A common misconception is that the typical first-time buyer is in their mid or late 20s-but the real median age is actually 34, according to the Zillow Group Consumer Housing Trends Report. About a third (32.5 percent) of first-timer buyers are 40 and older and a non-trivial share (15.5 percent) are 50 and older. Since most research focuses on the millennial and Gen Z first-time buyer, this misconception can lead to confusion around the home and purchasing needs of older first-time buyers.

A diverse group: Lower incomes overall, and more likely to buy with cash

Younger first-time buyers (under age 40) often become homeowners as they are forming new households with partners and spouses and having children. They have higher median household incomes than older-first-time buyers (40 or older), and they are more likely to leverage gifts from family or friends to help with their down payments.

Older first-time buyers are a more diverse group with varied experiences. Some may have been financially able to purchase a home but continued renting into midlife and beyond for lifestyle reasons, such as wanting to move frequently or not be tied to a mortgage. They are more confident about qualifying for financing, are more likely to be cash buyers (22.9 percent compared to 11.7 percent of younger first-time buyers), and are less likely to go over budget than their younger counterparts.

At the other end of the spectrum, some could have been waiting until they saved enough for a down payment. As a group, older-first time buyers are less likely to have sources besides savings for down payments. They have lower median household incomes ($57,500 compared to $72,500 for younger first-time buyers)[1] and buy more modest homes than their younger counterparts. This group may lack social networks to help them through the process for the first time-the way many younger first-time buyers lean on their parents.

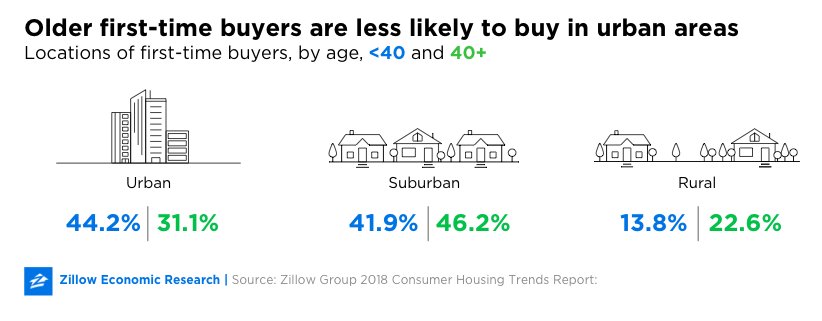

Older first timers also lean more toward suburban and rural areas than the younger cohort.

Family dynamics

Buying a home comes with large upfront costs, and couples are often better positioned to save for a down payment because they are more likely to have two incomes. It's not surprising that the majority of first-time buyers are married or living with a partner or spouse, no matter what their age.

Beyond that, the family dynamics of older and younger first-time buyers diverge. Younger first-time buyers are more likely to never have been married (23.2 percent versus 16.8 percent of older first-time buyers), and the older group is much more likely to be separated, divorced or widowed (14.9 percent versus 1.2 percent of the younger group). Older first-time buyers also are less likely to have children under 18 living in the home (48.1 percent of older first-timers versus 59.9 percent of younger ones).

Family help with a down payment could be one reason younger first-time buyers are purchasing homes earlier in life: Almost half of them used a gift from family or friends toward down payments, compared with only about a third of older first-timers. In fact, about 60 percent of older first-time buyers funded their down payments from a single source, typically savings.

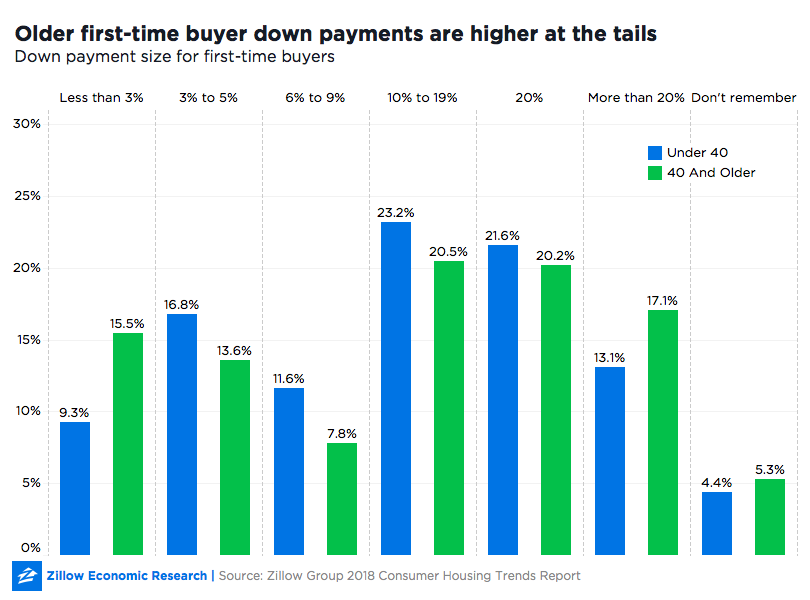

The size of their down payments also indicates a range of life experiences: Among first-time buyers who have mortgages, older first-time buyers are more likely to make down payments that are unusually low and unusually high.

