Thursday, February 28, 2019

$57M NYC Penthouse With Private Rooftop Pool Is This Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Castles for Sale in USA That Look Like They Were Plucked Out of an Irish Fairy Tale

Picture this: An old stone castle, perched on a hillside and casting a dark and looming shadow over the landscape below. A moat surrounds said structure, and like a looking...

The post Castles for Sale in USA That Look Like They Were Plucked Out of an Irish Fairy Tale appeared first on RE: Find.

from Castles for Sale in USA That Look Like They Were Plucked Out of an Irish Fairy Talehttps://https://ift.tt/2Tmkoz6

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

As Empty Luxury Rental Apartments Pile Up, So Do Offers That May Be Too Good to Be True

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, February 27, 2019

Polar Vortex, Shutdown Should Temper Mortgage Rate Response to January Data

For the third week in a row, mortgage rates ended the week roughly where they began it. Rates continue to hover near their lowest levels since March 2018, providing a boost to home buyers just as inventory is starting to rise nationwide.

Over the coming week, all eyes will be on several Fed speakers as markets continue to try and grapple with a shifting monetary policy outlook. Wednesday's release of the minutes from the Federal Open Market Committee's January meeting provided more details about how the Fed plans to manage its legacy recession-era bond portfolio, and made explicit that the committee is monitoring incoming data for how last year's interest rate hikes have spilled over into the broader economy.

This week also will see the release of January housing market data. The housing sector was a soft spot for the economy late last year, in part because of rising interest rates. But interest rates are down and inventory is up in the first two months of 2019 – which should provide more stimulus to the sector. However, it would be a big leap to read too much into the January data. While inventory and interest rates provided a boost, the partial federal government shutdown and the polar vortex that hit much of the country mid-month likely weighed on housing activity.

The post Polar Vortex, Shutdown Should Temper Mortgage Rate Response to January Data appeared first on Zillow Research.

via Polar Vortex, Shutdown Should Temper Mortgage Rate Response to January Data

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Why Hasn’t Anyone Bought Eleanor Roosevelt’s Former Townhouse in NYC?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Most popular homes and their neighborhoods of February 2019

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, February 26, 2019

Creating a Home(work) Station That Gets Top Marks

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

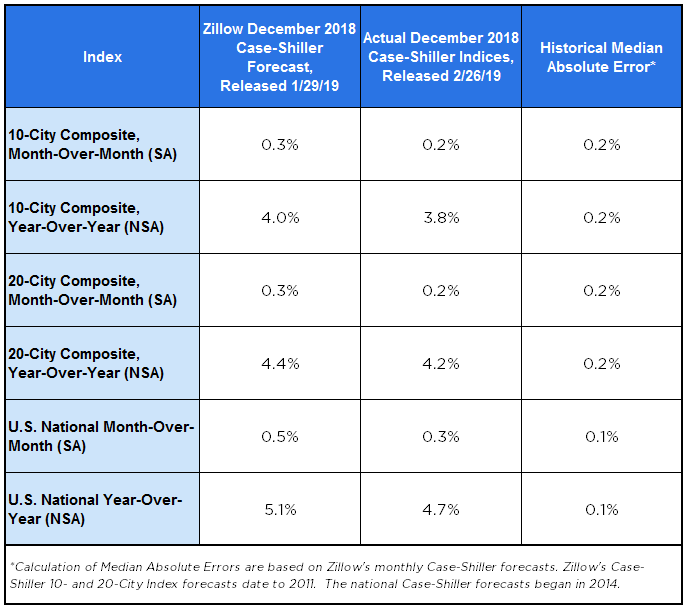

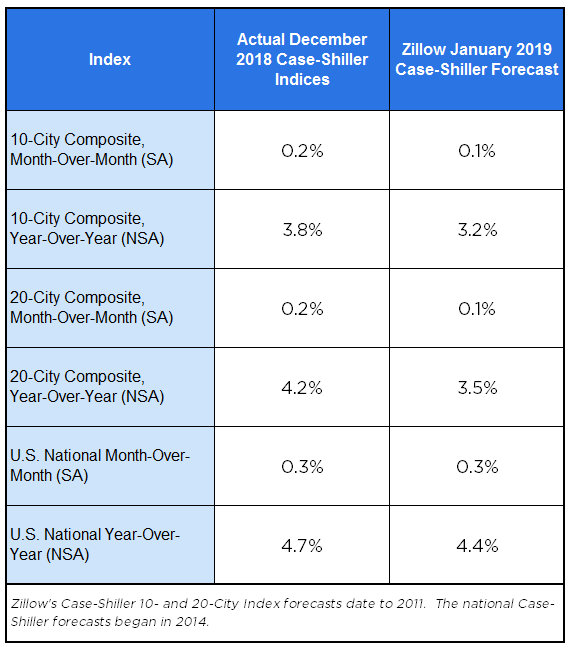

December Case-Shiller Results and January Forecast: Slowing home price gains

For years, the housing market has been anything but "normal" or "balanced." But as the start of the busy home shopping season looms, someone squinting at the market might be able to find signs of both normalcy and balance as the market continues to cool off after a years-long sizzle.

Annual home price growth, while still rapid in a handful of the most in-demand and/or affordable markets, has fallen to a pace not far off historic norms and feels largely sustainable for now at a national level of 4.7 percent year-over-year in December. That pace is down from 5.1 percent in November, according to the Case-Shiller home price index.

Las Vegas once again led the way, with an 11.4 percent annual gain, followed by Phoenix at 8 percent and Atlanta at 5.9 percent.

Additional headwinds were reported by the Census Bureau today, which said housing starts fell 11.2 percent in December from November.

Inventory is certainly not "back," but modest gains are being made month-after-month, and buyers are likely to have more choice this spring than they have in years. Mortgage interest rates have stabilized below recent peaks and look set to remain in their current range near historic lows for the time being, a boon to buyers' budgets.

On their own, none of these small shifts would be likely to move the needle much in terms of rebalancing the buyer/seller dynamic, but taken together, they represent a meaningful swing in buyers' favor – just in time for spring.

The post December Case-Shiller Results and January Forecast: Slowing home price gains appeared first on Zillow Research.

via December Case-Shiller Results and January Forecast: Slowing home price gains

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Places That Have—and Have Not—Recovered the Most Since the Housing Bust

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

December Housing Starts: Clear Declines, But an Incomplete Picture

- December housing starts fell 11.2 percent from November and 10.9 percent from a year ago, to just over 1 million units (SAAR) according to the Census Bureau. Starts were down most sharply in the inventory-starved West.

- Single family starts down 6.7 percent from November; multifamily starts were down 22 percent month-over-month. December was the weakest month for single-family housing starts since August 2016.

- Housing permits rose 0.3 percent from November and 0.5 percent from December 2017.

- National housing completions fell 2.7 percent from November and 8.4 percent percent from December 2017.

With two months’ hindsight, there were obvious headwinds to the housing market late last year that have since eased. High interest rates, a stock market freefall and the partial government shutdown translated into a drag on the housing market. Most housing market metrics – including starts and permits – now reflect the fallout from the fourth-quarter economic turmoil.

But December now feels like a lifetime ago – especially in the housing market. Mortgage rates are down from seven-year highs to 12-month lows, and the interest rate outlook is less ambitious with the Federal Reserve pausing hikes until they get more data on the state of the economy.

While homeowners can move quickly to list a home for sale or pull it off the market when the market shifts, builders have a slower, wider turn radius in reacting to interest rates and other market factors. As a result, builders will be less agile at reacting to the shifting economic outlook. However, the stronger market conditions in early 2019 mean than home builders have been able to offload inventory that had been piling up late last year.

Today's data should have been released several weeks ago, but were delayed as a result of the partial government shutdown. Delayed economic data releases have clouded our read on the state of the economy – a lasting effect of January's political brinkmanship.

