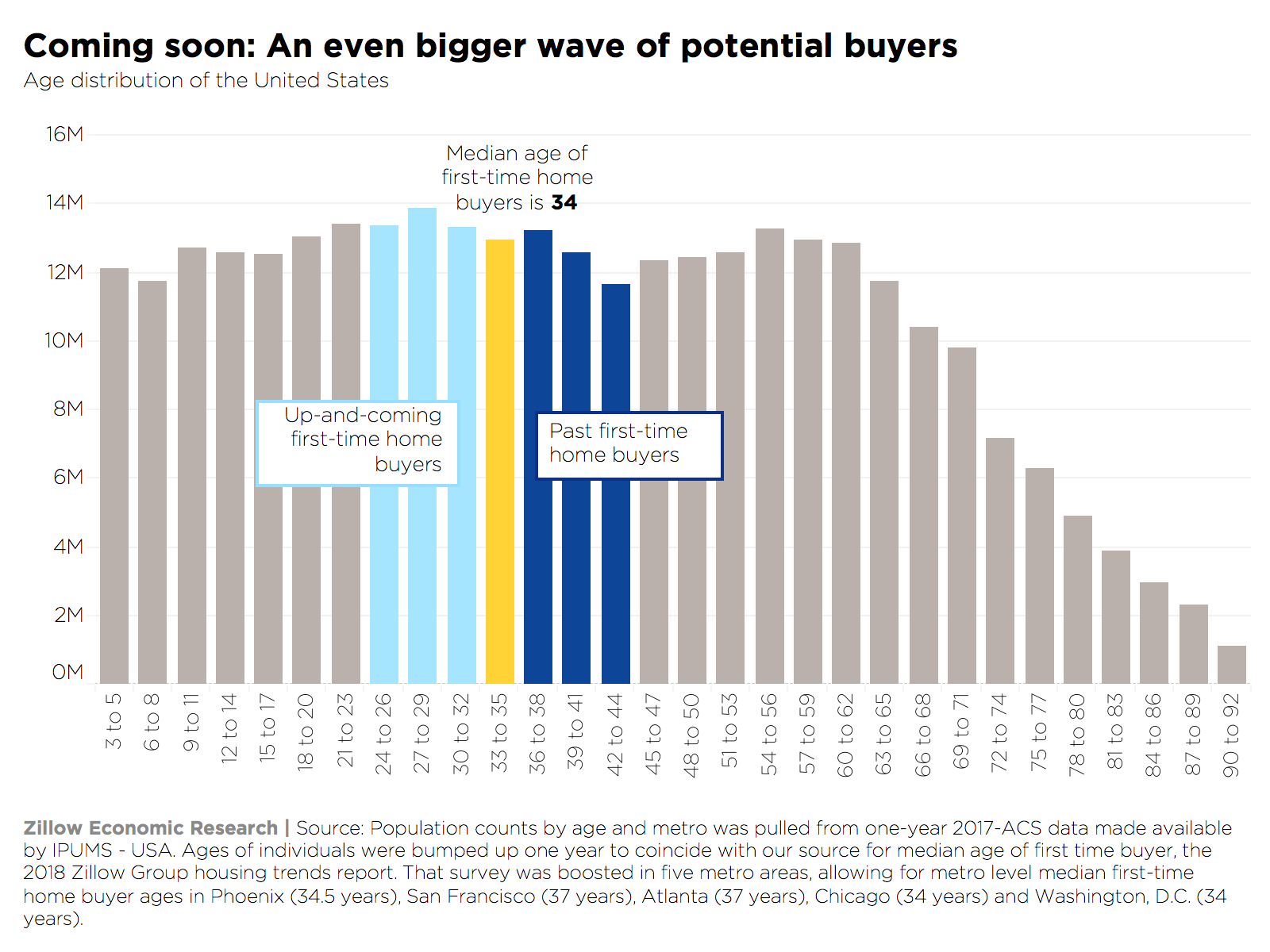

If you thought there were a lot of first-time home buyers over the past 10 years, check out what's coming: An extra 3.11 million people at prime first-time home-buying age. From 2019 through 2028, 44.9 million people will turn 34, the median age of current first-time home buyers. That's an increase of 7.4% from the past 10 years, when 41.8 million people passed that threshold. And while we can't say for sure whether the younger group will buy homes as readily when they hit their mid-thirties, by the sheer heft of their numbers, they will have an impact on the market.

