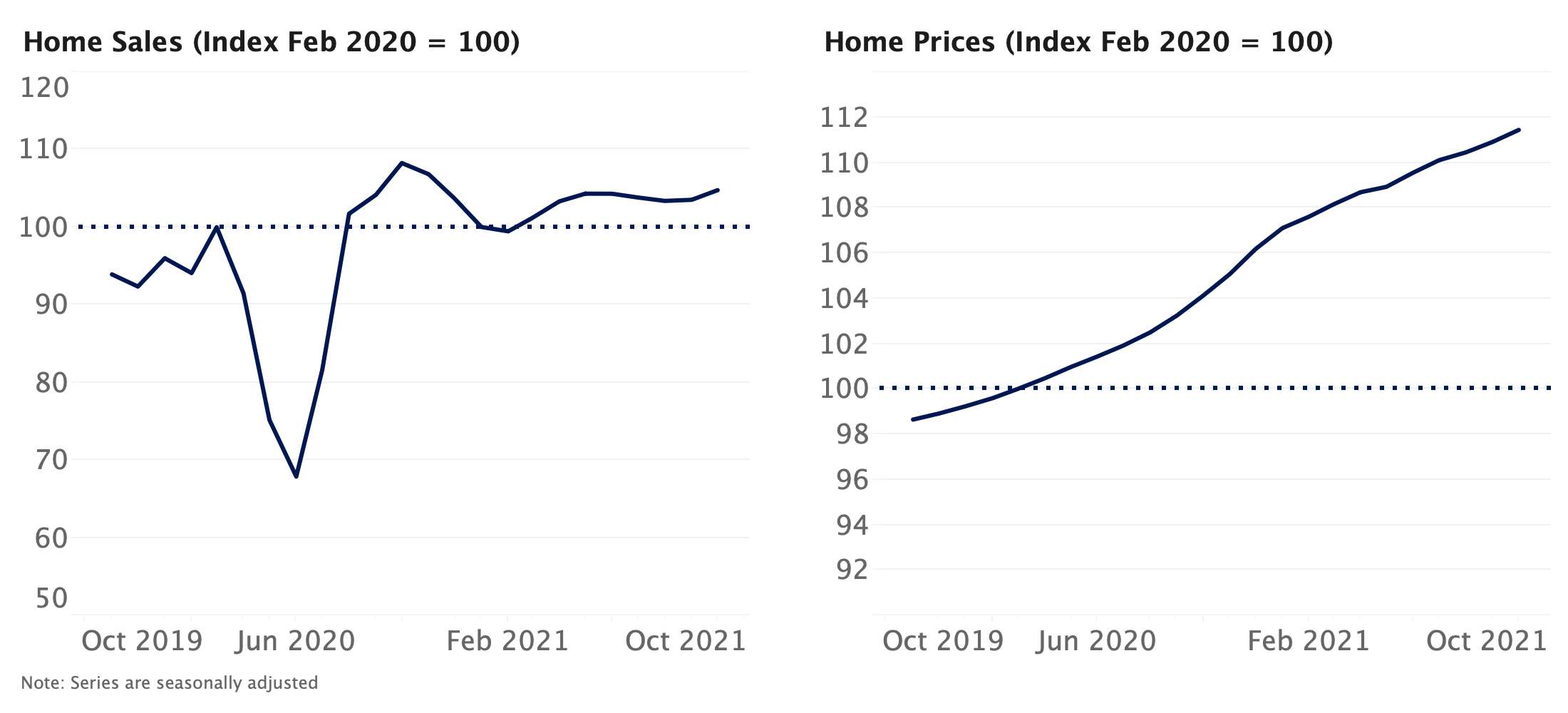

The number of days homes are staying on the market remains at a record-low in the face of intense and persistent buyer demand. Sales are at levels not seen since prior to the Great Recession and are expected to remain high, and prices continue to grow quickly.

September was the best month for existing home sales since 2006

Closed sales of existing homes continued togrow at a torrid pace in September, rising 9.4% from August and 20.9% year-over-year to a seasonally adjusted annualized rate (SAAR) of 6.54 million — the highest rate recorded in any month since early 2006, according to data from the National Association of Realtors (NAR).

Buyer demand remains very high and sales volumes are expected to stay elevated in coming months, especially relative to last year. But modest slowdowns in mortgage application and pending sales data indicate sales are likely to recede somewhat in coming months:

Seasonally adjusted purchase mortgage application activity remains 25% above typical levels seen from 2016 through 2019, but has fallen 7.9% from recent highs in mid-September.

NAR's seasonally adjusted pending sales index (a leading indicator of closed sales to come in the next 1-2 months) slipped 2.2% in September from August – the first monthly decline since April (though the index remains 20.5% above last September's levels).

Time on market matches record lows

Robust buyer-side demand persisted through October. For the fourth consecutive week, homes typically stayed on the market for 12 days, a full 17 days faster than the same time last year.

There were 25,158 listings that went pending last week, similar to volume seen in near-peak buying periods of late April and early July in 2019.

Pending sales were up 19.7% year-over-year, though they have slowed 3.1% since last month and 1.3% since last week.

Scalding homebuyer demand continues to drive inventory lower

Available inventory fell for the 23rd straight week and is now down 37.4% compared to last year. Demand for homes is still sky high, and current homeowners cite a lack of confidence in their ability to secure and afford a new home amongreasons they're not selling.

New listings on the market dropped 7.4% year-over-year, and were down 7.9% from the week prior.

Price growth continues months-long stretch of uninterrupted annual growth

Median list prices have grown year-over-year in every week since early May, and are now up 11.8% from the same period a year ago. Compared to last week, typical list prices were down $500, to $345,500 — the first weekly drop since mid-April.

Homeowners that do decide to sell are realizing big gains. Median sale prices rose to $289,625 in the week ending Sept. 19 (the latest week for which sales price data is available), up 12.5% over the same period in 2019.