The post December Housing Starts: Clear Declines, But an Incomplete Picture appeared first on Zillow Research.

via December Housing Starts: Clear Declines, But an Incomplete Picture

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

10 Homes Priced Below $100K Prove Homeownership Isn’t Out of Reach

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

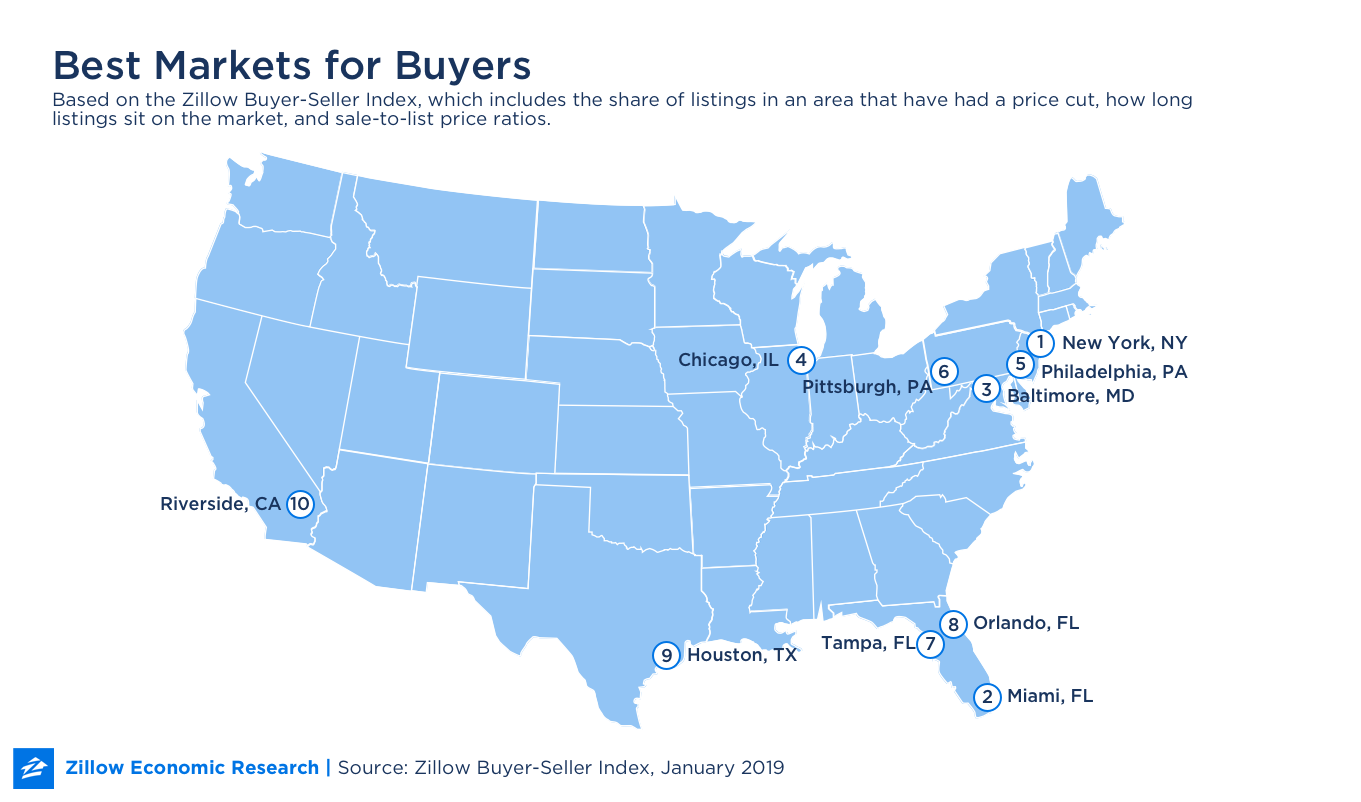

Best Markets for Home Buyers Led by New York, Florida

Of the 10 metro areas that have the best conditions for buyers as home-shopping season approaches, three are in Florida – Miami, Tampa and Orlando – but the best market overall for buyers is New York, according to the Zillow Buyer-Seller Index.

It's not that New York is all that affordable: Its median home value in January was $438,300, almost double the U.S. median of $225,300. But other aspects of the New York market are a boon to buyers who can afford it. For example, among the largest 35 metros, it has the longest number of days on the market, at 132 days. The next longest time on market is 102 days in Chicago. It's followed by Miami, at 99 days.

Two other Florida metros – Tampa and Orlando – rank in the top five for the share of listings with a price cut, a pro-buyer characteristic. In Tampa, 23.2 percent of listings received a price cut in January. In Orlando, it was 20.4 percent.

The third metric in the buyer-seller index is the sale-to-list-price ratio. A ratio above 100 percent indicates that buyers are paying more than list price. The further the ratio falls below 100 percent, the better the market is for buyers – because they're paying that much less than list, which would be 100 percent even. The lowest ratios among the largest metros are Pittsburgh, at 93.7 percent, Miami at 93.9 percent and Chicago at 94.2 percent.

We've also published a list of best markets for sellers.

| Rank | Metro area | % listings with price cut | Median days on market | Sale-to-list-price ratio (%) | Median home value |

|---|---|---|---|---|---|

| 1 | New York, NY | 14.6% | 132 | 95.7% | $438,300 |

| 2 | Miami-Fort Lauderdale, FL | 16.7% | 99 | 93.9% | $283,800 |

| 3 | Baltimore, MD | 19.2% | 97 | 96.4% | $267,900 |

| 4 | Chicago, IL | 18.2% | 102 | 94.2% | $224,800 |

| 5 | Philadelphia, PA | 17.9% | 90 | 95.7% | $232,700 |

| 6 | Pittsburgh, PA | 16.8% | 87 | 93.7% | $143,900 |

| 7 | Tampa, FL | 23.2% | 75 | 95.6% | $213,600 |

| 8 | Orlando, FL | 20.4% | 84 | 95.8% | $237,100 |

| 9 | Houston, TX | 19.4% | 89 | 94.8% | $205,500 |

| 10 | Riverside, CA | 17.5% | 83 | 96.7% | $367,100 |

| United States | 15.8% | 83 | 96.2% | $225,300 |

The post Best Markets for Home Buyers Led by New York, Florida appeared first on Zillow Research.

via Best Markets for Home Buyers Led by New York, Florida

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

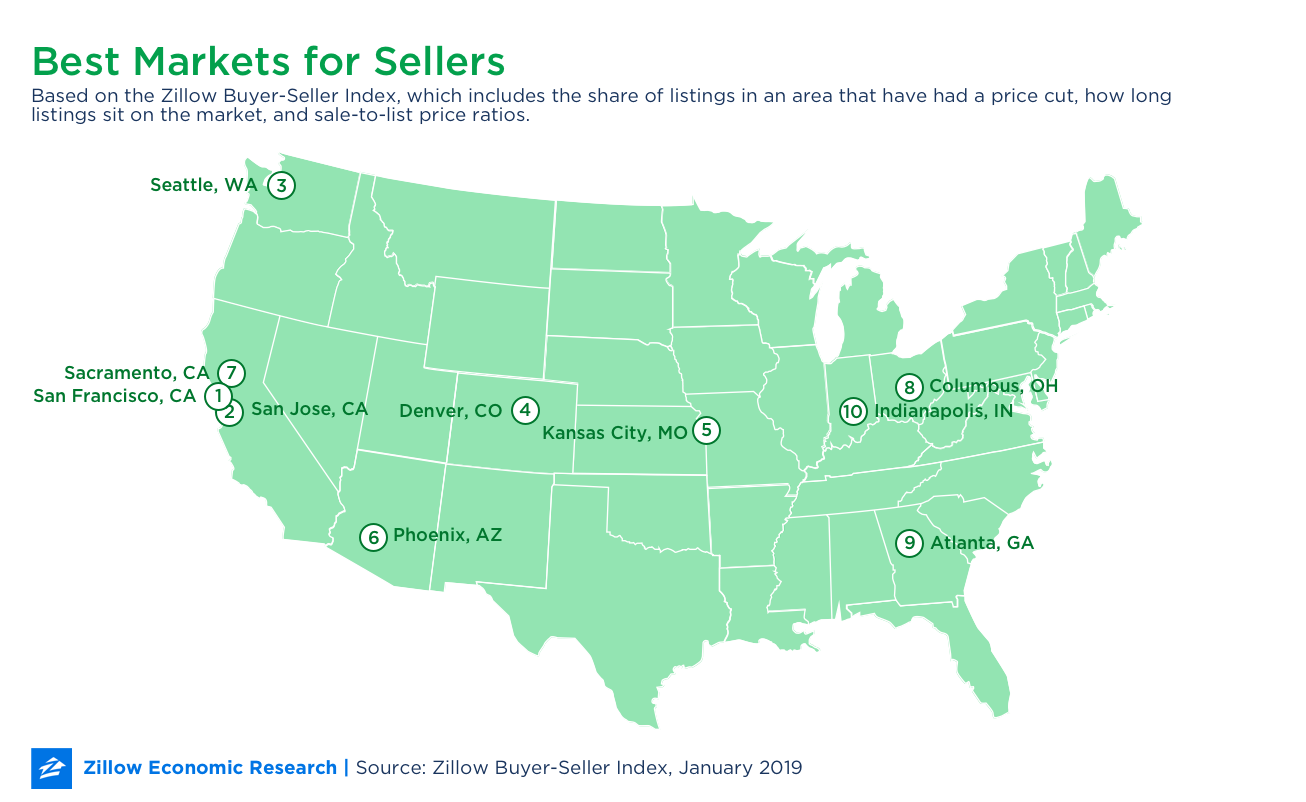

Tech Metros Lead List of Best Markets for Home Sellers

As home selling season approaches, tech hubs San Francisco, San Jose, Calif., and Seattle lead the list of metro areas that are poised to be the best for sellers.

