- The typical household in the Washington, D.C., metro has the most money left over after paying for a median-sized mortgage.

- Typical Los Angeles metro households have the least money left over after paying their mortgages.

- Median-earning household in San Jose, Calif., has the most money left over after making the typical rent payments in that area – despite the fact that these households pay an unusually large share of their incomes on housing.

It's a general guideline that people should not spend more than 30 percent of their incomes on rent or a mortgage. That ratio leaves room to buy food, clothes and other items without creating too much financial stress.

In some parts of the country, staying below 30 percent is a breeze. In others, it's all but impossible. Rather than just report what the percentages were for each market in the fourth quarter 2018, we decided to look at how much money is left over after the median-earning household pays the typical rent or mortgage in the largest metro areas. Those dollars clearly go further in some places than in others – but seeing how much people have left in the bank after housing is covered each month tells the story from a different angle.

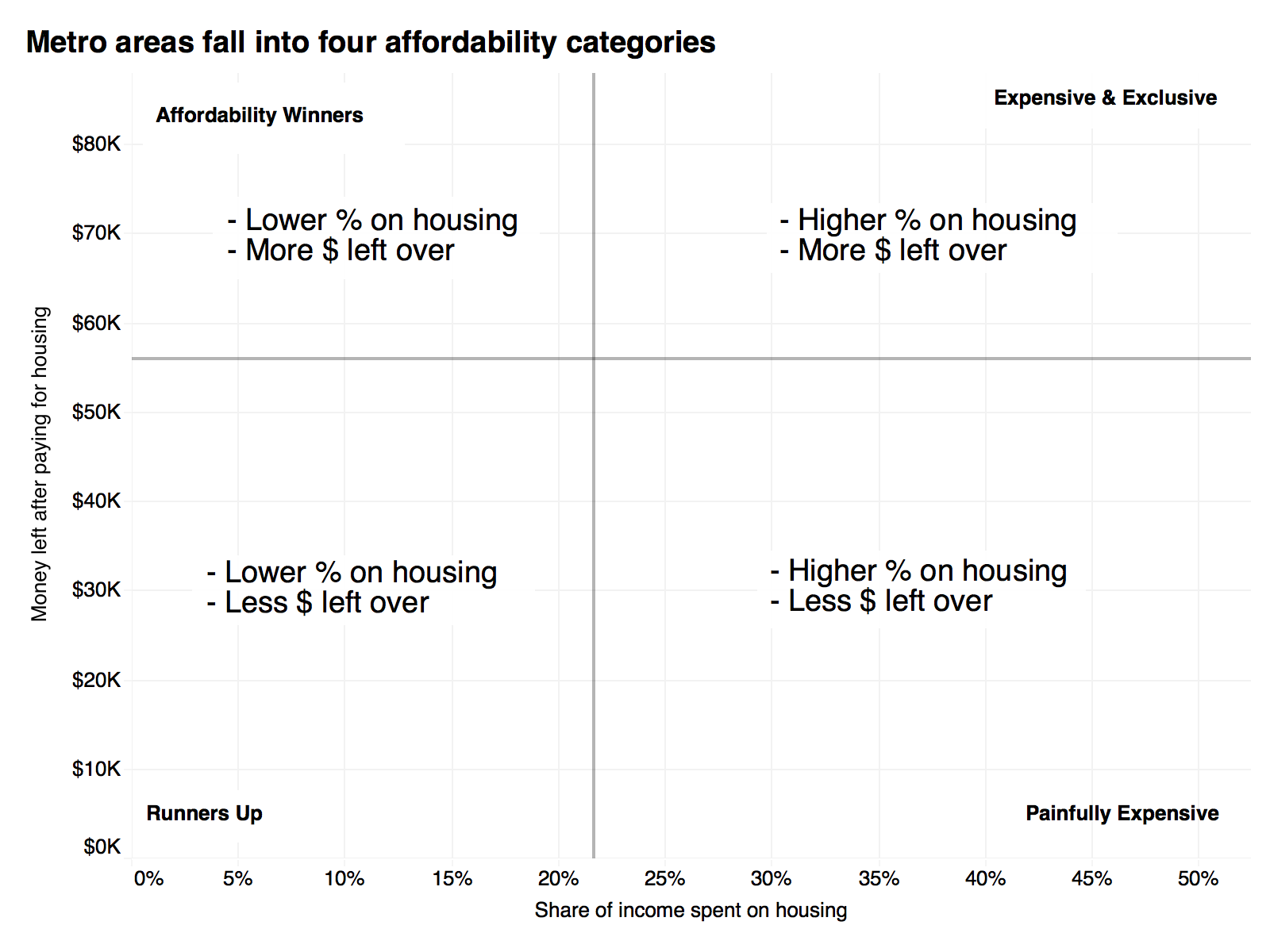

The major U.S. metros fall into four affordability categories:

Expensive & Exclusive

In these markets, median-earning households spend a high percentage of their income on the typical rent or mortgage, but still have a solid amount of money left over.