Home value growth expected to continue accelerating in coming months

We expect seasonally adjusted home values to increase 2.9% between September and the end of 2020, and rise 7% in the 12 months ending September 2021. This forecast is notably more optimistic than previously: Our prior forecast called for a 4.8% rise between August 2020 to August 2021.

Historically low levels of for-sale inventory teamed with robust buyer demand and mortgage rates that remain near historic lows should continue to place upward pressure on prices.

2020 home sales likely peaked in September, expected to reaccelerate early next year

Our forecast suggests that closed home sales reached a recent high in September, and will temporarily slow down in coming months, falling to pre-pandemic levels by January 2021. Growth is then expected to resume next spring and to remain firmly above pre-pandemic volume through most of next year.

This short-term deceleration in sales volume can be attributed in large part to an expected slowdown in GDP growth, the fading impact of historically low mortgage rates, fewer sales occurring that were deferred from earlier this year and historically low levels of for-sale inventory. An expected reacceleration of GDP growth in 2021 should help push sales volumes higher.

¹Using the closest daily rates available from theFreddie Mac Primary Mortgage Market Survey. Monthly payments calculated with Zillow's Mortgage Calculator using 20% down payment.

Methodology

The Zillow Weekly Market Reports are a weekly overview of the national and local real estate markets. The reports are compiled by Zillow Economic Research and data is aggregated from public sources and listing data on Zillow.com. New for-sale listings data reflect daily counts using a smoothed, seven-day trailing average. Total for-sale listings, newly pending sales, days to pending and median list price data reflect weekly counts using a smoothed, four-week trailing average. National newly pending sales trends are based upon aggregation of the 38 largest metro areas where historic pending listing data coverage is most statistically reliable, and excludes some metros due to upstream data coverage issues. For more information, visitwww.zillow.com/research/.

Click here to read past editions of Zillow's Weekly Market Report.

Anthony and Charlie Champalimaud have a spiritual side. After the couple bought an 18th-century home in Litchfield, Conn., they hired a self-described energy healer to ensure that they would be welcomed by any previous residents.

The pair bought the five-bedroom, 3,800-square-foot home in the town’s historic district last year. They paid $900,000 for the 4-acre property, which also includes a 2,000-square-foot carriage house and a woodshed.

The healer’s fee was a small splurge of $1,000 following a renovation that cost $150,000. The couple updated the three-level home’s electrical and lighting systems, replastered ceilings, stripped wood paneling and painted.

The work transformed the house into a bright family home with a Scandinavian aesthetic, a nod to the Norwegian heritage of Ms. Champalimaud, 36 years old. Outside, the couple planted trees and are making plans for the carriage house.

“We both grew up in historic houses and like them for their patina, warmth and craft,” says Mr. Champalimaud, 42. “This house feels grounded. It’s not grand, but the scale and proportions are proper and lovely.”

After the renovation, the energy healer performed a ritual using incense, candles and salt to prepare for the home birth of the couple’s daughter, their second child, some three months later. They plan to one day convert their roomy attic into a playroom and two additional bedrooms.

The couple’s home is in the landmark historic district of Litchfield, a quaint New England village set in the hills of Northwest Connecticut about two hours from New York City. The area has many second-home residents.

The pair were living in a farmhouse in the town when they decided to downsize. They were drawn to their current home’s multiple 12 over 12 windows, its fireplaces and its four-room floor plan—unusual when the house was built, according to the Litchfield Historical Society.

The house’s most striking feature may be an original plastered wall decoration of repeating urns and sunbursts in the entrance hall. It was designed to imitate block-print wallpaper.

“It’s a bit faded but has stood up pretty well,” says Mr. Champalimaud.

At the time it was built, the home was one of the grandest in Litchfield, believed to be the work of master carpenter and architect William Sprats. It was commissioned by Dr. Daniel Sheldon, who lived there until his death at age 90 in 1840, after which his daughter moved in.

Behind the home is an original three-seat privy—the only extant example in Litchfield. The 19th-century carriage house has a tack room and stalls. The plan is to restore the first floor and add a climbing wall. The second floor would become a guest apartment.

The entryway has the original painted decoration on the plaster walls.

Julie Bidwell for The Wall Street Journal

The couple is considering buying horses, which are permitted in the town. They also plan to turn a nearby woodshed into a studio.

Mr. Champalimaud, speaking about the finishing touches to the home, said the interior colors are meant to be fun. The living room has rose walls with gray trim, the den is teal with a bold blue nook, and the main bedroom is an ocher that complements the woodwork.

The décor overall reflects the couple’s love of Midcentury Modern furniture mixed with antiques, folk art—including their collection by Winfred Rembert—and contemporary photography. A Saarinen table and Bertoia Diamond chairs are in the dining area. An early Chinese terra-cotta of a boy with a scythe was purchased from a local estate. The living room features an Old Master painting that hung in Mr. Champalimaud’s grandfather’s house in Estoril, Portugal. The home’s unvarnished wide-plank floors are covered with kilims.

The kitchen mixes new and old.

Julie Bidwell for The Wall Street Journal

A stone trough used as a sink is original to the house The owners replaced the kitchen countertops.

Julie Bidwell for The Wall Street Journal

The couple both have extensive experience in historic and cultural preservation. He has developed historic hotels in Europe. She worked for the Nordic World Heritage Foundation in Oslo.

Today, Mr. Champalimaud, a managing partner of The Working Group development company, also is an owner of the historic Troutbeck estate hotel some 30 miles away in Amenia, N.Y.

That estate was built in 1765, then rebuilt in the early 20th century—after a fire—by Joel Spingarn and his artist wife, Amy Einstein Spingarn, both activists for racial equality. Over the decades, Troutbeck was visited by prominent Americans such as Ralph Waldo Emerson, Henry David Thoreau, W.E.B. DuBois and Ida B. Wells, according to Ms. Champalimaud. She currently heads programming at Troutbeck.