These are also three of the priciest markets in the country, which can be attractive for sellers, depending on how much they paid for their homes and how long they've owned them.

In San Francisco, the best market for sellers overall, the median home value is $957,400. In San Jose, it's $1.25 million.

But home values (also reflected in prices) are not what makes these the best metros for sellers. The Zillow Buyer-Seller Index uses three metrics that capture market trends and are a robust measure of buyer/seller dynamics. The metrics are: what share of listings in an area have had a price cut, how long listings sit on the market, and sale-to-list price ratios.

Among the country's largest 35 metro areas, San Francisco had the smallest share of price cuts in January, at 11.5 percent. It also had the shortest median number of days on the market, at 57 days for homes sold in December, the most recent month for which data are available. And its sale-to-list-price ratio, which gauges whether sellers are getting their asking prices at sale, is the second-highest, with sellers getting 98.6 percent of their asking prices, at the median.

We've also published a list of the best markets for buyers.

| Rank | Metro area | % listings with price cut | Median days on market | Sale-to-list-price ratio (%) | Median home value |

|---|---|---|---|---|---|

| 1 | San Francisco, CA | 11.5% | 57 | 98.6% | $957,400 |

| 2 | San Jose, CA | 15.3% | 61 | 97.2% | $1,245,800 |

| 3 | Seattle, WA | 15.2% | 77 | 96.6% | $489,700 |

| 4 | Denver, CO | 18.1% | 65 | 97.2% | $405,300 |

| 5 | Kansas City, MO | 14.5% | 66 | 98.2% | $191,600 |

| 6 | Phoenix, AZ | 19.2% | 61 | 97.4% | $264,900 |

| 7 | Sacramento, CA | 17.3% | 67 | 96.9% | $408,700 |

| 8 | Columbus, OH | 16.5% | 71 | 96.6% | $189,900 |

| 9 | Atlanta, GA | 16.1% | 77 | 97% | $217,500 |

| 10 | Indianapolis, IN | 17.9% | 70 | 97% | $163,900 |

| United States | 15.8% | 83 | 96.2% | $225,300 |

The post Tech Metros Lead List of Best Markets for Home Sellers appeared first on Zillow Research.

via Tech Metros Lead List of Best Markets for Home Sellers

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, February 25, 2019

Chip and Joanna Gaines Buy a Castle That Could Do Them In—These Pics Reveal Why

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

A New Concierge Service Wants to Make Sure Your Nasty Breakup Goes Smoothly

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

3 Reasons to Use an HSA to Save for Retirement

Could this be the best thing since the 401(k)?

The post 3 Reasons to Use an HSA to Save for Retirement appeared first on RE: Find.

from 3 Reasons to Use an HSA to Save for Retirementhttps://https://ift.tt/2ExTxYN

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Most Expensive Neighborhood in Every State in America

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, February 22, 2019

3 Things We Love About the 2019 New American Home—and 3 We Could Live Without

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Millennials Are Hiring Consultants to Raise Their ‘Plant Babies’

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

2019’s Top Must-Have Home Features and Interior Design Trends

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Heads Up! Scary Hunting Lodge Home Shoots to Top Spot of Most Popular Listings

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, February 21, 2019

Roofing a House: 3 Easiest Roof Types to Install

A simple gable roof is best for DIY.

The post Roofing a House: 3 Easiest Roof Types to Install appeared first on RE: Find.

from Roofing a House: 3 Easiest Roof Types to Installhttps://https://ift.tt/2X9K3tQ

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

How to Set Up a Will Online (and Why You Need One)

Don't leave prized possessions in the hands of strangers.

The post How to Set Up a Will Online (and Why You Need One) appeared first on RE: Find.

from How to Set Up a Will Online (and Why You Need One)https://ift.tt/2BLvLqr

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

$110M Santa Barbara County Ranch Is the Week’s Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Mortgage Rates Fall to One-Year Low, Setting the Stage for a Sunny Spring Selling Season

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

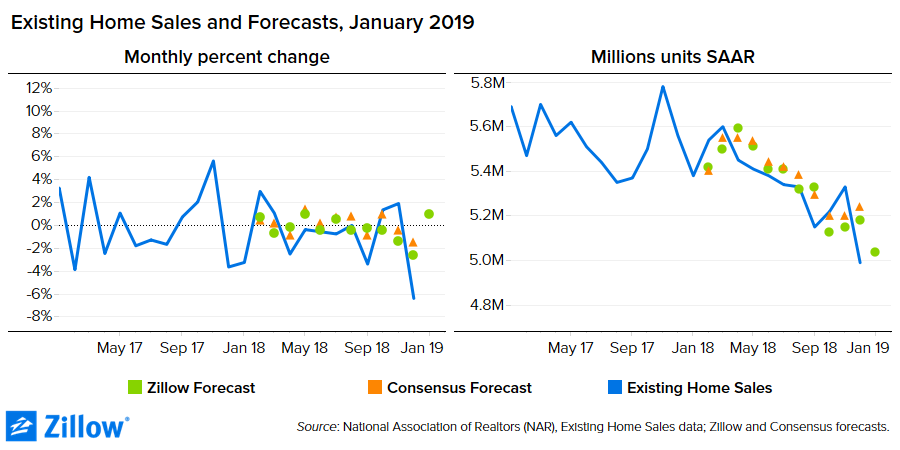

January Existing Home Sales: Another Disappointment, But Spring is Coming

- Existing home sales fell 1.2 percent in January from December, and were down 8.5 percent from a year ago to 4.94 million sales (SAAR), according to the National Association of Realtors.

- Inventory of existing homes for sale rose 3.9 percent from January and 4.6 percent from a year ago.

- The median (non-seasonally adjusted) price of existing homes sold in January was $247,500, up 2.8 percent from a year ago.

Another monthly decline to begin 2019 might be tough for some to swallow after a disappointing end to 2018 and months of generally soft sales numbers. But it's risky to read too much into the January existing home sales data. The partial federal government shutdown and the polar vortex that hit much of the country mid-month weighed on economic activity in January. But interest rates fell to 10-month lows, and with for-sale inventory creeping higher late in the fall, potential home buyers who had been sitting on the sidelines in fear of a broader housing market slowdown likely shifted their expectations as the market stabilized and jumped in come the New Year. But these sales likely won’t be visible in the closing data until February or March. The outlook for mortgage rates has shifted decisively lower over the past two months. Together, lower rates combined with stronger inventory and more temperate weather bode well for home sales in February and March.

The post January Existing Home Sales: Another Disappointment, But Spring is Coming appeared first on Zillow Research.

via January Existing Home Sales: Another Disappointment, But Spring is Coming

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Neighborhoods where you can find some peace and quiet

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

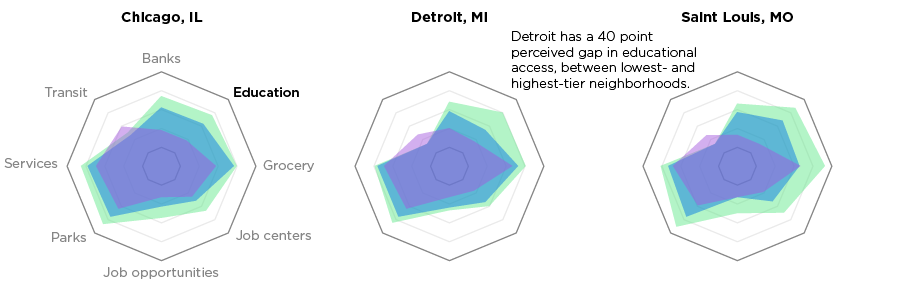

In Areas Where Home Values are Lower, Residents Perceive Worse Access to Education & Jobs

Where we live has a tremendous impact on our lives, including how easily we can climb the socioeconomic ladder, and economic prospects for children vary greatly depending where they grow up. Access to local amenities – the unique, beneficial and sometimes crucial features of a neighborhood – can go a long way in shaping those opportunities.

And local residents say that access to education, transit, job opportunities and other amenities varies widely depending on the price point of the neighborhood in which they live. Those living in areas with higher median home values said they are more satisfied with their access to local amenities, according to the latest Zillow Housing Aspirations Report (ZHAR), a semi-annual survey of 10,000 Americans in 20 large metro areas.[1] People living in areas with lower home values said they were largely not as satisfied – except when it comes to public transportation.[2]

Gaps in Perceived Access to Quality Education

Education was the amenity with the biggest gap in perceived access between people in bottom-tier neighborhoods (those with median home values in the lower one-third of all neighborhoods) and top-tier neighborhoods (those with median home values in the highest one-third). Less than 40 percent of people in areas in the bottom tier said they have relatively good access to high-quality education in their neighborhood — versus almost 70 percent of people in top-tier areas.