These metros prove that having a lot of cash left over does not necessarily mean an area is affordable.

A good example is San Jose, Calif., the major metro where median-earning households have the most money left over – $81,880 a year – after paying the median rent. The median rent takes up 34.1 percent of the median income – making San Jose one of the least affordable major metro areas in the country.

Even that 34.1 percent figure is low for many San Jose renters: For lower-income households in the metro area, a lower rent price still would consume 99.8 percent of their incomes[1] – which is financially impossible and requires people to find roommates and make other lifestyle decisions to live there.

Other expensive and exclusive metros include Boston, San Francisco and Seattle.

Affordability Winners

These are markets where households earning the median income and paying the median rent price spend a smaller share of their income on housing and have more dollars left over.

The market with the second highest amount of money left over after rent is Washington, D.C., at $77,738 a year – but median-earning renters in D.C. pay just 25 percent of their incomes on the typical rent. That's partly because the median household income is so high, and because the metro area covers much of Virginia and Maryland, where median rents are not as high as they are in the city center.

Other metros where typical renters have at least $50,000 a year left over – after spending no more than 27 percent of their incomes on rent – are St. Louis, Kansas City, Mo., Atlanta, Columbus, Ohio, Dallas-Fort Worth, Philadelphia, Chicago, Baltimore and Minneapolis-St Paul.

Runners Up

In these metros, people typically pay a smaller share of their incomes on the average rent or mortgage — and have fewer dollars left over.

They include a handful of metros in the Southwest and Midwest, including Pittsburgh, where the median-earning household spends 21.4 percent on the area's typical rent and has $48,172 left over. It's possible that that amount of money goes further in some metros than it would in markets with higher costs of housing – but that's not necessarily the case and will vary by market, along with taxes, childcare and other costs.

Painfully Expensive

These metros have the worst of both worlds: median-earning households spend a higher share of their income on housing and have less money left over.

In Los Angeles, renters spend 45.7 percent on the typical rental and $39,926 a year left over. And while homeowners at the national level tend to spend a smaller share of their incomes on mortgages than renters do on rent, the situation for homeowners in Los Angeles is almost as bad: They pay 43.7 percent of their incomes on the typical mortgage – using current home values, so this applies mostly to people who recently bought a home – and still have just $41,426 left over.

The situation for lower-income renters and homeowners is predictably worse: People earning lower incomes in Los Angeles would have to pay 121.2 percent of their incomes on a typical lower-priced rental. They would have to pay 83.8 percent of their incomes on a mortgage for a lower-priced home priced.

The varying toll of taxes

While this analysis excludes federal, state and local taxes, it's important to note that taxes mean that a homeowning household in Austin, Texas, would keep more of its income after taxes than one in San Diego.

The calculation for a household in San Francisco making the median income shows it would be left with $71,152 after paying income and payroll taxes. Spending the typical 44.2 percent of its income on a mortgage would leave it with $26,674 in spending money — less than half of what it would have after subtracting the mortgage cost alone.[2]

Childcare can cost more than rent

That same calculation can be done for a variety of services, including childcare. According to a Hotpads analysis, in some metros, households pay more for childcare than they do for rent.

Even in areas where childcare is cheaper than housing, it still represents a large chunk of a household's budget. The average household in San Francisco pays about $24,000 for the service. A typical renter there paying that amount would see their post-housing income drop from $66,423 to $42,423.[3]

Following up from the tax example above, a San Francisco homeowner with the median income paying the typical mortgage would be left with $2,674 a year to cover all other expenses after paying for childcare, taxes and the mortgage.

Transportation can drive budgets into the dirt

Metros with high fuel costs and less transit, like Los Angeles, also represent a higher cost of living than those with more robust transit systems, like Chicago or New York.

While San Francisco households pay, on average, $1,676 a year on public transit and $8,276 on transportation in general, including for cars, they still spend less overall on transportation than their Los Angeles counterparts — who pay 21.9 percent more on transportation. For a median-income household there with all the expenses mentioned above, this added cost would put them in the red.

Transportation also chews into household budgets in metros like Detroit with high car insurance costs. Detroit residents spend, on average, $4,458 a year on vehicle expenses like insurance (excluding car payments and fuel) — 85 percent more than households in Chicago, a fellow midwestern city.

Basic necessities breaking the bank in some places

The grand sum of expenses in high-cost metros can be a financial burden, even to middle-income households. In some metros, the typical sum of housing, taxes, childcare and transportation can exceed the median income, without even factoring in other necessities like the cost of food, education, and healthcare.

[1] SmartAsset Income Tax Calculator for a household filing as Single https://ift.tt/1IhBWQq

[2] According to Care.com's Care Index from https://www.care.com/care-index. These are 2017 numbers adjusted for 2018 inflation.

[3] Base on the most recent tiered data, from the second quarter 2017.

The post Which Metros Leave Households With the Most Money After Housing? appeared first on Zillow Research.

via Which Metros Leave Households With the Most Money After Housing?

No comments:

Post a Comment