Back in Litchfield, another home attributed to a commission by the Sheldon family is for sale. Nearby Sheldon Tavern, built in 1760 and later turned into a 7,242-square-foot private home is on the market for $1.795 million.

A greater share of homes sold above their list price in September (22.4%) than in any month since at least January 2018, another byproduct of incredibly strong buyer demand. That share has grown each month so far this year, pushing well past the typical high point as the market continues to defy seasonal norms.

Homes priced near the typical U.S. home value appear to be the most sought after, with 28.2% of homes in that price quintile selling above list in September.

Compared to last year, the share of homes that sold above list in September doubled in Phoenix, San Diego, Denver, Virginia Beach and Riverside.

More than one-in-five homes sold nationwide in September went for more than the asking price, another example of a seasonal and historical aberration in a year chock full of them — and the latest evidence that sellers have the upper hand in the 2020 housing market.

It is not uncommon for certain homes to generate offers above list price. But the frequency with which homes are selling above list price this year is both historically and seasonally unusual. Of all U.S. homes sold in September, 22.4% went for more than their asking price — roughly 50% higher than both the long-term average (14.5%) and for the month of September in both 2019 and 2018 (around 15% in each year), according to a Zillow analysis of sales and list prices. The data point to robust competition and likely bidding wars over the extremely limited supply of homes for buyers to choose from — a home selling above list on its own does not necessarily mean that home received multiple offers, but it's a very strong indicator.

Typically, July is the month in which the highest share of homes fetch more than their list price, but September 2020's figure was noticeably higher than July of this year (18.2% of homes sold above list), last year (16.1%) and 2018 (17.7%). In a typical year, the market cools in August and September — but the market accelerated into the early fall this year, defying historical seasonal patterns. If most sellers dream of a bidding war pushing their gains beyond their initial expectations, then the evidence suggests that in a year that has otherwise been filled with nightmares, many home sellers' dreams are nevertheless coming true as we approach the end of the year.

Widespread Gains

Gains in the share of homes sold above list were widespread across both geographies and market segments. Sales above list were most common for homes priced just above and below the typical September U.S. home value of $259,906. Homes priced in the second quintile of all U.S. home listings — between $192,001 and $264,000 — sold above list in 28.2% of September sales. Homes in this price range are also selling incredibly quickly — a recentZillow analysis of time on marketfound similarly priced homes typically sold faster than any other price tier in September.

Homes priced between $264,001 and $346,000 nationwide, sold above list price 25.9% of the time in September, up from 16.4% in the previous year. And 21.8% of homes in the move-up segment (priced between $346,001 and $487,000) sold above list in September, up from 13.4% a year ago.

Because progressively fewer buyers can afford homes at higher price points, it is common for the most expensive homes to generate fewer offers above list price. But even in the premium home segment, there is significant evidence of intense buyer competition. Roughly one-in-six (15.7%) of homes in the most-expensive segment (priced higher than $487,001) sold above list in September, up from 10.5% in 2019 and the highest share sold above list in this price range in any month since at least January 2018, the earliest month included in the analysis.

The data also show extraordinary year-over-year changes in buyer behaviors in individual markets that reflect the unprecedented nature of 2020. The share of homes sold above list is up from last month and higher than a year ago in each of the 50 largest U.S. metros, and has more than doubled year-over-year in five of the top 50: Phoenix, San Diego, Denver, Virginia Beach and Riverside. In Phoenix, 27.9% of homes sold above the initial asking price in September, up from 11.8% in the previous year. Market conditions in these markets are clearly markedly different than they were only 12 months ago.

Among the top 50 metros, San Francisco had the highest share of homes that sold above list price in September at 48.9%, up from 43.4% in September 2019. That almost half of buyers were able — if perhaps not entirely "willing" — to pay more than the list price in what has perennially been one of the nation's most-expensive housing markets speaks to the complicated relationship between a number of unique local factors, including: The enduring desirability of the area; the high incomes of many willing to pay the price to live there; and the very limited number of homes available to buy in the first place. It could also indicate that sellers may be underestimating the strength of the local market and pricing too conservatively — or, for some savvy sellers, it could validate the strategy of pricing low on purpose, in hopes of generating competition that will drive the ultimate price up. The Bay Area willcontinue to grapple with huge housing affordability challenges, but its clear that ultra-low mortgage rates are helping local buyers stomach otherwise nosebleed-level prices.

A Sense of Urgency

Perhaps unsurprisingly, homes that soldin the shortest amount of time— indicative of more-intense competition for these properties — also were more likely to sell above list. Nationwide, of homes that sold in 10 days or less, an average of 28.5% sold above list since 2018 . The longer homes stayed on the market, the less likely they were to sell above list — although its not unheard of: Among homes that took 60 days to sell, about 10.4% received an offer above list.

Potential buyers may be feeling urgency tolock in low mortgage rateswhile they last, especially if they sense prices will slip further from reach in coming years. Many others may be taking advantage of newfreedom to telecommutefrom an area where they can more easily afford a home. In either case,the housing market is taking us all back to Economics 101 and teaching lessons about supply and demand. There are simply more prospective buyers than sellers right now, and this imbalance is driving prices higher than we typically see at this time of year. Many buyers in the market right now will need to be realistic about the possibility of bidding wars, and leave themselves financial flexibility by looking at homes listed for less than their maximum price point.

After a brief freeze in activity in the early months of the coronavirus pandemic, the housing market has been scorching hot throughout the summer — but there are signs of an expected seasonal cooldown as we approach the end of the year.Modest drops in both mortgage applications and pending sales indicate that closed sales are likely to recede somewhat in coming months. Still,with tight inventory, low interest rates, and robust demand from households re-evaluating their housing needs, a competitive market is likely here to stay into 2021 — which may mean many listings are likely tofetch their seller a surprising bonus above their initial expectations.