Millennials hold such fascination partly because they are a massive generation, and that generational heft has yet to fully hit the home-buying market. The largest 3-year cohort in the U.S. is only 24 to 26 years old, yet the median age of the first-time home buyer is 34.

To imagine the scale of the millennial generation's impact on housing, let's look at the size of the U.S. population ages 35 to 44 relative to the cohort aged 24 to 33. We'll call the older set "past first-time home buyers" and the younger set "up-and-coming" first- time buyers. There are 3.11 million more up-and-coming than past first-time home buyers.

The relative size of the up-and-coming group is important for a few reasons:

Prices will climb quickly again

It's a comforting idea in a quickly cooling housing market that there is significant structural, long-term demand moving into home buying. This increases our confidence that the slowdown will correct itself before too long. The current home value declines in some expensive markets can be seen in this light as an important reset for down payment affordability for home buyers of the future.

Dearth of inventory pushing up the age at which people first buy

It suggests that the median age of the first-time buyers will continue to be pushed further and further out. The rate of single-family construction is still behind the pace of building we experienced back in the '90s, a more "normal" time in housing when home values and incomes took turns in the lead. Without an increase in truly new supply, we will need boomers to start downsizing in earnest to lubricate the housing market. As it currently stands, boomers are more often aging in place, contributing to low inventory numbers.

Rents will keep climbing, too

Younger generations' persistence in the rental market will continue to put pressure on those markets despite all the new apartment building. This is a huge generation and the rate of multifamily building, as aggressive as it seems for anyone watching the skylines of urban areas, does not make up for years' worth of shortfall when more capital was being directed to single-family building during the housing bubble.