The perceived access-to-education gap between the priciest and least-pricey neighborhoods is sizable in most metros. The largest gap is in St. Louis, where only 27 percent of people living in a bottom-tier neighborhood reported relatively good access to a high-quality education compared to 81 percent in the top tier, a 54-point difference. Other midwest metros, including Detroit and Chicago, also had large perceived gaps in educational access, with point differentials of 40 and 36 between bottom- and top-tier neighborhoods, respectively.

And those metros with narrower gaps appear to be on more equal footing only because access to high-quality education is perceived to be relatively weak all-around. In Las Vegas and Tampa, Fla., less than 50 percent of respondents from all value tiers expressed satisfaction with their educational access. Still, Los Angeles shows that it is possible to have good perceived access to education that is widely shared – it is the only metro analyzed where more than half of residents from bottom-tier neighborhoods said they were satisfied with their access.

Axis of Opportunity

Across the board, respondents said that job opportunity was the least available amenity, with only a third of people nationwide saying they have good access to jobs in their neighborhoods. But again, access to these opportunities was perceived to be most sparse in bottom-tier neighborhoods – just 29 percent of residents in neighborhoods with lower home values said they had good access to jobs (compared to 40 percent among respondents from pricier areas). Residents of relatively less-pricey places in some metros reported at least decent access to jobs, but that may come with a significant trade-off as these metros also feature high housing costs overall. San Jose, Los Angeles and Seattle fall into this category – and even an entry level home in these areas is considerably more expensive than the median U.S. home. In December, the median (roughly middle-tier) U.S. home value was $223,900, well below the median bottom-tier home value in Seattle ($315,900), roughly half that in Los Angeles ($447,500) and less than a third than that in San Jose ($795,600).

But there is an axis of opportunity in America running north-to-south just east of the Continental Divide, where three metros – Minneapolis, Denver and Dallas – rank among the highest for perceived access to job opportunities among residents in bottom-tier neighborhoods. In each of these metros, the share of people in bottom-tier neighborhoods who said there is relatively good local job availability is on par with or above the overall national figure of 34 percent. These metros also match others in perceived bottom-tier access to high-quality education and financial services. And housing costs in these areas, while still higher than the U.S. median, are far lower than in the pricey West Coast metros mentioned earlier. All three metros are among Zillow's hottest markets for 2019.

Transit Flips the Trend

While perceived access to most amenities is worse among residents of bottom-tier neighborhoods, the pattern is reversed when it comes to public transit. In 14 of the 20 surveyed metros, those living in neighborhoods with higher home values reported worse access to transportation services. And in some of these metros, the difference in perceptions is pretty stark. In Philadelphia, 64 percent of respondents from bottom-tier neighborhoods said they enjoy good access to public transit, compared to only 30 percent of respondents in top-tier neighborhoods. The situation is similar in Denver and Las Vegas.

These differences may be because many highest or high value neighborhoods are farther away from urban cores, and so have less-frequent transit options. Or it may be because directed federal transit funding from programs like BUILD Transportation grants are geared toward economic revitalization in areas with lower home values. It could also reflect resistance of some high value communities to mass transit.

![]()

In New York and Washington, D.C., the results were flipped: A greater share of respondents living in top-tier areas said they enjoyed good access to transportation than those in the bottom tier, although respondents from less-pricey areas also reported decent access to public transportation in these areas.

Access to Basic Services Widely Perceived to be Available

Basic public services such as fire departments, libraries and hospitals were perceived as the most universally available amenities, with high ratings from respondents across all home-price tiers. Only 8 percent of respondents nationwide said they felt they had subpar access to these basic public services – and that did not fluctuate much among price tiers.

Basic public services are perceived to reach people living in all kinds of neighborhoods in most metros very effectively, but there are a few exceptions – again, particularly among respondents from bottom-tier neighborhoods. In Atlanta, Las Vegas and Washington, D.C., as many as 15 percent of respondents in bottom-tier neighborhoods reported weak access to these services. While that's a low number compared to people's perceptions about access to other amenities, it's critical that residents of all areas feel their access to essential services like fire response and medical care is on par with everyone else's.

[1] The Zillow Housing Aspirations Report, a semi-annual survey sponsored by Zillow and conducted by IPSOS, asks 10,000 renters and homeowners in 20 metros nationwide about their views on homeownership and their personal housing expectations going forward. Survey respondents were also asked to rank the availability and accessibility of amenities in their neighborhood.

[2] Respondents were asked "Compared to other areas, how would you rank the availability and accessibility of the following amenities/resources in your own neighborhood? [Amenity description]"

The post In Areas Where Home Values are Lower, Residents Perceive Worse Access to Education & Jobs appeared first on Zillow Research.

via In Areas Where Home Values are Lower, Residents Perceive Worse Access to Education & Jobs

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Recession Watch: Will Another Downturn Rock the Housing Market?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, February 20, 2019

Can Your Home Accommodate an Attic Room?

Depends on the roof framing.

The post Can Your Home Accommodate an Attic Room? appeared first on RE: Find.

from Can Your Home Accommodate an Attic Room?https://ift.tt/2GAten0

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Tuesday, February 19, 2019

How to Modernize a Split-Level Home

The possibilities are endless!

The post How to Modernize a Split-Level Home appeared first on RE: Find.

from How to Modernize a Split-Level Homehttps://http://bit.ly/2Gz9zng

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Meet the Clutter Scale: One Pro's Secret to a More Intentional Home

Although I have always been organized, there were two significant moments in my life that taught me how to manage clutter.

The first was when I returned from a backpacking trip around the world. Having visited homes in many developing nations, I no longer wanted to have such excess in my own home. My possessions were organized, but I had too many of them for my taste.

After I unpacked from my journey, I began a thorough review of my stuff. I started upstairs, removing unnecessary items floor by floor. By the time I reached the basement, I had enough stuff to set up a second apartment.

My second decluttering lesson was right after my divorce. Just months after the split, I was facing bankruptcy. I began my climb out of sudden and severe financial debt while simultaneously making a name for myself in the organizing industry. I hired a top-tier PR agent, but I knew I had to come up with some big bucks to cover his fee and all the expenses that go along with creating a brand. I decided to sell my home and everything I owned to make it happen.

As I sorted my belongings for a second time, I created the ranking system below to help me decide what to keep and what to toss. It worked beautifully for me, and I think it can work for you too.

The clutter scale

5 - Important items whose place in your home is non-negotiable. For me, this included my green-stained Depression glass, photos, business files, office equipment and car.

4 - Items that are difficult to replace and items you use every day. This pile included most of my clothes, some furniture, a favorite sheet set, towels and jewelry.

3 - Items you use occasionally but haven’t used within the last six months.

2 - Items you rarely use but feel hesitant to toss.

1 - Items you never use, like seasonal items, specialized tools or kitchen gadgets. I got rid of stationery, extra wrapping paper, old boxes and my printer.

You know what I found as I used the clutter scale? There were rarely items that rated a 2 or 3. And once I established some criteria, I sorted and purged the 2s and 3s like never before. As you sort your less important items, ask yourself the following questions:

- Do I love it?

- What's the special story behind it?

- Do I have the space for it?

- Can I replace it?

- Can I easily borrow it or rent it if I need it again?

- Does it support my goals and values?

- Does it compare to the items I ranked as a 5?

The clutter scale is a great way to get back in touch with your priorities. My priority at the time was starting my business, so I kept the bigger goal in sight and let go of anything that didn’t support it.

What I didn't know then was that I was already practicing what I was going to preach in my business. I learned to organize my life and stuff based on my values. I chose to collect experiences - not things.

As you declutter and rank your possessions, don’t forget to take a few minutes to think about your goals and values. You’ll find your home to be much more intentional and peaceful if you do!

Related:

- 5 Organizing Secrets Only the Pros Know

- 3 Steps to Creating an Organized Entryway (Even If You Don’t Have the Space)

- 10 Home Organization Woes (and How to Fix Them)

Originally published January 2017.

via Meet the Clutter Scale: One Pro's Secret to a More Intentional Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

6 Gorgeous Picks From Joanna Gaines’ New Anthropologie Line

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

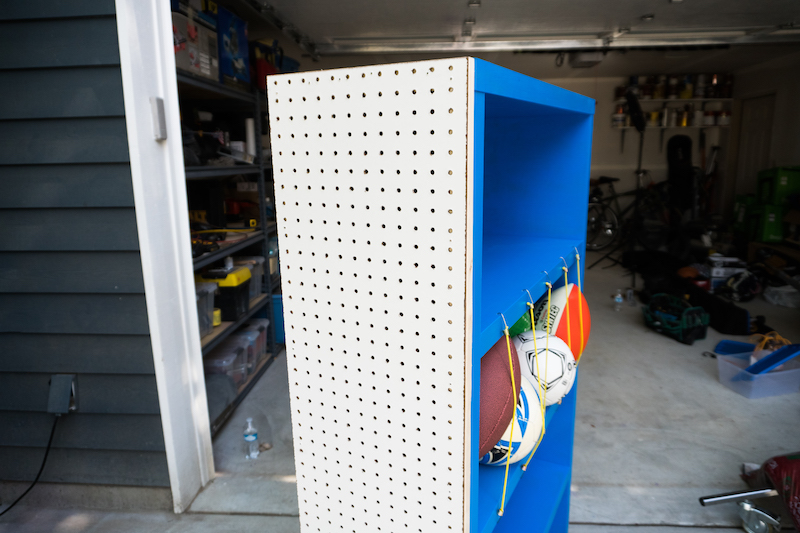

With This DIY Sporting Goods Catch-All, Game Day Is No Sweat

This project will help you organize your garage and become the MVP of DIY projects. With all your sporting gear in the same place, you’ll always be prepared when someone yells, "Where’s my basketball?” (Or volleyball, hockey stick, tennis racket, etc.)