Older first-timers less concerned about financing, with reason

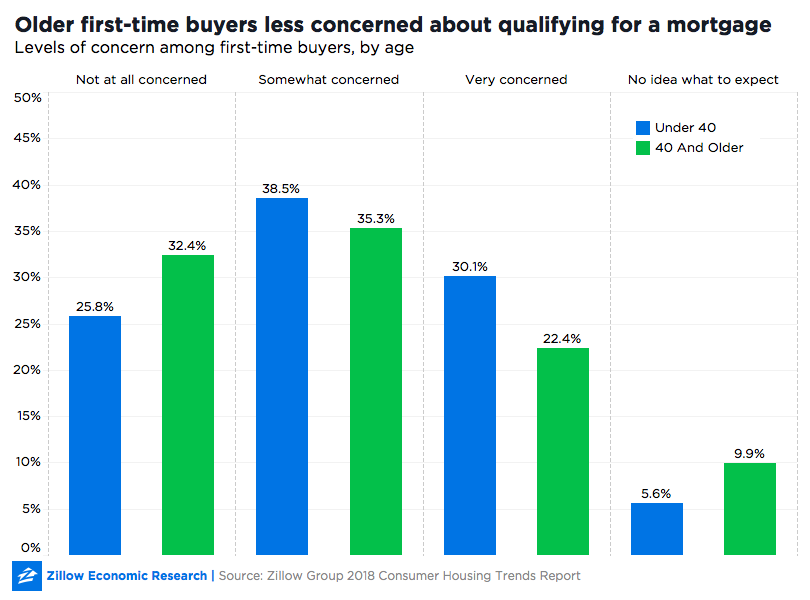

Less than a quarter of older first-time buyers said they were "very concerned" about qualifying for a mortgage, compared with almost a third of younger first-timers. And their experiences with lenders match those expectations: Only 21.9 percent of first-time buyers at midlife and beyond were denied prior to qualifying for a mortgage versus 35.5 percent of first-time buyers under 40.

Still, almost twice as many older first-time buyers said they didn't know what to expect when applying for a mortgage (9.9 percent versus 5.6 percent for the younger group). Perhaps older first-time buyers are experienced enough to know when they don't know something. It's also possible this segment of older buyers may lack social networks to help shepherd them through the process the way parents can help younger buyers.

Older first-time buyers purchase more modest homes-and don't blow their budgets

More than a quarter (27.4 percent) of younger first-time buyers go over budget in buying their starter homes, compared with about a fifth (19.9 percent) of older first-time buyers. The homes they end up with reflect that difference: Older first-time buyers purchase somewhat more modest homes (1,931 square feet with 3.1 bedrooms and 2.7 bathrooms) than their younger counterparts (2,000 square feet, 3.2 bedrooms, 3.5 bathrooms).

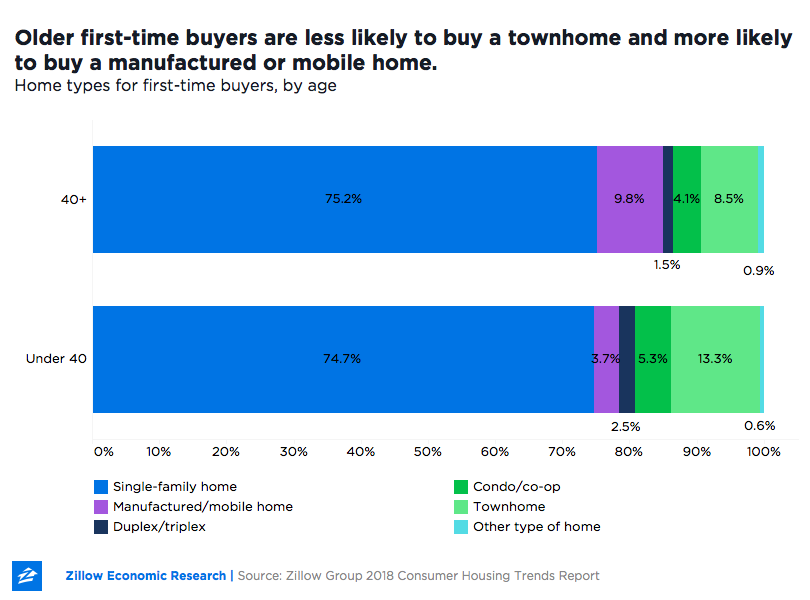

The single-family home is still the standard among first-time buyers of any age. The difference comes at the margins, with older first-time buyers more likely to buy a manufactured or mobile home-which could be related to their stronger preference for suburban and rural areas. Similarly, younger first-timers more likely to buy a townhome-which could be related to their propensity for urban living.

[1] Older first-time buyers have lower incomes if they are retired or in the later stages of their career. They also could have additional sources of assets and wealth.

The post Older First-Time Buyers Lean Suburban/Rural, Have Lower Incomes, More Likely to Pay With Cash appeared first on Zillow Research.

via Older First-Time Buyers Lean Suburban/Rural, Have Lower Incomes, More Likely to Pay With Cash

No comments:

Post a Comment