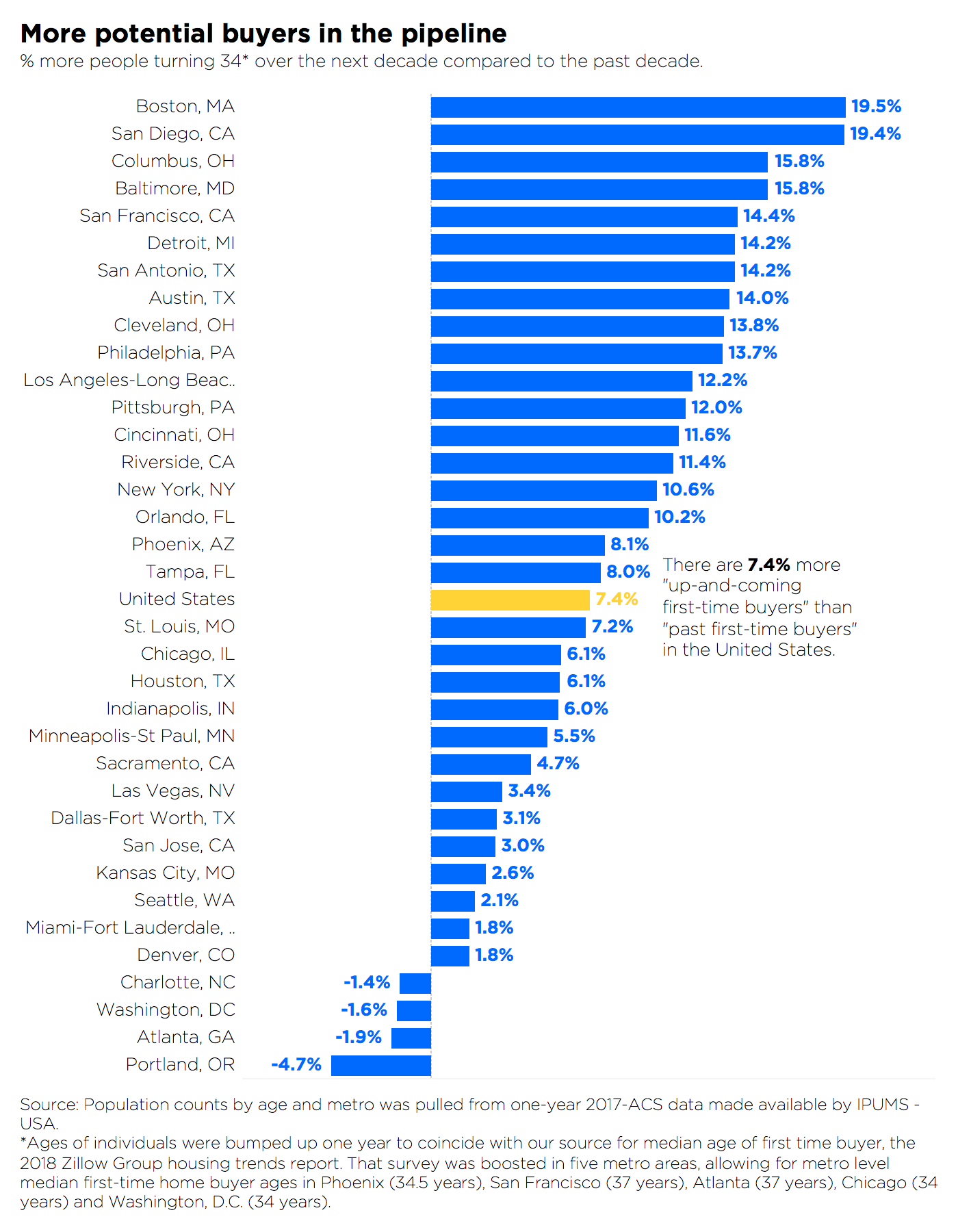

Jumping down to the metro level, the pressure implied by the relative size of "up-and-coming" and "past" first-time homebuyers varies greatly. In Boston or San Diego, for example, there are almost 20% more people in the younger than the older cohort.

Indeed, in 45 of the country's largest 50 metros, there are more potential first-time home buyers at the younger end of the pipeline. The only markets where that's not true are Charlotte, Washington, D.C., Atlanta, Raleigh, N.C., and Portland, Ore.. The relative affordability of Charlotte and Raleigh, along with the lower demographic pressure on housing needs, could influence migration from expensive, high-pressure markets that will likely be unable to facilitate the homeownership of many residents.

Consider San Francisco, for example. A notoriously expensive place to live, the median age of first-time home buyers in the San Francisco metro is 37. Looking at the shape of the San Francisco age distribution relative to the nation, San Francisco has more than its fair share of 27- to 36-year-olds, but under indexes on late-Gen Xers, young boomers, and teenagers. When families start to need more space for privacy loving teens, when they're searching for high-quality public high schools-and when they want both of those things affordably, they leave.

Time will tell whether the potential "up-and-coming" first-time home buyers buy homes at a similar rate as those who came before, or if they have to move to more affordable ground to make that happen. The life cycle of housing is intimately tied to the life cycles of our population. From this quick glance at the age distribution of the U.S. and major metro areas, what we do know is that challenges are ahead.

Methodology

Population counts by age and metro were pulled from 2017-ACS data made available by IPUMS – USA. Ages of individuals were bumped up one year to coincide with our source for median age of first-time buyer, the 2018 Zillow Group housing trends report. Median age of first-time home buyers was estimated at the national and regional level. While the median age of FTHBs by region matches the U.S. in the Northeast and Midwest, it increases to 36 in the South and decreases to 33 in the West. Due to sample boosting in five major metros, more local estimates of median age of first-time home buyers is available Atlanta (37 years old), Chicago (34 years old), Washington, D.C. (34 years old), Phoenix (34.5 years old), and San Francisco (37 years old).

The post Prices Are Cooling, But a Wave of Potential Buyers Is Coming Soon appeared first on Zillow Research.

via Prices Are Cooling, But a Wave of Potential Buyers Is Coming Soon

No comments:

Post a Comment