See how it’s done, then follow the step-by-step instructions to build one of your own.

1. Find a bookcase

Choose a bookcase with at least three wide shelves so you can store gear in a variety of sizes.

2. Add locking wheels

Attach locking wheels to the bottom of the bookcase so you can easily move it around the mudroom or the garage.

3. Drill holes

Drill evenly spaced holes (about four or five, depending on the width of the bookcase) along the top surface of one of the shelves. Keep the holes fairly close to the edge - about one-half inch away or less.

On the underside of the shelf below, drill holes to match up exactly with the holes on the shelf above.

4. Attach bungee cords

Place the bungee cord hooks in the drilled holes, and arrange the cords vertically so they create a net. You want the cords to be pretty taut, so get the right size for your bookcase.

5. Mount peg boards

Frame the sides of your bookcase with 1-by-2-inch boards to support peg boards that have been cut to size. Secure the peg boards with a few nails on the top and bottom.

6. Customize with hooks and holders

Place hooks and holders on the peg board so you can hang your tennis rackets, baseball gloves, jerseys, helmets and more.

7. Load up your catch-all, MVP!

Grab your gear and organize the bins however you see fit. Now all you have to worry about is scoring the winning goal.

Related:

- A DIY for the Books: How to Get Custom Built-In Shelves on a Budget

- A Quick DIY for Space-Saving Kids’ Room Storage

- DIY Backyard Fire Pit: Build It in Just 7 Easy Steps

Originally published September 2017.

via With This DIY Sporting Goods Catch-All, Game Day Is No Sweat

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

What Is Zillow's Buyer-Seller Index, and How Is It Computed?

The Zillow Buyer-Seller Index (BSI) is a measure of the balance between sellers and buyers in a given market. A hot market, or sellers market, typically occurs when buyers are forced to compete for a limited supply of homes, often resulting in higher prices and/or quicker sales that tend to benefit sellers. A cold market, or buyers market, is the opposite: general lack of demand means homes can linger on the market longer and ultimately sell for less, putting negotiating power in the hands of buyers.

The media and others often use isolated housing market indicators and broad heuristics to classify markets as either hot or cold. Zillow's BSI uses a consistent, rigorously developed set of granular housing market fundamentals to create a nuanced scale of market heat, incorporating historical and regional quantitative context.

The full index includes two measurements:

- The cross-time BSI measures how hot a region's housing market is relative to its own history.

- The cross-region BSI measures how hot a region's housing market is relative to other regions at a single point in time.

Together, they capture the dynamics of negotiating power in a local housing market. Both indices are computed monthly.

Input Data

The BSI is computed using three input metrics:

- Percentage of listings with a price cut —The percentage of current for-sale listings on Zillow with a price cut during the month.

- Median days on Zillow — The median days on market of homes sold within a given month, including foreclosure re-sales.

- Median sale-to-list price ratio — The median of the ratio between the sale price and the list price for all homes (e.g. if a home with a list price of $200k sells for $250k, its ratio would be 5:4, or 1.25)

The days on Zillow and sale-to-list ratio used in our BSI calculation are slightly different than those series published regularly on our website. We'll explain in further detail below.

Cleaning of Input Data

Because the input data from Percentage of Listings with a Price Cut is calculated separately, it has its own suppression rules to determine which observations in each regional time series are suspicious. Only unsuppressed (publicly published) observations from each aggregate series are retained as inputs to the BSI.

Using a property-level algorithm to match transactions to listings, the Median sale-to-list price ratio as well as the number of days on Zillow (time on market) per matched transaction are calculated. Unlike published data, in order to ensure a more stable input for the BSI, both of these metrics are subject to special data management concerning the observation count, the aggregation and imputation strategies. Both metrics are then subjected to the following property-level suppression rules:

- Days on Zillow is reported as NA (missing) for a given transaction if it's lower than 10 or higher than 365.

- Median sale-to-list price ratio is reported as NA for a given transaction if it's below 0.5 or above 2 (list price is less than half or more than twice the sale price).

Aggregation and Outlier Removal of Input Data

Percentage of listings with a price cut is pre-aggregated to all regional levels. Both directly-calculated inputs, days on zillow and median sale-to-list price ratio are aggregated at the regional level by:

- Neighborhood

- ZIP code

- City

- County

- Metro (CBSA)

- State

- Nation (United States)

The aggregation uses a rolling median with a three-month window. Employing a rolling median with a smaller window leads to many regions having too few observations, while a bigger window does not significantly increase the number of regions for which data is observed. Data are considered too sparse in a given month for a region if the number of observations is fewer than 15. In these cases, the data value is reported as NA.

The three aggregate input metrics for BSI now have a time series structure for all regions of interest.

Input Data Volatility and Imputation

All input metrics can have significant month-over-month (MoM) volatility. To suppress outliers, MoM growth rates are calculated for each region and used to remove outliers. A metric's value for a given month-region combination is reported as NA if the MoM growth is less than negative 50 percent or more than 100 percent (in other words, it less than halves or more than doubles). This is done at all geographic levels.

When data are missing, they are imputed for child regions of metros using the nearest observed period for the child region. We then carry its value backward and/or forward to the missing periods, using the parent-metro’s MoM growth rates. If a metro's growth rates are missing for less than 12 months, they are linearly interpolated. If data are missing for more than one year, the state's growth rates will be used. If those are missing as well (which rarely happens), then U.S. growth rates will be used. If regions are missing more than 50 percent of their respective time series observations, data will be suppressed.

From Inputs to Final Metrics

Comparable Distributions and Seasonality

As each of the inputs' units are absolute, the inputs are normalized by forcing their respective distribution to be on the inclusive interval 0 to 1. As minimum and maximum values, the "global" maxima/minima across regions and time periods of the unsuppressed data are used. This implies a comparison of data across regions. However, this may be the least restrictive way of normalizing the inputs while maintaining a valid comparison over time.

The fundamental Buyer-Seller Index (raw BSI) is defined for a given region and month as the average of the three inputs. As it is a convex combination of normalized inputs, it is bound between 0 and 1. Due to strong seasonality, there exists a seasonal decomposed version of the raw BSI (trend component). The decomposition uses the X-13ARIMA-SEATS method. If the seasonal decomposition fails (due to non-convergence of likelihood optimizer), the region gets excluded from the dataset to ensure comparability between the seasonal decomposed BSI and raw BSI (this is the case for roughly 5 regions).

Smoothing and Creating Final BSI Flavors

As the seasonally decomposed BSI and raw BSI can both still contain strong fluctuation, a three-month rolling (trailing) mean is calculated. This smoothed flavor of raw BSI is used to calculate the end products:

- To capture time variation in one region's market (BSI Cross-time), there will be a ranking for a respective region with its own time series , initially ranging from zero to the number of time periods, and then scaled to the closed interval from 0 to 10.

- To capture how a region's market compares to surrounding areas' markets (BSI Cross-region), a ranking takes place within any given month, comparing a region's raw BSI with its peer regions' one. The ranking initially ranges from zero to the number of like-typed regions in that period, and is then also scaled to the closed interval from 0 to 10.

This yields two metrics (following the order described above):

- BSI Cross-time: BSI Cross-time Smoothed and Seasonal Adjusted (SSA)

- BSI Cross-region: BSI Cross-region Smoothed and Seasonal Adjusted (SSA)

The ranking for (2.) takes place in the following structure:

- Neighborhoods, ZIPs, Cities are ranked in their respective parent metros

- Metros, Counties, States are ranked across the U.S.

- The U.S. is ranked with respect to itself (resulting in a constant value for BSI Cross-region)

Interpretation of the Index

As the index is relative to its own history, it is computed monthly for all regions and time periods.

The final BSI lies on the inclusive interval of 0 to 10. A value of 0 indicates that the market is relatively cold/not tight/buyers have more negotiating power. A value of 10 indicates that the market is relatively hot/tight/sellers have more negotiating power.