Methodology

The share above list price figures reported in this analysis are computed from a matched data set of final sale prices and first list prices. Share above list price by tiers are computed as the three month trailing average of homes that sold above the list price within each sale price quintile. Sale price quintiles and tiers are computed monthly. National figures are computed as an inventory-weighted average of the state-level share of homes sold above list, which is necessary for computational considerations.

As a wave of urban transplants heads for America’s suburbs and small towns, those areas could find themselves undergoing a dramatic makeover.

The coronavirus pandemic has driven many well-off residents out of the cities, with their overpriced and cramped apartments, and toward less populated areas where they can find more space for less money. People leave cities for the suburbs all the time, but this year’s circumstances are forcing even die-hard urbanites to give up on city living. And many are going to want to re-create some aspects of the cities they left behind in their new hometowns.

President Donald Trump and President-elect Joe Biden battled for the suburban vote in this election cycle. But while those communities were once synonymous with white flight, they have become increasingly diverse in recent years as more immigrants and millennials have moved in. The latest wave of buyers—mostly older millennials, including families, and Gen X couples—is likely to accelerate the pace of change in the suburbs.

“People are already voting with their feet and with their dollars,” says Ed McMahon, a senior fellow at the Urban Land Institute. The nonprofit group researches real estate and land use issues. “The drive-everywhere-for-everything suburb is not going to do as well as those that are walkable and have invested in quality of life, cultural, and recreational amenities. Young people, in particular, want suburbs that give them the best aspects of cities, that have access to parks.”

How will urban transplants change the suburbs?

To the extent that these new residents can’t find their beloved urban amenities in the vicinity of their big house with a yard, they’re going to want to create them. They’ll become involved in local community groups, boards, and planning commissions. They’ll encourage the kinds of businesses they like to open up, and they’ll support the kinds of community initiatives that will create the amenities they want.

“The suburbs are going to change,” says McMahon. “You’re going to see more parks and green space in the suburbs, because people are more interested in running and health-inducing activities. … You’re going to see a lot more housing choices.”

Over the past few years, he’s seen dull office parks reimagined as shared workspaces—with housing, dining, and entertainment in the same complex. Zoning changes could allow more housing to go up in the town’s retail and dining centers. Popular businesses, like food halls and bars offering pingpong tables and video games, could move in.

Experts expect different kinds of housing to rise to meet the growing demand. That could add more affordable options, such as townhouses, duplexes, and condo buildings to towns made up of seas of single-family houses with crisp, green lawns.

“Suburbs in the past had no center, had no edge. You didn’t know where the city ended and the countryside began,” says McMahon.

Forward-thinking suburban communities are building city centers, he adds. “They’re trying to create a sense of place.”

Which suburbs will do the best—and the worst?

The towns that become popular destinations for new residents will likely see higher home values, more tax dollars, and as a result, stronger local economies.

Before the pandemic, urbanites leaving the cities sought out walkable towns with smaller homes, shorter commutes, and lots of places to eat and drink, says Alison Bernstein, founder and president of the Suburban Jungle, which offers advice to people seeking a move to the suburbs.

Today, folks also want to feel like they’re on vacation once they switch off their work computer in their home office. That means having things like public golf courses, hiking and cycling trails, or beaches nearby, Bernstein says.

“A lot of people are going fully remote,” says Bernstein, describing their mindset as “if I can live anywhere, I can get a new-construction house for a quarter of what I’m paying—and I can get a better tax situation.”

She’s seeing many younger families move from the East Coast to Florida, with its lower taxes and cost of living. They’re seeking out towns like Boca Raton and Parkland, as well as homes in Denver and Austin, TX.

These younger, urban buyers care more about the areas they are moving into, and the lifestyle they offer, than the homes they’re purchasing.

“The character of the neighborhood is more important than whether you have granite countertops,” says the Urban Land Institute’s McMahon.

The most successful towns will have unique identities and be adept at leveraging their selling points, such as green space, walkability, and farmers markets, says Brett Schwartz. He is the associate director of the National Association of Development Organizations Research Foundation, an umbrella group of suburban and small-town regional planning commissions.

They’ll also need friendly residents and stable broadband infrastructure, he says. It will be hard to attract professionals working remotely and new business owners to more rural areas with dial-up internet connections and spotty cellphone signals.

“The small towns and suburban communities that are welcoming … are the communities that are going to be able to thrive,” says Schwartz.

The downsides could be overburdened infrastructure, such as more traffic and congested schools. And while rising home prices will be good for homeowners, locals trying to buy their first home could have a tough time.

Will city slickers stay in the burbs—or return to the big cities?

Once there’s a cure for COVID-19, businesses reopen fully, and white-collar professionals feel safe returning to their offices, at least some of these newly minted suburbanites will likely move back to the cities they loved. But the majority are likely to stay right where they are. After all, selling a home after just a couple of years means risking a loss.

“The longer it takes for the world to go back to normal, the more people will stay where they’ve migrated to,” says realtor.com® Chief Economist Danielle Hale. “But I don’t think they’ll necessarily keep everyone.”

Plus, they’re likely to have begun putting roots down in their new communities, says Jason Hickey, president of Hickey & Associates. The New York City–based business helps companies determine where to expand and if they should relocate.

“They would have made the purchase of their home and enrolled their children into the school system,” he says.

However, some of this will hinge on employers. Even workers required to go back to their offices may not have to commute very far. Many companies are looking into opening smaller, satellite offices in the suburbs where their workers are based, says Hickey.

“Right now many people are 100% remote or very close to 100% remote,” says Hale. “If that changes in the future, more people will want to go back to the city and try to minimize their commute.”