It's important to keep in mind that the index forces each observation to lie in the interval 0 through 10, even in markets which are relatively stable over time. Because of the forced boundaries, those markets may appear more volatile than they actually are.

The post What Is Zillow's Buyer-Seller Index, and How Is It Computed? appeared first on Zillow Research.

via What Is Zillow's Buyer-Seller Index, and How Is It Computed?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Beach in December: Bargain Rents in Chilly Weather

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

The Top 10 U.S. Cities to Buy Your Starter Home—or Your Forever Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Why Early May Is the Best Time to List a Home for Sale

- U.S. homes listed for sale in early May sell for $1,600 more than the average listing throughout the year.

- Homes listed on a Saturday are viewed the most on Zillow within the first week of listing.

For home buyers in recent years, it may feel like the best time to begin their search in order to beat the spring competition has gotten earlier and earlier. But for home sellers, the best time to list a home for sale has remained remarkably consistent: Once again, U.S. homes listed for sale on Zillow in the first half of May have sold for more money and more quickly than the average listing throughout the year.

Nationwide, homes listed for sale between May 1 and May 15 tended to sell for about 0.7 percent more (or roughly $1,600 on the typical U.S. home) and about six days faster than usual. And while the exact best time to list a home varies from market-to-market, in most cases the magic window falls squarely in spring.

In 29 of the 35 large markets analyzed, the magic two-week window for listing fell between the second half of March and first half of June. In the remaining six markets – Charlotte, Dallas, Houston, Las Vegas, Miami and Tampa – the magic window was the first half of July.

The metro area exhibiting the largest price boost from a particular half-month was Minneapolis-St. Paul, which shares the same early-May window as the nation as a whole. Homes listed during that time-frame in the Twin Cities area sell for about 1.8 percent more ($4,900 on the median local home). San Jose, Calif., and Chicago both also saw their biggest boosts in early May, of about 1.5 percent in each metro area ($18,900 and $3,300, respectively). The sweet spot for listing comes a bit later in Seattle and Columbus, Ohio, where early June listings typically see a 1.5 percent premium ($7,500 and $2,900 respectively).

The two-week magic window doesn't just mean more money – it can also mean a faster sale. And when time is money, the benefits of listing at the right time are even greater. In Cleveland, homes listed for sale in the area's early-May magic window sell almost two weeks faster (13 days) than an average listing throughout the year, the most time savings of any of the markets analyzed.

If you want to get even more strategic about when to list, it can also pay to consider what day of the week will get your home seen by the most house hunters. Nationwide and in 12 of the largest 35 metros, Saturday listings get the largest number of views by users on Zillow within the first week of listing. Friday is a great day to list as well, with homes listed that day getting the most views after a week in 10 of the top 35 markets. At the other extreme, Tuesday is worst time to list, nationally. Saturday listings end up with about 20 percent more page views in their first seven days on the market than Tuesday listings.

The post Why Early May Is the Best Time to List a Home for Sale appeared first on Zillow Research.

via Why Early May Is the Best Time to List a Home for Sale

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Monday, February 18, 2019

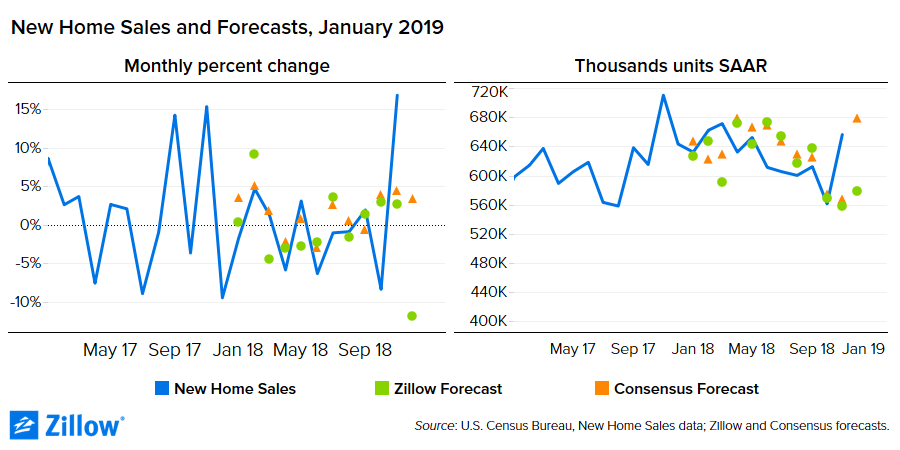

Forecasts for Existing and New Home Sales (January 2019)

- Zillow expects estimates January existing home sales to rise 0.9 percent from December to 5.04 million units at a seasonally adjusted annual rate (SAAR). That's down 6.4 percent from January 2018.

- We estimate new home sales totaled 643,000 units (SAAR) in January, up 1.6 percent from a year earlier.

Existing home sales posted an exceptionally weak December – registering their slowest pace in more than three years. But December marked a recent high point for economic pessimism: Mortgage rates were coming off seven-year highs, the stock market sank deep into correction territory, a partial federal government shutdown loomed, and the Federal Reserve seemed poised to push interest rates higher.

Somewhere between Christmas and New Year's, however, everything changed.

The shutdown plunged forward – taking a measurable toll on economic sentiment and data for much of January – but the Fed paused, rates dipped, and financial markets rallied. Potential home buyers who had sat on the sidelines during the Q4 turbulence saw for-sale inventory rising and, once interest rates dipped, the buyers again began to (tentatively) bite.

We expect existing home sales posted a modest rebound in January despite headwinds associated with the partial government shutdown, rising 0.9 percent from December to 5.04 million units at a seasonally adjusted annual rate (SAAR). They remain down 6.4 percent from a year earlier.

The National Association of Realtors (NAR) will report January existing home sales on Thursday, February 21.

The outlook for new home sales is somewhat cloudier, because December new home sales data still have not been released as a result of the partial government shutdown. (The Census Bureau reported November new home sales a month late, on January 31,and plans to release December new home sales on Thursday, February 26. They have yet to announce a release date for January new home sales.)

We expect new home sales fell 2.1 percent in December to 643,000 units (SAAR) – up 1.6 percent from a year earlier – and then rose 0.6 percent in January to 647,000 units (also SAAR).

The post Forecasts for Existing and New Home Sales (January 2019) appeared first on Zillow Research.

via Forecasts for Existing and New Home Sales (January 2019)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

What is a Mortgage Forbearance?

There is help for a temporary setback.

The post What is a Mortgage Forbearance? appeared first on RE: Find.

from What is a Mortgage Forbearance?http://bit.ly/2DOwpU9

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Getting Ready for Tax Season: A 3-Step Plan

It’s true: Tax time is right around the corner. April 15 will be here before you know it, and that means there’s no better time than now to get yourself ready for the big day. Whether you use a CPA or are a fan of filing your taxes online, getting prepared will help you file your taxes with ease.

1. How to Organize Your Taxes

Filing your taxes can involve a lot of paperwork. One of the best steps to take is to store all your W-2s or 1099s in one central place, like a physical folder. You can also include any credit card annual statements for your deductions as well as any student loan or home loan interest forms. Any document that you think you might need to file your taxes should find its home in your tax folder.

|

|

|

If you’re self-employed or have a side hustle, you likely will be claiming some deductions off your taxes. There’s no shame in having a pile of receipts that you’ve collected throughout the year, but now is the time to categorize your receipts, so you know how much to deduct.

There are lots of great mobile apps to help you manage your expenses and deductions, such as QuickBooks and FreshBooks. They will make your life easier when it comes to filing your taxes.

2. How to File Taxes

The million-dollar question is always should you use an accountant or online software to file your taxes. While there isn’t one right way to answer that question, a good rule of thumb is to look back at the previous year. Did you have any major milestones, like getting married, having a baby, starting a business, losing your job or buying a house? If the answer is yes, you should consider talking with an accountant to make sure you’re taking advantage of all your deductions and maximizing your potential deductions.

Filing your taxes online is an equally great option. For starters, it’s usually lower in cost than working with an accountant and straightforward. Within a few minutes, and with all the information in your tax folder, you can file both your state and federal taxes.

There are a couple of great resources to be aware of when it comes to filing your taxes:

- Volunteer Income Tax Assistance Program: This program offers free tax filing help to anyone making $55,000 or less, persons with disabilities and limited English speakers.

- If you make below $66,000, you can file your state and federal taxes for free with many different companies.

3. What to Do With Your Tax Refund

More than 7 out of 10 filers receive tax refunds of at least $2,800. That’s a nice amount to get as a refund and can be used in so many great ways to help you fund your financial goals. The problem is that most people don’t have a plan for their refunds, so the money seems to disappear.

Before you receive your refund check, make a list of what you plan to do with your refund so you can maximize it.

- Do you have high-interest credit card debt to pay off?

- Are there financial risks you need to cover, like buying life insurance?