The future of local businesses could also affect the trajectory of residents. If restaurants and bars are forced to close because they can’t make ends meet during the pandemic, that will make these communities less desirable.

“People would be less likely to stay if an area loses a lot of things that brought people in in the first place, like local businesses,” says Hale.

Promising results from an early coronavirus vaccine trial sent markets soaring. Treasury yields spiked to their highest levels in months and mortgage rates rose significantly. The Federal Reserve called for more fiscal support in the face of surging virus cases, and hinted at more market easing initiatives.

Pfizer published preliminary data showing its coronavirus vaccine is 90% effective.

Economic growth in sectors most affected by the virus stayed flat.

The virus continues to influence Federal Reserve actions

Last week, the Federal Reserve kept key, benchmark interest rates unchanged.

Fed Chair Jerome Powell pointed out the need for more government stimulus amid rising cases and the waning benefits of earlier relief packages.

Mortgage rates spike on vaccine news

Increased optimism pushed the yield on the 10-year U.S. Treasury to its highest level since March.

Mortgage rates rose strongly as a result, erasing almost all of last week's declines.

So what?

The fate of the economy's recovery depends largely on the evolving path of the pandemic, and our ability to handle it — and markets soared today on promising, if early, signs of progress towards an eventual vaccine. Economic activity has improved from springtime lows, aided initially by unprecedented government support that has since expired. But high-frequency indicators suggest that the virus has and will continue to constrain activity and optimism.In the week ending October 25, levels of consumer spending were 3.9% below January, and the pace of improvement has stalled since early September. Even as some parts of the economy show real signs of progress, there are clearly portions that cannot recover until the virus has been corralled: Entertainment spending is down 54.8% from January; spending at restaurants and hotels is down 29.1%. At the end of September, the number of small businesses in the leisure and hospitality sector was 36.9% less than at the beginning of the year.So even as much of the world remains firmly in the grips of a devastating uptick in cases over the last several weeks, today's news was a shot in the arm for hopes of an eventual return to normalcy.

The worsening virus surge was a key theme in statements made at the most-recent meeting of the Federal Reserve's Federal Open Market Committee.Fed Chair Jerome Powell emphasized the fragility of U.S. households' budgets and the risks to the economic recovery posed by the coronavirus' accelerating spread, particularly if no additional fiscal support is passed in Congress. As expected, the Fed kept key interest rates near zero, and Powell hinted that the central bank could adjust or increase its pace of asset purchases should the economy's recovery continue to slow.An uptick in asset purchases would likely place more downward pressure on bond yields, and thus mortgage rates.

Today's encouraging vaccine news and more certainty surrounding the outcome of U.S. elections combined to push bond yields strongly upward, and mortgage rates followed suit. The yield on the 10-year Treasury bond briefly touched its highest level since March, before retreating slightly near the end of the trading session.The yield curve of U.S. government bonds grew to its steepest shape since February 2018, an indication of quickly-growing optimism and appetite for risk in financial markets. Mortgage rates didn't move by quite as much, but did rise and essentially erase all of the declines (or improvements) made last week in the immediate wake of the election.Even so, mortgage rates in general remain very low, and the recent weakening of their long standing relationship with Treasury yields suggests that any upward movements will be muted compared to those of Treasury yields. But today's market behavior was a reminder that mortgage markets are certainly not immune to coronavirus-related developments.

Click here to read past editions of Zillow’s Market Pulse updates.

Who’s buying homes, who’s selling them, and what types of homes are inspiring bidding wars all look a little different this year as the country remains in the throes of the coronavirus pandemic.

Those who managed to nail a home purchase after the COVID-19 pandemic began spreading through the United States were more likely to pay dearly for larger, more expensive homes in the suburbs, according to the National Association of Realtors® 2020 Profile of Home Buyers and Sellers. The annual report breaks down the characteristics of buyers, sellers, and the homes they bought and sold. It was based on responses from more than 8,200 buyers and sellers who completed their transactions between July 2019 and June 2020.

“Buyers who are out there have a higher income and are financially secure and need to find a house that will work for their family,” says Jessica Lautz, NAR’s vice president of research.

And prices just keep going up and up. Buyers paid more for these homes—a median $339,400 since April, compared with $270,000 before the crisis, as prices climbed as a result of competition flooding a market with a stark lack of inventory.

That’s a nearly 27% increase in just a few short months.

The throngs of buyers lured by record-low mortgage interest rates and the need for more space (home office anyone?) have led to a surge in offers over asking price, bidding wars, and homes selling within days of being listed, or sometimes hours.

About 57% of these buyers closed in the suburbs, up from 50% last year. However, urban sales also ticked up slightly from 12% to 14% as the pandemic dragged on.

“Some of this is normal; it happens every year,” says realtor.com Chief Economist Danielle Hale. “We do know that spring and summer buyers tend to be families who purchase larger, more expensive homes.

“But some of it could be driven by the pandemic,” adds Hale.

Today’s buyers haven’t been as affected by the downturn brought on by the coronavirus and have held onto their jobs, despite the worst unemployment since the Great Depression. (Unemployment has been highest among customer-facing workers, such as lower-paid restaurant, retail, and other employees who can’t work remotely.) Those who bought in April and after had median household incomes of $100,800 compared with a median $94,400 for those who closed before the crisis.

“People who are in the market right now who have kept their jobs and have relatively steady income, so have been able to take advantage of low mortgage rates,” says Hale. Rates fell to an all-time low of 2.78% for a 30-year fixed-rate mortgage in the week ending Nov. 5, according to Freddie Mac.

Pandemic buyers don’t expect to stay in their homes as long as those who bought before the public health crisis. They plan to be in their new homes for 10 years, compared with 15 years.

“People are saying, ‘I just need to find a home that’s right for me right now. Perhaps after the pandemic, I’ll continue living here or find a new place,'” says Lautz.

They also tend to be a bit more family-focused than they were before the deadly virus. They’re more likely to buy a multigenerational home for themselves and their aging parents, grown children, or grandchildren—or all of the above. About 15% of buyers purchased such homes in April and afterward versus 11% before the pandemic.

“They need to find a home that will have enough room for all of these adults who suddenly are living together,” says Lautz. “It’s to take care of and spend more time with an elderly parent. Adult children may also be back at home with their families.”

Fewer first-time buyers became homeowners this year

Overall, the number of successful first-time home buyers fell this year as the pandemic and the struggling economy took their toll. That could be because these buyers, who tend to be younger and make less money, may have been hurt more by the recession.

First-time buyers, a median33 years old, made up about 31% of sales. That was down a little from 33% last year and is the lowest it’s been since 1987, when they made up 30% of the share.

“Even with low interest rates, it’s hard to find an affordable home with the lack of housing available,” says Lautz.

This group had an $80,000 median household income, lower than repeat buyers at $106,700. They also had lower down payments, of a median 7%. That’s because they earned less, were contending with student loan debt, and didn’t get as much family help. The median down payment for all buyers was 12% of the purchase price.

Just over a quarter, 26%, of these buyers received financial help from their families on their home purchase—compared with 33% last year. Student loans were the biggest obstacle for saving up for a down payment. Buyers typically carry about $30,000 in student loan debt.

That’s why the homes they purchased were more affordable than those bought by repeat buyers. First-time buyers spent a median $230,000—about 18% less than the median $272,500 price of all homes sold.

“Younger buyers, first-time buyers are less established and have to make sacrifices,” says Hale. “It is a challenge buying a home.”

Not surprisingly, their homes tended to be smaller, at a median 1,680 square feet. That’s a little more than 200 square feet in difference from buyers overall.

Repeat buyers were a median 55 years old and bought 2,020-square-foot homes for a median $297,000.

Overall, the typical buyer this year is middle-aged, is coupled up, and makes good money. These folks are a median47 years old and have a $96,500 median household income.

Buyers were also overwhelmingly white, making up about 83% of those who purchased homes. Hispanics made up about 7%, followed by Asians and Blacks, both at 5%.

“It is not just a reflection of the makeup of the country, but also a reflection of how income and wealth are spread out among different racial groups,” says Hale.

Sellers made more money during the pandemic

Homeowners who sold their properties during the pandemic were more likely to cash in as prices spiked nationally. Those who sold after March scored a median $300,000 for their residences. That’s nearly $30,000 more than those who sold before the virus for a median $270,700.

Pandemic sellers were more likely to put their homes up for sale because they felt they were too small. About 18% did so after the March lockdowns, compared with 13% who sold their abodes before March.

“Sellers have more urgency to find a place that fits their family’s needs during the pandemic,” says Lautz.

Sellers tended to be older, a median 56 years old, and wealthier than buyers with median household incomes of $107,100. They lived in their homes for about a decade before putting them onto the market.

Their homes sold in about three weeks for 99% of the final list price. They made a median $66,000 on their sales compared with what they had originally paid for their properties.

The hottest housing in 2020

As folks increasingly sought out additional square footage and the ability to better socially distance, detached, single-family homes remained the top type of housing purchased this year. That makes sense as folks forced to work and school their children from home sought out larger spaces, home offices, and bigger backyards to safely socialize in.

The typical home bought this year was a three-bedroom, two-bathroom with approximately 1,900 square feet. Homes sold were a median 27 years old.

“People are seeking more space either to home-school or work remotely or have more personal space,” says Lautz.

Overall, homes sold for a median $272,500. Buyers purchased properties a median 15 miles away.

“Larger, more suburban homes were a trend that existed even before the pandemic,” says Hale. “Of course, we’ve seen that trend accelerate due to the havoc the coronavirus has wreaked on all aspects of life.”

The U.S. labor market improved in October from September, and unlike the month before, appeared to do so for the right reasons. But problems persist: measures of persistent job loss remain elevated and more than half the jobs lost in the Spring have not been recovered.

The job market continued its gradual recovery in October…

The U.S. economy added 638,000 jobs in October.

The headline unemployment rate fell to 6.9%, down a full percentage point from September.

…But, like before, signs of stress persist…

A third of all people unemployed but in the labor force have been jobless for at least 27 weeks.

Alternative measures of persistent unemployment have barely improved and remain near pandemic highs.

…And the path forward remains uncertain.

The labor market is still down almost 12 million jobs from where it would be had the pandemic not occurred.

55% of the jobs lost in March and April have not returned.

So what?

The October jobs report offered both encouraging and discouraging signals for the U.S. labor market. The U.S. economy added 638,000 jobs in October from September, a figure that would have been larger without the removal of about 150,000 temporary Census jobs.The headline unemployment rate dropped a full percentage point, to 6.9%, and unlike September's report, the decline in overall unemployment appears to have occurred for healthy reasons. Both the labor force participation rate and the share of people who are employed both increased from September, as did the overall size of the labor force.All three of these metrics remain well below their pre-pandemic levels, but after September's weak showing, October's improvements could indicate that people are gaining confidence in their ability to find employment.

But it's critical not to overlook signs of weakness, too — particularly the fact that joblessness is becoming increasingly permanent. While temporary job losses declined, continuing a trend that has been playing out for months, measures of persistent or permanent unemployment barely improved in September and remain near their highest pandemic-era levels.There were 3.6 million "long-term" unemployed people — those out of work for 27 weeks or longer – in October, up about 46% from September and representing 33% of all people currently unemployed but still in the labor force.Given the still-elevated level of jobless claims and ongoing spread of the coronavirus, an increase in this metric isn't a surprise, but it also reinforces a key challenge that the labor force will face going forward. Generally, the longer people are out of work, the harder it is for them to reconnect with their old employer and, more broadly, to find work even when jobs become available.