- What are your financial goals for this year that need a little boost in funding?

- Does your emergency fund need a cash infusion?

- What about donating some of your refund to your favorite charity?

There are so many amazing things you can do with your refund if you have a plan in place. Take out a piece of paper and a pen and jot down some of the goals that you’d like to achieve with your refund and put a dollar amount next to them. Once you get your refund check, divvy up your funds and put them towards the items on your list.

The post Getting Ready for Tax Season: A 3-Step Plan appeared first on RE: Find.

from Getting Ready for Tax Season: A 3-Step Planhttps://http://bit.ly/2T1QGPQ

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

This Once-Scruffy Beach Town Is South Florida’s New Real Estate Hot Spot

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Yankee Doodle! We Salute 9 Homes From America’s Revolutionary Era

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Friday, February 15, 2019

Quiz: Should You Renovate Your Home or Sell?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thanks for Sticking Around!

We're so pleased that you've decided to continue using and enjoying RealEstate.com! We'll be sure to keep you on our mailing list. Here are some helpful tips, so you can make the most of your experience on our site:

Get to Know All-In Monthly Pricing

All-In Monthly Pricing is designed to cut through all the noise and confusion to give first-time buyers (that's you!) a more realistic snapshot of monthly mortgage-related expenses. Knowing an average monthly cost ahead of time can help you better establish (and stay within) a home budget. Learn how to use our cost to buy a home calculator.

Save Your Favorite Homes and Searches

Click the *heart* icon in the top right corner of each property to save it in your favorites folder. To save time on return visits, click the orange "Save Search" button in the upper right corner of a search results page to save your favorite search criteria (city/state, price, bedrooms, etc.). Search for homes.

Update Your Preferences

Be sure to visit your profile page and select the types of notifications you wish to receive from us, including our weekly newsletter and updates on a property's status. Miss this step and a home you love and saved in your favorites folder could slip through your fingers! Log into your account.

The post Thanks for Sticking Around! appeared first on RE: Find.

from Thanks for Sticking Around!http://bit.ly/2N9YObm

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Your Account on RealEstate.com

Thank you for supporting RealEstate.com and letting us know that you no longer wish to receive emails from us. We will remove you from our mailing list. Should your home buying plans change, we invite you to return and create a new account.

The post Your Account on RealEstate.com appeared first on RE: Find.

from Your Account on RealEstate.comhttps://http://bit.ly/2V3dSuu

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Suburban Home With Sex Dungeon Spanks Competition, Becomes Most Popular Home

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Thursday, February 14, 2019

Amazon's Exit from New York Most Likely to be Felt By Early Long Island Investors

Amazon's announcement Thursday that it will not build a new headquarters in Long Island City is expected to impact not only the housing market there, but also places like Arlington County, Virginia, and Nashville, where many of those jobs are likely to move.

The Washington D.C. metro area, named late last year along with Long Island City as the home of a new headquarters, already was expected to gain nearly 38,000 Amazon employees. A Zillow analysis projected that — even if 50,000 new Amazonians join the workforce there — rent growth would rise beyond the already-minimal expected gain by less than one percentage point. That's thanks in part to a well-developed public transit system, deep labor market and responsive housing supply.

The impact would be smaller in places like Toronto and Boston, where Amazon has offices that could add some of those workers. In Nashville, though, where Amazon also is building out its workforce, 50,000 more workers would have meant a near tripling of rent growth. A smaller influx of employees would mean a smaller impact, but still likely larger than in some of the bigger metro areas where Amazon has offices. Interestingly, Nashville's Elizabeth Park neighborhood – a roughly 30 minute walk from Amazon's proposed Nashville Center of Excellence – was the most-loved Nashville neighborhood on Zillow in recent months according to a recent Zillow analysis.

The impact in Long Island City now is most likely to be felt by those who dove into real estate following Amazon's HQ2 announcement in November. Median list price for condos in the area jumped from essentially flat year-over-year in August to nearly 10 percent higher in November and nearly 12 percent higher in December. Growth in year-over-year median condo rental price per square foot tripled from October to December.

For investors and hopeful locals who bought Long Island City real estate after Amazon announced it was coming there, the news is disheartening. Indeed, they are likely to see a near-term dip, but the longer-term outlook for New York City real estate is still good. New York continues to be an attractive area for jobs, and companies besides Amazon are still growing there. The city's persistently sky-high rents are a testament to the Big Apple's enduring popularity. But the experience also demonstrates how important it is to consider potential housing needs in any local economic development plans.

The post Amazon's Exit from New York Most Likely to be Felt By Early Long Island Investors appeared first on Zillow Research.

via Amazon's Exit from New York Most Likely to be Felt By Early Long Island Investors

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

8 Curb Appeal Boosters You Can Do in a Weekend

A polished home exterior creates an inviting experience for visitors or passersby, which is especially important if your home is on the market.

Check out our tips to get the most curb appeal for the lowest cost - while turning your neighbors' heads and getting prospective buyers to your door.

Clean up

The easiest way to enhance curb appeal is dedicating a weekend to deep cleaning your home’s exterior.

Sure, you'll want to trim bushes, sweep and mow your lawn, but there's more to curb appeal than keeping a tidy front yard. Turn the nozzle on your garden hose to the strongest setting and clean off your driveway, sidewalk, windows and fence.

If dirt and grime are caked on your home's exterior, you can rent a powerwasher for around $50 to $75 a day. Just avoid areas with caulking, like windows and doors, because you can strip some of the sealing. And as tempting as it may be to powerwash your roof, don’t do it - you may damage the shingles’ coating.

When it comes to your windows, spraying them with a garden hose isn't enough. For maximum sparkle, clean your windows outside and inside. Instead of relying on a glass cleaner, try a mix of detergent diluted in warm water.

Add shutters

Shutters are an easy way to accentuate the size of your windows. They make your windows look larger and add visual interest by disrupting a bland exterior wall. For maximum curb appeal, choose a shutter color that contrasts with your home’s color to make it pop.

Paint accent areas

Paint is a quick and easy curb appeal booster. Instead of painting the entire exterior of your home, focus on the trim, door and shutters.

You can typically find a gallon of exterior paint for $20 to $30. But before you decide on a color, consider home exterior color trends, along with your home's natural style.

Give your door a face lift

If you don’t love your front door, you don't need to dish out loads of money to replace it. Think beyond paint - consider adding molding, which offers a decorative frame for your door that welcomes visitors.

You can also add metal house numbers, which you can find for as low as $5 a number. And if seasonally appropriate, consider adding a wreath to your door as a bonus.

Replace your house numbers

If you'd rather not add house numbers to your freshly painted door, here are some alternative DIY ideas:

- Paint a terra-cotta planter with your house number and place it by your doorstep.

- Add house numbers to a post planter near your front porch.

- Use your front porch stair riser’s real estate by hanging or painting numbers there.

Update your light fixtures

Replacing your exterior light fixtures is another curb appeal must. You can usually find outdoor sconces for around $20 at home centers. Just make sure your new light fixtures have the same mounting system. And if you want to save on lighting, a fresh finish can do wonders. Try spray-painting them - a can of spray paint costs around $10.

Keep porch furniture neutral

Just as you would aim to simplify the interior of your home so shoppers can envision themselves living there, the exterior of your home should be neutral and welcoming too.

Put your pink flamingo and wind chime collection into storage, and focus on porch decor that offers pops of color and character. You can find brightly colored outdoor chairs or throw pillows for $20 to $30 each.

Don’t forget the small things

These low-budget fixes make a big impact, so don’t forget the little details!

- Upgrade your mailbox: Install a new mailbox for under $100, or spray paint your existing mailbox.

- Plant a tree: A charming tree can up your curb appeal for as low as $20.

- Build a tree bench: If you already have a tree you love, build a bench around it! Great for napping, picnicking or just hiding exposed roots, a wraparound tree bench costs only what you spend on boards and screws.

- Install flower boxes: For around $20 each, flower boxes are a quick way to add some life and color to your windows. If flower boxes sound like too much work, try a container garden in pots by your front porch.

- Hide eyesores: Place a small lattice fence or a side of paneling around your air conditioner, and hide your trash bins behind a small fence. You can also hide your hose in a pot or storage bench.

Related:

- 5 Myths (and 5 Truths) About Selling Your Home

- Property Descriptions 101: How to Write Listing Descriptions That Sell

- 3 Must-Do’s Before Listing Your House for Sale

Originally published March 2018.

via 8 Curb Appeal Boosters You Can Do in a Weekend

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

$68M Waterfront Estate in Coral Gables Is Most Expensive New Listing

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

How Big of a Blow Did Amazon Just Deal Long Island City’s Housing Market?