As expected, job growth has slowed markedly in the past few months and more than half (55%) of the jobs lost in March and April have failed to return.Assuming the same level of job growth as before the pandemic had continued, estimates suggest that the labor market is still down about 11.7 million jobs compared to where it would have been had the pandemic not occurred. What's more, the report fails to account for the 7 million workers who remain employed but have seen their hours or wages cut in recent months. Meanwhile, jobless claims remain elevated – more than a million people filed for initial jobless claims last week.The outlook for the job market depends most of all on the path of the coronavirus and the potential for additional federal, fiscal relief. Today's report showed that state and local governments — suffering huge losses in revenues because of the pandemic — cut 130,000 jobs in October, and will continue to contract without additional relief.

Click here to read past editions of Zillow’s Market Pulse updates.

Big-city life has always been a major trade-off: the amazing job opportunities, cultural resources, and endless options for dining and nightlife weighed against cumulous-scraping prices for homes with a tiny footprint. Looming large over the equation has been the common goal of keeping work commutes as short and easy as possible. But the coronavirus pandemic of 2020 turned all that upside down. Suddenly plenty of office workers (and their employers) have made a startling discovery: They can do their jobs just as well remotely! So, it stands to reason, why not do it somewhere cheaper?

After spending seemingly endless months of Zooming from the bedroom, schooling in the living room, and lingering in the bathroom for a few precious extra moments of privacy, many families have been packing up their urban cubbyholes in favor of large homes out in the country or the ‘burbs.

According to the Pew Research Center, even back in June, at least 1 in 5 adults had moved, or knew someone who had moved, due to the pandemic.

If employers let their workers go remote permanently, suddenly folks could go anywhere—anywhere that has a decent internet connection and good living conditions, that is. So where are the best places for folks to escape the biggest, priciest cities? The industrious data team at realtor.com® (working remotely, of course) is here to help!

We focused on more affordable metropolitan areas, all but one with home list prices under the national $350,000 median. They offer the magical combo of low home prices and reasonable cost of living as well as fast-speed internet so folks don’t uncomfortably freeze in their work meetings. We also made sure these metros have plenty of businesses and fun/interesting places to explore when the pandemic ends. Because it will end. (Metros include the main city and surrounding smaller towns, urban areas, and suburbs.)

“With so much more time spent at home, there’s more urgency to try to address a fit that’s not quite right,” says Danielle Hale, chief economist for realtor.com®. “People’s priorities and needs have shifted as a result of changes in the way we live now.”

To come up with the best places to telecommute, we scoured the 100 largest metros for the ones with access to high-speed internet (at least 250 Mbps), affordable home prices, and a low cost of living. The data came from realtor.com, the Federal Communications Commission, the U.S. Census Bureau, and the St. Louis Federal Reserve.

Only one metro per state was included to ensure geographic diversity.

Ready to peruse the greener grasses? Let’s check out the best places to work remotely during the COVID-19 pandemic—and beyond!

The ‘Cuse might be cold as hell come wintertime, but what it lacks in sunny warmth it makes up for in space, affordability, and connectivity. Verizon’s high-speed Fios is available throughout much of the city, and the company launched what it claims is the fastest 5G network in the world just last month.

Buyers who want to settle down in this college town can easily find a nice home with room for an office and some outdoor space, including this small four-bedroom listed for just $104,900. However, in the COVID-19 era, many of the new residents who have been flocking to Syracuse from pricey downstate (the New York City metro area) have been opting for even more space outside the city proper, into the suburbs and surrounding rural ZIP codes with slightly slower web speed. Like everything else, it’s a trade-off.

For less than the cost of a Manhattan studio, buyers have been snatching up sprawling properties just a 20-minute drive from downtown, including this large three-bedroom on nearly 3.5 acres for $689,900 or this four-bedroom on more than an acre for just $199,900.

“In greater Onondaga County we have a lot of access to high-speed internet and whatnot,” says Sarah Barrows, a licensed real estate salesperson with Keller Williams Realty Syracuse. “We’ve enabled a lot of people to work from home.”

Cleveland may have the Browns, Indians, Monsters, and Cavaliers—heck, it even had LeBron!—but Akron has high-speed internet. A whopping 98.95% of its residents have access to broadband, which makes it a better place to work from home. (But if you’re watching a game on your big screen, does it really matter how close you are?)

The well-connected metro offers home seekers plenty of room to roam. The northern part of the city is full of beautiful parks, including a national park. So those looking for easy access to nature need not travel far at the end of the workday and school day from places like this three-bedroom ranch for $225,000 or this three-bedroom on an acre lot right on the perimeter of Cuyahoga Valley National Park for $238,400.

Scranton and greater Northeastern Pennsylvania already had a scorching-hot home market before the pandemic due to its growing population and burgeoning jobs market. Earlier this spring—at the height of the state’s COVID-19 shutdown—new listings plummeted by 78%, the third-steepest decrease in the nation. New listings are up now, but they are still flying off the multiple listing service.

A surge of new residents fleeing pricey metros like New York City has driven up prices throughout Lehigh Valley—but they’re still far cheaper than in the big cities. Some home buyers, lured to Electric City by Scranton Mayor Paige Gebhardt Cognetti’s “Work From Here” initiative this summer, put in offers without even stepping foot on the property.

It sounds crazy, but the $359,000 that can’t even buy a shoebox in Manhattan can get a historic five-bedroom home on 1.5 acres in Scranton’s stunning East Mountain or a cute three-bedroom with a covered porch for just $205,000.

While many restaurants have been struggling with takeout and reduced capacity, pizzerias have been one of the few winners of the pandemic. Talk about comfort at home. Why not cut living expenses while picking up some of the best pies in the United States to eat in your sprawling abode?

New Haven’s renowned clam pizzas (try ’em!) may not be the reason Big Apple residents have been relocating to Elm City in droves—but they certainly don’t hurt matters. The city and its surrounding ZIP codes have received an influx of New Yorkers packing up their apartments for spacious single-family homes near the shore. Homes such as this three-bedroom in Historic City Point listed for $205,000 and this West Haven five-bedroom Colonial Cape for just $199,500 have been in high demand all summer.

“If they’re trading the New York City lifestyle, most buyers want a different lifestyle near the water,” says Regina Sauer, a Realtor® with Frank D’Ostilio Real Living Milford. “And they definitely want a lot of space to work from home and teach children from home.”

Due to skyrocketing COVID-19 cases and their corresponding pressure on the local medical system, El Paso County is currently in the midst of another shutdown. But the city is still considered one of the best places to work remotely in terms of affordability, internet speed—nearly 97% of the population has access to broadband—and weather. Daytime highs in the winter range from the high 50s to low 60s, making it easy to socially distance outdoors year-round when your northern brethren are stuck inside.

Just northwest of downtown, buyers can take advantage of the sunshine from the comfort of their backyard pool, starting in the mid-$200,000s, like this four-bedroom with a den listed for $270,000 and this four-bedroom with two living areas for just $247,500. With those kinds of setups, why would you even want to leave the house?

Even before the pandemic prompted many urbanites to rethink the skyscraper-high rents and home prices in places like New York City and San Francisco, there were plenty of folks decamping for New Orleans. The walkable city has just as much culture and even better food (and drink) than most major metros for a tiny fraction of the price.

In centrally located, desirable neighborhoods, the competition for homes is tough, though. The average single-family home price across the metro has risen by more than 6% from the same time period last year. But buyers can still find lovely homes in those sorts of neighborhoods for a whole lot less than in equally attractive burgs around the country.

This charming Mid-City three-bedroom, within walking distance to City Park, is listed for $335,000, and this nearby three-bedroom Arts and Crafts bungalow with covered porch and tree-covered yard is asking $395,000.

The suburbs surrounding Milwaukee have experienced a swell of new homeowners since the start of the pandemic. City dwellers from both the Cream City and nearby Chicago have been getting into bidding wars over spacious homes close to downtown in areas like New Berlin and Wauwatosa.

You remember this was one of the battleground states, right? In conservative New Berlin, buyers have been seeking out houses with grassy lawns, including this three-bedroom with a finished basement (office anyone?) for $259,000. In Democrat-leaning Wauwatosa, homes are generally a bit more expensive, but buyers can still find deals that are far more affordable than in similar neighborhoods, including this sprawling four-bedroom that could use a few updates for $264,900.

Regardless of which way they lean politically, many of these folks have been prompted to seek a change of scene due to the pandemic.

“We’re seeing this dynamic of younger people moving to suburbs because they don’t want to be on lockdown,” says Michael Borowski, owner/broker of Homestead Realty. “People are moving outside of the city because of COVID, and employers are not requiring them to come back to their physical workplace anymore.”

Rhode Island is so tiny, the Providence metropolitan statistical area encompasses the entire state plus Southeastern Massachusetts. And the whole metro area is seeing a massive influx of people relocating from cities like New York and Boston, says Amanda Nickerson Toste, broker associate and partner at Sakonnet Homes.

“The hotter markets are in the rural areas,” she notes.

However, the internet in rural Rhode Island has been struggling to meet the demand of all the people needing Zoom or Google Hangouts for school and work. To get the best connections, buyers need to look toward Providence and its nearby suburbs. Barrington, for example, is known for its great schools (and correspondingly high taxes and home prices), proximity to downtown, and safe, rural vibe with high-speed internet.

There, it’s possible to get into a home with an office starting in the high-300,000s, including this historic three-bedroom listed for $384,900 and this three-bedroom Cape Cod on an acre for just $379,000.

U.S. News and World Report recently ranked this Midwestern metro at No. 5 on its Best Places to Live list, and it certainly has a lot going for it. It’s home to nearly 60 company headquarters, numerous parks, and interconnected bike trails. Pre-pandemic, the recently revitalized downtown was a lovely place to dine out, and it surely will be postpandemic, too. And more than 90% of its population has access to ultrafast internet.

As is the case with most metros these days, many young families who are working remotely are looking for deals on homes with extra space inside and out. About 20 minutes southwest of Des Moines, and just a 10-minute drive from Blank Park Zoo, the suburb of Norwalk has been seeing a ton of young parents due to its affordable price points and higher-performing schools for the past few years—and that trend has continued through the pandemic.

The walkable town offers first-time buyers a chance to get into large homes starting in the $200,000 range, including this three-bedroom with an office and deck for $249,000 and this four-bedroom with a decked-out yard listed at $269,000.

While St. Louis is justly famed for its iconic Gateway Arch, it also boasts 700 life science and agriculture technology firms, a thriving startup scene, 45 colleges and universities, nationally acclaimed restaurants, and one of the best zoos in the county. And it’s also one of the 25 most affordable cities in the United States, with a standard of living higher than 95% of other cities, says Luan Meredith, broker/owner of Realty and Associates.

After years of downtown revitalization, the suburbs surrounding the city have been seeing a surge of new residents this year, with many young families looking for fully renovated homes with separate spaces for spouses to work and kids to study. Even in highly desirable neighborhoods with coveted school districts, like Kirkwood, buyers can find great deals, including this convertible three-bedroom with a loft for $339,000 and this cute two-bedroom with recently finished extra spaces for $260,000. That extra square footage and new renovations are exactly what St. Louis buyers have been snatching up in droves.

“Now they all want a bigger house, or better house, or newer house,” says Meredith. “It’s the younger generation that’s growing and moving up.”

* Median home list prices are from October using the most recent realtor.com data available.