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

10 Epic Bedroom Design Fails That’ll Haunt Your Dreams

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

For First Time in 5 Years, Buyers Have More Selection to Start the Year (January 2019 Market Report)

- U.S. for-sale home inventory increased 1.2 percent from a year ago. The largest inventory increases were seen in softening but still competitive West Coast markets.

- The typical U.S. home was worth $225,300 in January, 7.5 percent more than a year ago.

- The median rent rose 2.1 percent over a year ago to $1,468, the third straight month of accelerating appreciation.

January marked the reversal of a longstanding trend in the housing market – a modest annual gain in for-sale inventory last month means that for the first time in at least a half decade, the U.S. housing market began the calendar year with more homes available for sale than the year prior.

There were slightly more than 1.6 million U.S. homes listed for sale on Zillow in January, up 1.2 percent from a year ago and the first annual gain recorded in January since prior to 2014,[1] according to the January Zillow Real Estate Market Report.[2] The small bump in inventory to start the year may give those buyers eager to get an early jump on the spring home shopping season some reason for optimism after years of consistent inventory declines, though inventory levels overall remain constrained.

Inventory fell year-over-year for 44 straight months beginning in January 2015, before reversing course in September 2018. It has since grown on an annual basis in four of the past five months, though at a fairly tepid pace. And inventory remains far below peak levels: The 1,618,058 U.S. homes for sale in January is down more than 20 percent from the recent high of more than 2 million set in July 2014.

Inventory remains below peaks reached in the past five years in all 35 of the nation's largest markets for which we have adequate inventory data – in many cases far below. January inventory was more than 20 percent below recent peaks in 24 of these 35 markets, and less than 10 percent below peak in just seven.

Still, inventory did rise year-over-year in 28 of those 35 large markets, and many are adding inventory at a rapid pace, especially a handful of previously red-hot West Coast markets. On an annual basis, January inventory grew 42.9 percent in San Jose, Calif. (904 more homes available for sale in January 2019 from January 2018), 36.9 percent in Seattle (3,324 more homes), 31.9 percent in San Diego (2,450 more homes), 29.1 percent in Los Angeles (6,682 more homes) and 25 percent in San Francisco (1,556 more homes). Recent rapid growth in inventory is putting many of these areas closer to recent peak levels: Inventory is less than 10 percent below recent peaks in Los Angeles and San Jose, and is just 2.3 percent below peak in San Francisco.

For the past several years, many home buyers may have felt they couldn't catch a break as the number of homes available for sale continued to shrink each passing month. But something shifted during the second half of 2018, and while home buyers aren't yet out of the woods there is a glimmer of light on the horizon. The number of homes on the market is hesitantly inching higher – now approaching the highest level in a year and a half. And in the priciest markets, the jump has been even more definitive.

But buyers should not mistake a few more options for a sudden bounty, and this latest growth spurt in inventory has done little to cool rapid home value appreciation that has been driven in large part by high demand from buyers and limited availability of homes for sale. The median U.S. home value in January was $225,300, up 7.5 percent year-over-year. Annual U.S. home value growth has remained steady in the seven percent range over the past two years, though the national numbers obscure substantial differences across the country.

Home values were up year-over-year in each of the country's 35 largest markets. Indianapolis and Atlanta experienced the biggest jumps over the past year, with home values increasing by more than 12 percent in both metros.

Rents also continue to grow. The U.S. median rent rose to $1,468/month in January, up 2.1 percent from a year ago, the largest annual increase in rent since May 2018 and the third straight month of annual growth after a brief flattening and decline in August, September and October 2018. Rent increased or remained flat in all major metros, with Orlando (up 7.4 percent) experiencing the biggest increase. On the other end of the spectrum, rents were flat in Portland over the past year.

Mortgage rates on Zillow ended January at 4.14 percent,[3] the lowest rate of the month. On January 1, rates began the year at their highest point, 4.3 percent. By the end of January, mortgage rates had retreated 61 basis points from their most-recent November 2018 peak.

Lower rates headed into the spring home shopping season may give buyers slightly more wiggle room in their budgets, helping to keep monthly mortgage payments more manageable even as home prices themselves continue to rise. But the benefit of lower rates may prove to be a double-edged sword for buyers – lower rates do boost affordability, but may also drive more buyers into the market, creating a more competitive environment than the brief lull the market experienced as 2018 came to a close.

[1] Zillow inventory data begin in January 2013, so year-over-year calculations for the month of January are only available beginning in January 2014.

[2] The Zillow Real Estate Market Reports are a monthly overview of the national and local real estate markets. The data in Zillow’s Real Estate Market Reports are aggregated from public sources by a number of data providers for 928 metropolitan and micropolitan areas, in many cases dating to 1996. Mortgage and home loan data are typically recorded in each county and publicly available through a county recorder’s office. All current monthly data at the national, state, metro, city, ZIP code and neighborhood level can be accessed at http://bit.ly/RyJFlw.

[3] Zillow’s real-time mortgage rates are based on thousands of custom mortgage quotes submitted daily to anonymous borrowers on the Zillow Mortgages site and reflect the most recent changes in the market.

The post For First Time in 5 Years, Buyers Have More Selection to Start the Year (January 2019 Market Report) appeared first on Zillow Research.

via For First Time in 5 Years, Buyers Have More Selection to Start the Year (January 2019 Market Report)

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

‘Help! My Luxury Rental Was Turned Into a College Dorm’

Hi, I'm Parker Stiles. I'm the owner of Barrington Acquisitions, a real estate investment company operating in Charleston, SC and Atlanta, GA.

We help homeowners sell their home fast.

Wednesday, February 13, 2019

What is Zillow's Buyer-Seller Index, and How is it Computed?

The Zillow Buyer-Seller Index (BSI) is a measure of the balance between sellers and buyers in a given market. A hot market, or sellers market, typically occurs when buyers are forced to compete for a limited supply of homes, often resulting in higher prices and/or quicker sales that tend to benefit sellers. A cold market, or buyers market, is the opposite: general lack of demand means homes can linger on the market longer and ultimately sell for less, putting negotiating power in the hands of buyers.

The media and others often use isolated housing market indicators and broad heuristics to classify markets as either hot or cold. Zillow's BSI uses a consistent, rigorously developed set of granular housing market fundamentals to create a nuanced scale of market heat, incorporating historical and regional quantitative context.

The full index includes two measurements:

- The cross-time BSI measures how hot a region's housing market is relative to its own history.

- The cross-region BSI measures how hot a region's housing market is relative to other regions at a single point in time.

Together, they capture the dynamics of negotiating power in a local housing market. Both indices are computed monthly.

Input Data

The BSI is computed using three input metrics:

- Percentage of listings with a price cut —The percentage of current for-sale listings on Zillow with a price cut during the month.

- Median days on Zillow — The median days on market of homes sold within a given month, including foreclosure re-sales.

- Median sale-to-list price ratio — The median of the ratio between the sale price and the list price for all homes (e.g. if a home with a list price of $200k sells for $250k, its ratio would be 5:4, or 1.25)

The days on Zillow and sale-to-list ratio used in our BSI calculation are slightly different than those series published regularly on our website. We'll explain in further detail below.

Cleaning of Input Data

Because the input data from Percentage of Listings with a Price Cut is calculated separately, it has its own suppression rules to determine which observations in each regional time series are suspicious. Only unsuppressed (publicly published) observations from each aggregate series are retained as inputs to the BSI.

Using a property-level algorithm to match transactions to listings, the Median sale-to-list price ratio as well as the number of days on Zillow (time on market) per matched transaction are calculated. Unlike published data, in order to ensure a more stable input for the BSI, both of these metrics are subject to special data management concerning the observation count, the aggregation and imputation strategies. Both metrics are then subjected to the following property-level suppression rules:

- Days on Zillow is reported as NA (missing) for a given transaction if it's lower than 10 or higher than 365.

- Median sale-to-list price ratio is reported as NA for a given transaction if it's below 0.5 or above 2 (list price is less than half or more than twice the sale price).

Aggregation and Outlier Removal of Input Data

Percentage of listings with a price cut is pre-aggregated to all regional levels. Both directly-calculated inputs, days on zillow and median sale-to-list price ratio are aggregated at the regional level by:

- Neighborhood

- ZIP code

- City

- County

- Metro (CBSA)

- State

- Nation (United States)

The aggregation uses a rolling median with a three-month window. Employing a rolling median with a smaller window leads to many regions having too few observations, while a bigger window does not significantly increase the number of regions for which data is observed. Data are considered too sparse in a given month for a region if the number of observations is fewer than 15. In these cases, the data value is reported as NA.

The three aggregate input metrics for BSI now have a time series structure for all regions of interest.

Input Data Volatility and Imputation

All input metrics can have significant month-over-month (MoM) volatility. To suppress outliers, MoM growth rates are calculated for each region and used to remove outliers. A metric's value for a given month-region combination is reported as NA if the MoM growth is less than 50 percent or more than 100 percent. This is done at all geographic levels.